Understanding Post Employment Benefits: A Complete Guide for Employees and Employers

What Are Post Employment Benefits?

Definition and Core Concept

Post employment benefits are one of those things people don’t really think about—until they suddenly matter a lot. At their core, post employment benefits refer to any form of compensation or support that an employee receives after they have retired or left an organization. This isn’t just about pensions anymore; it’s a broad umbrella that includes healthcare, insurance, and other long-term financial support systems designed to provide stability when regular income stops.

Think of it like planting a tree while you’re still young. You may not enjoy its shade immediately, but over time, it becomes something you rely on. These benefits are structured to ensure that employees don’t face a financial cliff once their working years end. Instead, they transition into a phase where their past service continues to support their present needs.

Organizations typically design these benefits as part of their long-term employee value proposition. They aren’t just perks—they’re commitments. In fact, according to global workforce studies, over 60% of employees consider retirement benefits a critical factor when choosing or staying with an employer. That’s a powerful indicator of how central these benefits have become.

From a structural standpoint, post employment benefits can be either funded (where money is set aside in advance) or unfunded (where payments are made as obligations arise). Each approach carries its own financial implications, both for employers and employees. But regardless of the structure, the underlying goal remains the same: providing financial security and peace of mind after employment ends.

Why These Benefits Matter in Today’s Workforce

The importance of post employment benefits has grown dramatically over the last few decades, and it’s not hard to see why. Life expectancy is increasing, traditional family support systems are evolving, and the cost of living—especially healthcare—continues to rise. All of these factors combine to make retirement planning more complex than ever before.

Imagine working for 30 or 40 years and then suddenly having no steady income. Without post employment benefits, that scenario becomes a real risk. These benefits act as a safety net, helping individuals maintain their standard of living even when they are no longer earning a salary. In many ways, they bridge the gap between active employment and financial independence.

For employers, offering strong post employment benefits isn’t just about generosity—it’s strategic. Companies that provide robust retirement and post-retirement packages tend to attract higher-quality talent and retain employees longer. It builds loyalty and reduces turnover, which can save significant recruitment and training costs in the long run.

There’s also a societal angle to consider. Governments around the world are increasingly encouraging private-sector involvement in retirement planning because public pension systems are under pressure. This means employers are playing a larger role in ensuring financial stability for retirees. In fact, reports suggest that private retirement plans now account for a significant portion of retirement income in developed economies.

At a personal level, these benefits offer something that’s hard to quantify: peace of mind. Knowing that your future is at least partially secured allows you to focus on your present work and life without constant financial anxiety. And in today’s fast-paced, uncertain world, that kind of assurance is invaluable.

Types of Post Employment Benefits

Pension Plans

Pension plans are often the first thing that comes to mind when people hear about post employment benefits—and for good reason. They’ve been the backbone of retirement systems for decades, offering a structured way for employees to receive income after they stop working. But not all pension plans are created equal, and understanding the differences can make a huge impact on financial planning.

At a basic level, a pension plan is a retirement fund into which money is added during an employee’s working years and from which payments are drawn during retirement. These plans are typically sponsored by employers, although employees often contribute as well. The goal is simple: create a steady income stream for life after employment ends.

What makes pension plans particularly interesting is how they distribute risk. Depending on the type of plan, either the employer or the employee bears the responsibility for investment performance and funding adequacy. This distinction plays a crucial role in how secure—or uncertain—retirement income can be.

In recent years, there’s been a noticeable shift in how pension plans are structured. Traditional models are gradually being replaced by more flexible, employee-driven options. This shift reflects broader economic changes, including increased job mobility and the need for more adaptable financial solutions.

Understanding pension plans isn’t just about knowing how they work—it’s about recognizing their long-term impact. A well-structured pension can mean the difference between a comfortable retirement and financial struggle. That’s why both employers and employees need to pay close attention to how these plans are designed and managed.

Defined Benefit Plans

Defined benefit plans are often considered the gold standard of pension plans, mainly because of their predictability. Under this system, employees are promised a specific payout upon retirement, usually based on factors like salary history and years of service. It’s like having a financial guarantee waiting for you at the end of your career.

One of the biggest advantages of defined benefit plans is certainty. Employees know exactly what they’ll receive, which makes financial planning much easier. There’s no need to worry about market fluctuations or investment performance—the employer takes on that risk. This level of security is increasingly rare in today’s financial landscape.

However, this predictability comes at a cost—primarily for employers. Maintaining a defined benefit plan requires careful financial planning, actuarial assessments, and consistent funding. If investments underperform or liabilities increase, the employer must cover the shortfall. This has led many organizations to reconsider or phase out these plans altogether.

From an accounting perspective, defined benefit plans are also more complex. Companies must estimate future obligations and account for them in their financial statements, often leading to significant liabilities on their balance sheets. This complexity has been a driving factor behind the global shift toward defined contribution plans.

Despite these challenges, defined benefit plans still hold strong appeal, especially in the public sector and among long-tenured employees. They represent a traditional approach to retirement security—one that prioritizes stability over flexibility. And for many, that trade-off is well worth it.

Defined Contribution Plans

Defined contribution plans flip the script entirely. Instead of guaranteeing a specific payout, these plans define how much is contributed—usually by both the employer and the employee—but leave the final outcome dependent on investment performance. In other words, the risk shifts from the employer to the employee.

This type of plan has become increasingly popular, especially in the private sector. One reason is flexibility. Employees often have control over how their funds are invested, allowing them to tailor their portfolios based on their risk tolerance and financial goals. It’s a more hands-on approach to retirement planning.

Another advantage is portability. In today’s world, where people change jobs more frequently, defined contribution plans offer a level of continuity that traditional pensions often lack. Employees can carry their retirement savings with them, making it easier to build wealth over time regardless of career changes.

However, this flexibility comes with responsibility. Employees must make informed investment decisions, and not everyone has the financial literacy to do so effectively. Market volatility can also significantly impact retirement savings, introducing a level of uncertainty that defined benefit plans largely avoid.

Despite these challenges, defined contribution plans are now the dominant form of retirement benefit in many countries. They align well with modern workforce trends and provide a scalable solution for employers. But they also highlight the growing importance of financial education, as individuals take on a more active role in securing their future.

Other Post Employment Benefits (OPEB)

When people think about retirement perks, pensions usually steal the spotlight. But there’s another category quietly carrying just as much weight—Other Post Employment Benefits (OPEB). These benefits go beyond income and focus on essential life needs, particularly healthcare and insurance coverage after retirement. And if you’ve ever looked at medical costs in later life, you already know why this matters.

OPEB includes a wide range of non-pension benefits provided to employees once they leave the workforce. These can include retiree healthcare plans, dental and vision coverage, life insurance, and even long-term disability support. While they may seem like “extras,” they often end up being the difference between financial stability and serious hardship during retirement years.

Here’s the reality: healthcare costs tend to increase as people age. According to industry estimates, a retired couple in the U.S. may need hundreds of thousands of dollars just to cover medical expenses throughout retirement. That’s not a small number—it’s a potential financial burden that can wipe out savings quickly. OPEB helps offset this risk by providing structured support.

From an employer’s perspective, offering OPEB can be both a competitive advantage and a financial challenge. These benefits are highly valued by employees, but they also create long-term liabilities that must be carefully managed. Many organizations are now reevaluating how they offer these benefits, often shifting toward cost-sharing models or capped contributions.

What makes OPEB particularly complex is its unpredictability. Unlike pensions, which can be calculated with relative precision, healthcare costs fluctuate based on inflation, policy changes, and individual health conditions. That uncertainty makes planning more difficult—but also more necessary.

Ultimately, OPEB reflects a broader philosophy: retirement isn’t just about income—it’s about quality of life. And without proper healthcare and insurance support, even the best pension plan can fall short.

Healthcare Benefits After Retirement

Healthcare is easily one of the most critical—and expensive—components of post employment benefits. While pensions provide income, retiree healthcare benefits ensure that individuals can actually use that income to live comfortably rather than spend it all on medical bills. It’s not just about coverage; it’s about preserving financial dignity.

Many employers offer healthcare plans that extend into retirement, either fully or partially subsidized. These plans may cover hospital visits, prescription drugs, preventive care, and specialist consultations. Some even include wellness programs designed to help retirees maintain better health over time, which can reduce long-term costs.

But here’s where things get tricky: healthcare inflation consistently outpaces general inflation. This means the cost of medical services rises faster than most other expenses. Without employer-sponsored coverage, retirees often find themselves paying significantly more out of pocket, especially in countries where public healthcare systems are limited or overburdened.

Employers are increasingly moving toward cost-sharing models, where retirees pay a portion of premiums or expenses. While this reduces the financial burden on companies, it also shifts some responsibility back to employees. It’s a delicate balance—one that requires transparency and careful planning on both sides.

There’s also a growing trend toward Health Savings Accounts (HSAs) and similar tools, which allow employees to set aside pre-tax income specifically for medical expenses in retirement. These accounts add another layer of flexibility, giving individuals more control over how they manage their healthcare costs.

At the end of the day, healthcare benefits aren’t just a nice addition—they’re essential. Without them, retirement planning becomes incomplete. And as life expectancy continues to rise, their importance will only grow.

Life Insurance and Disability Coverage

Life doesn’t stop being unpredictable just because someone retires. That’s where life insurance and disability coverage come into play as part of post employment benefits. These elements often get overlooked, but they provide a crucial safety net for retirees and their families.

Retiree life insurance policies are typically smaller than those offered during active employment, but they still serve an important purpose. They can help cover final expenses, outstanding debts, or provide financial support to surviving family members. It’s less about wealth replacement and more about financial protection during a vulnerable phase of life.

Disability coverage, while less common post-retirement, can still be relevant—especially for individuals who retire early or transition into part-time work. Some plans offer limited protection against conditions that prevent retirees from maintaining supplemental income streams. In that sense, they act as a buffer against unexpected disruptions.

Employers offering these benefits often do so as part of a broader commitment to employee well-being. However, maintaining these programs requires careful cost management, particularly as the workforce ages and claims increase. Some organizations have started offering optional or voluntary insurance plans, allowing retirees to opt in and pay premiums based on their needs.

From the employee’s perspective, these benefits add another layer of reassurance. Retirement is often portrayed as a time of relaxation and freedom, but it also comes with uncertainties. Having insurance coverage in place helps mitigate some of those risks, making the transition smoother and more secure.

In many ways, life insurance and disability coverage are like the quiet guardians of retirement planning. They may not be front and center, but when needed, they make all the difference.

How Post Employment Benefits Work

Funding Mechanisms

Understanding how post employment benefits are funded is where things start to get a bit technical—but stick with it, because this is where the real story unfolds. These benefits don’t just appear out of nowhere; they’re built over time through structured financial strategies designed to ensure future obligations can be met.

There are two primary funding approaches: funded plans and unfunded plans. Funded plans involve setting aside money in advance, typically in a trust or investment fund, which grows over time. Think of it like saving for a big purchase—you contribute regularly so that when the time comes, the money is already there.

Unfunded plans, on the other hand, operate on a “pay-as-you-go” basis. Employers pay benefits directly from their current revenues when they become due. While this approach may seem simpler, it can create significant financial strain if not managed carefully, especially as the number of retirees increases.

Investment plays a major role in funded plans. Contributions are often invested in a mix of assets such as stocks, bonds, and real estate. The goal is to generate returns that will help cover future benefit payments. However, this also introduces risk—market downturns can impact the value of these funds, potentially creating funding gaps.

Actuarial calculations are another key component. Experts use statistical models to estimate future obligations based on factors like employee lifespan, salary growth, and retirement age. These estimates guide how much needs to be contributed today to meet tomorrow’s commitments.

In essence, funding mechanisms are the backbone of post employment benefits. Without proper funding, even the most generous benefit plans can become unsustainable. And that’s why organizations invest so much effort into getting this part right.

Employer vs Employee Contributions

The balance between employer and employee contributions is a defining feature of any post employment benefit plan. It determines not only how the plan is funded but also how risk and responsibility are shared.

In traditional setups—especially with defined benefit plans—employers bear most of the financial responsibility. They commit to providing a specific level of benefits and must ensure sufficient funding regardless of market conditions. Employees may contribute a small portion, but the bulk of the burden lies with the organization.

Defined contribution plans, however, take a different approach. Here, both employers and employees contribute to individual accounts, often with employers matching a percentage of employee contributions. This creates a shared responsibility model, where both parties have a stake in the outcome.

One of the biggest advantages of this approach is transparency. Employees can see exactly how much is being contributed and how their investments are performing. It also encourages more active participation in retirement planning, which can lead to better financial outcomes—provided individuals make informed decisions.

But there’s a trade-off. With greater control comes greater risk. Employees must navigate investment choices, market volatility, and long-term planning on their own. Without proper guidance, this can lead to suboptimal outcomes.

Employers, meanwhile, benefit from more predictable costs. Instead of dealing with uncertain future liabilities, they commit to fixed contributions. This makes financial planning easier and reduces long-term risk.

Ultimately, the contribution structure reflects a broader shift in the employment landscape—from employer-driven security to shared responsibility. And while this model offers flexibility, it also underscores the importance of financial literacy and proactive planning.

Accounting for Post Employment Benefits

Key Accounting Standards (IFRS & GAAP)

When you peel back the curtain on post employment benefits, you quickly realize they’re not just HR perks—they’re major financial commitments that must be reported with precision. This is where accounting standards like IFRS (International Financial Reporting Standards) and GAAP (Generally Accepted Accounting Principles) come into play. These frameworks ensure that organizations don’t just promise benefits but also transparently account for the cost of those promises.

Under IFRS (specifically IAS 19), companies are required to recognize the full extent of their obligations related to employee benefits, including pensions and OPEB. This involves estimating future payments and discounting them back to present value. It’s not guesswork—it’s a structured process grounded in actuarial science, financial modeling, and economic assumptions. The goal is simple: reflect the true cost of employee benefits on financial statements.

GAAP, particularly in the United States, follows a similar philosophy but with some technical differences in measurement and recognition. For example, GAAP allows certain smoothing techniques to reduce volatility in reported expenses, whereas IFRS tends to favor more immediate recognition of gains and losses. These differences may seem subtle, but they can significantly impact how a company’s financial health appears to investors.

Why does this matter? Because post employment benefits can represent billions in liabilities for large organizations. Misreporting or underestimating these obligations can distort financial statements and mislead stakeholders. That’s why regulators take compliance seriously, and companies invest heavily in actuarial expertise.

Another interesting aspect is how sensitive these calculations are to assumptions. A small change in discount rates or life expectancy can dramatically alter the reported liability. It’s a bit like adjusting the lens on a camera—slight shifts can completely change the picture.

In practice, these accounting standards do more than ensure compliance. They force organizations to confront the long-term implications of their benefit plans. And in doing so, they play a crucial role in shaping how those plans are designed and managed.

Recognition and Measurement

If accounting standards are the rulebook, then recognition and measurement are the actual game being played. This is where companies determine when and how to record post employment benefit obligations in their financial statements—and it’s far from straightforward.

Recognition begins with identifying when an obligation arises. In most cases, this happens as employees render service. Every year an employee works, they earn a portion of their future benefits. That means companies must continuously account for these accumulating obligations, rather than waiting until retirement.

Measurement, on the other hand, is all about quantifying those obligations. This involves calculating the present value of future benefit payments, using assumptions about salary growth, employee turnover, mortality rates, and discount rates. It’s a complex process that relies heavily on actuarial valuations.

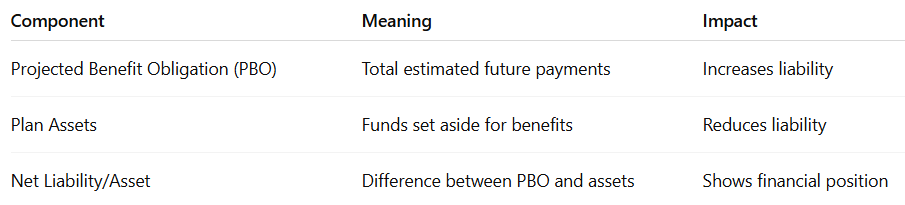

One key concept here is the Projected Benefit Obligation (PBO), which estimates the total benefits owed to employees based on current and future salaries. Another is the fair value of plan assets, which represents the funds set aside to meet those obligations. The difference between these two figures determines whether a plan is overfunded or underfunded.

Here’s a simple comparison to make it clearer:

What makes this process particularly challenging is volatility. Market fluctuations can affect plan assets, while changes in assumptions can alter liabilities. This creates swings in financial statements that companies must carefully manage and explain to stakeholders.

In essence, recognition and measurement turn abstract promises into concrete numbers. And those numbers carry real weight—not just for accountants, but for investors, employees, and regulators alike.

Advantages of Post Employment Benefits

Benefits for Employees

From an employee’s perspective, post employment benefits are more than just financial tools—they’re a form of long-term security that shapes how people think about their careers and futures. Imagine working for decades with the confidence that your later years are already being taken care of. That’s the kind of reassurance these benefits provide.

One of the most obvious advantages is income stability after retirement. Whether through pensions or defined contribution plans, employees gain access to a steady stream of income that helps maintain their lifestyle. This reduces dependence on personal savings alone, which can be unpredictable.

Healthcare benefits add another layer of protection. As discussed earlier, medical expenses can skyrocket with age. Having employer-supported healthcare coverage ensures that retirees don’t have to choose between their health and their finances. It’s not just about affordability—it’s about access to quality care.

There’s also a psychological benefit that often goes unnoticed. Knowing that your future is secure can reduce stress and improve overall well-being during your working years. Employees who feel financially secure are often more engaged, productive, and loyal to their organizations.

Another key advantage is tax efficiency. Many post employment benefit plans offer tax-deferred growth, meaning employees don’t pay taxes on contributions or earnings until they withdraw funds. This allows investments to grow faster over time, enhancing overall returns.

Finally, these benefits encourage long-term planning. They nudge employees to think beyond immediate needs and consider their future goals. In a world where instant gratification often takes priority, that kind of forward-thinking mindset is incredibly valuable.

Benefits for Employers

While post employment benefits are often seen as employee-centric, they offer substantial advantages for employers as well. In fact, these benefits are a powerful strategic tool that can influence everything from recruitment to organizational culture.

First and foremost, offering strong post employment benefits helps attract top talent. In competitive job markets, candidates don’t just look at salaries—they evaluate the entire compensation package. A robust retirement plan or healthcare benefit can be the deciding factor between two job offers.

Retention is another major benefit. Employees are more likely to stay with a company that invests in their long-term well-being. This reduces turnover, which in turn lowers recruitment and training costs. According to workforce studies, replacing an employee can cost anywhere from 50% to 200% of their annual salary, making retention a critical priority.

These benefits also enhance employer branding. Companies that prioritize employee welfare tend to build stronger reputations, both internally and externally. This can lead to higher employee satisfaction, better performance, and even increased customer trust.

From a financial perspective, certain benefit contributions are tax-deductible, providing cost advantages for organizations. Additionally, defined contribution plans offer predictable expenses, making budgeting and financial planning more manageable.

There’s also a cultural dimension. Providing post employment benefits signals that a company values its employees beyond their immediate output. It fosters a sense of loyalty and mutual respect, which can translate into a more cohesive and motivated workforce.

In short, post employment benefits aren’t just an expense—they’re an investment. And when managed effectively, they deliver returns that go far beyond the balance sheet.

Challenges and Risks

Financial and Economic Risks

As appealing as post employment benefits are, they come with a fair share of challenges—especially on the financial side. These plans involve long-term commitments, and predicting the future is never as simple as it sounds.

One of the biggest risks is investment volatility. For funded plans, the performance of investments directly affects the ability to meet future obligations. A market downturn can significantly reduce plan assets, creating funding gaps that employers must fill.

Interest rates also play a critical role. Lower discount rates increase the present value of liabilities, making obligations appear larger. This can put pressure on company finances, particularly during economic downturns.

Another major concern is longevity risk. People are living longer, which means benefits must be paid out for extended periods. While this is a positive societal trend, it increases the financial burden on benefit plans.

Inflation, particularly in healthcare, adds another layer of complexity. Rising costs can outpace initial estimates, leading to higher-than-expected expenses. This is especially relevant for OPEB, where medical inflation can significantly impact long-term liabilities.

These risks require careful management through diversification, actuarial analysis, and ongoing monitoring. Without proactive strategies, even well-designed plans can become unsustainable.

Regulatory and Compliance Issues

Beyond financial risks, organizations must navigate a complex web of regulatory and compliance requirements. Governments impose strict rules to ensure that employee benefits are managed responsibly and transparently.

These regulations cover everything from funding requirements to disclosure obligations. Companies must regularly report the status of their benefit plans, including assets, liabilities, and assumptions used in calculations. Failure to comply can result in penalties, legal issues, and reputational damage.

One challenge is that regulations are constantly evolving. Changes in accounting standards, tax laws, or pension regulations can require organizations to adjust their plans and reporting practices. Staying compliant requires ongoing attention and expertise.

There’s also the issue of cross-border operations. Multinational companies must navigate different regulatory frameworks in each country, adding another layer of complexity. What works in one region may not be applicable in another.

In many ways, compliance is like navigating a moving target. It requires flexibility, vigilance, and a deep understanding of both local and global standards.

Trends and Future of Post Employment Benefits

Shift Toward Defined Contribution Plans

One of the most significant trends in recent years is the global shift from defined benefit plans to defined contribution plans. This change reflects broader economic realities and evolving workforce expectations.

Employers are increasingly favoring defined contribution plans because they offer cost predictability and reduced financial risk. Instead of committing to uncertain future payouts, companies contribute fixed amounts, making budgeting more straightforward.

Employees, on the other hand, gain more control over their retirement savings. They can choose how to invest their funds and adjust their strategies based on personal goals. This flexibility aligns well with modern career paths, which often involve multiple job changes.

However, this shift also places greater responsibility on individuals. Without proper financial literacy, employees may struggle to make informed decisions, potentially affecting their retirement outcomes.

Role of Technology and Personal Financial Planning

Technology is reshaping how people approach post employment benefits. From digital investment platforms to AI-driven financial advice, individuals now have access to tools that make retirement planning more accessible and personalized.

Employers are also leveraging technology to manage benefit plans more efficiently. Automated systems, data analytics, and predictive modeling help organizations optimize funding strategies and improve decision-making.

At the same time, there’s a growing emphasis on financial education. Companies are offering workshops, online resources, and advisory services to help employees understand their benefits and make better choices.

This combination of technology and education is transforming post employment benefits from a passive system into an active, user-driven experience. And as innovation continues, the future of these benefits will likely become even more dynamic and personalized.

Conclusion

Post employment benefits are no longer just a corporate obligation—they’re a cornerstone of financial security in an increasingly uncertain world. They bridge the gap between active employment and retirement, ensuring that individuals can maintain their quality of life long after their careers end. From pensions to healthcare and beyond, these benefits touch nearly every aspect of post-work life.

For employers, they represent both a responsibility and an opportunity. When designed thoughtfully, they attract talent, build loyalty, and strengthen organizational culture. For employees, they offer stability, confidence, and a pathway to a more secure future.

As economic conditions evolve and life expectancy increases, the importance of these benefits will only grow. Understanding how they work isn’t just helpful—it’s essential for making informed decisions about careers, finances, and long-term well-being.

FAQs

1. What are post employment benefits in simple terms?

Post employment benefits are payments or services provided to employees after they retire or leave a company, such as pensions, healthcare, and insurance.

2. What is the difference between defined benefit and defined contribution plans?

Defined benefit plans guarantee a fixed payout, while defined contribution plans depend on contributions and investment performance.

3. Are post employment benefits mandatory for employers?

It depends on local laws and regulations. Some benefits are required, while others are optional and offered as part of compensation packages.

4. Why are healthcare benefits important after retirement?

Healthcare costs increase with age, and these benefits help cover medical expenses, reducing financial strain.

5. How are post employment benefits funded?

They can be funded through employer/employee contributions invested over time or paid directly when benefits are due.

SOURCEs

https://www.ifrs.org/issued-standards/list-of-standards/ias-19-employee-benefits/

https://www.ssa.gov/benefits/retirement/

https://www.dol.gov/agencies/ebsa

https://www.oecd.org/pensions/

https://www.worldbank.org/en/topic/socialprotection

https://www.fidelity.com/viewpoints/retirement/health-care-costs

https://www.investopedia.com/terms/p/postemployment-benefits.asp