Co-insurance Examples: A Complete Guide to Understanding and Calculating It

Understanding health or property insurance feels like decoding a secret language. One of the most confusing terms? Co-insurance. If you’ve ever stared blankly at your Explanation of Benefits (EOB) or felt sucker-punched by a medical bill, chances are co-insurance played a role. But don’t worry—we’re going to break this down like a human, not a robot.

Let’s make this simple. Think of co-insurance as your part of the bill after insurance chips in. It's like splitting the tab at dinner, only this time, you're splitting a hospital bill or property damage repair. Sound unfair? Maybe. But knowing how it works can save you thousands—and a ton of stress.

What Is Co-insurance?

Co-insurance is your share of the costs of a covered service, calculated as a percentage (not a flat fee). After you've paid your deductible, your insurance kicks in—but not 100%. You and the insurer share the remaining cost. That's co-insurance.

Let’s say you have an 80/20 co-insurance plan. That means your insurer pays 80%, and you're on the hook for 20%—after your deductible is met.

But wait, isn’t that the same as a co-pay? Nope.

A co-pay is a fixed fee (like $30 for a doctor’s visit).

Co-insurance is percentage-based and kicks in after the deductible.

So, while co-pay is predictable, co-insurance depends on the total bill. That’s why understanding it matters so much—it directly affects how much you pay out of pocket.

How Does Co-insurance Work?

Here’s where things get real. You don’t pay co-insurance on day one. First, you meet your deductible. Only after that does co-insurance kick in.

Let’s walk through it:

You have a $2,000 deductible.

You rack up $5,000 in medical bills.

You pay the first $2,000 (your deductible).

Now $3,000 remains.

If your plan is 80/20:

Insurance pays 80% of $3,000 = $2,400.

You pay 20% of $3,000 = $600.

That’s co-insurance in action.

The most common co-insurance splits include:

80/20 (most standard)

70/30 (you pay more)

90/10 (better coverage, higher premiums)

Co-insurance also ends when you hit your out-of-pocket maximum—more on that later.

Importance of Understanding Co-insurance

If you don’t get how co-insurance works, you're at risk—financially. One ER visit can lead to a four-digit bill, and if you’re blindsided by your share, it can be devastating.

Why should you care?

Budgeting: Knowing your 20% could mean $600 (or $6,000) is crucial for planning.

Choosing plans: Lower premiums often come with higher co-insurance.

Avoiding surprise bills: Some services may apply differently depending on the provider or the network.

Not understanding co-insurance is like driving blindfolded through a toll road. You may reach the destination, but the price might shock you when you arrive.

Common Co-insurance Percentages Explained

Let’s get into the nitty-gritty. These are the most common co-insurance breakdowns:

80/20 Plan

You pay 20%, insurance pays 80%.

Example: $1,000 bill post-deductible? You pay $200.

70/30 Plan

More cost for you.

You pay 30% ($300 on a $1,000 bill).

90/10 Plan

Less risk, higher premiums.

You pay 10% ($100 on a $1,000 bill).

When are they used?

Employer plans often offer 80/20.

Budget plans (cheaper premiums) tend to be 70/30.

High-premium, gold-level plans are usually 90/10.

Knowing this helps you compare apples to apples during open enrollment.

Example 1: Co-insurance in Health Insurance

Let’s say you have a surgery that costs $10,000.

Your plan details:

Deductible: $1,500

Co-insurance: 80/20

Out-of-pocket max: $6,000

Here’s what happens:

You pay the first $1,500 (deductible).

Remaining bill: $8,500

Insurance pays 80% of $8,500 = $6,800

You pay 20% = $1,700

Total paid by you:

Deductible: $1,500

Co-insurance: $1,700

Total: $3,200

Not terrible… unless you thought insurance was footing the whole bill.

Also, if that $3,200 pushes you closer to your out-of-pocket max, any costs beyond that will be covered at 100%.

Example 2: Co-insurance in Property Insurance

Co-insurance isn’t just a health insurance term—it plays a massive role in property insurance too, especially for homeowners and businesses. This type of co-insurance works a little differently but can be just as costly if misunderstood.

Imagine you have a commercial property insured for $400,000, but the replacement value of the building is $800,000. Your policy includes an 80% co-insurance clause. That means you should insure at least 80% of the building’s replacement cost—which is $640,000 (80% of $800,000).

But you only insured it for $400,000. Uh-oh.

Now a storm causes $200,000 in damage. You file a claim, thinking your insurance will cover it. But due to the co-insurance clause, the insurance company will penalize you for underinsuring the property.

Here’s the math using the co-insurance penalty formula:

(Amount of Insurance Carried / Amount Required) × Loss = Claim Payout

So:

($400,000 / $640,000) × $200,000 = $125,000

You’ll only get $125,000 from the insurer. You’re on the hook for the remaining $75,000—all because of a co-insurance clause you didn’t fully understand.

This is why it's crucial to insure your property at or above the required co-insurance level. Otherwise, you're essentially self-insuring part of the risk—and it can come back to bite hard.

Example 3: Co-insurance in Commercial Insurance

Now let’s look at co-insurance in commercial insurance policies, particularly those involving business property and inventory.

Suppose a small retail business insures its building and contents for $500,000. The actual replacement cost value is $1,000,000, and the co-insurance clause requires 90% coverage.

That means they should have at least $900,000 in coverage to meet the co-insurance requirement. Since they’re underinsured, here’s what happens when there’s a $100,000 loss due to a fire:

($500,000 / $900,000) × $100,000 = $55,555

That’s all they get from the insurance company. They’re responsible for the remaining $44,445.

This type of clause ensures businesses don’t lowball their coverage to save on premiums. Insurers expect a shared responsibility, and failing to meet the co-insurance requirement results in a penalty during claims.

Bottom line? Always check your commercial policy's co-insurance percentage, and insure accordingly.

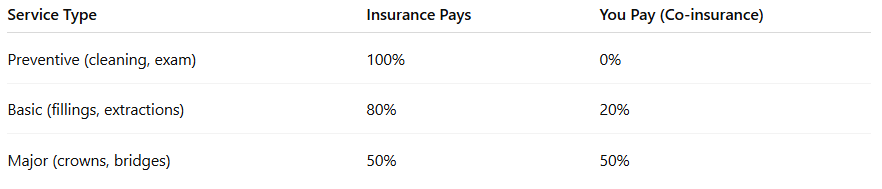

Example 4: Dental Insurance Co-insurance

Dental insurance also uses co-insurance to manage cost-sharing between the insurer and patient. Here’s a breakdown of a common structure:

Let’s say you need a crown that costs $1,200. Under a typical plan:

Insurance pays 50% = $600

You pay 50% = $600

No deductible? Lucky you. But some plans require you to meet a deductible before co-insurance applies. Also, dental plans often have an annual max, like $1,500—once that’s hit, you pay 100%.

Knowing your plan’s co-insurance structure helps you plan treatments throughout the year, and avoid surprise bills.

Example 5: Travel Insurance Co-insurance

Co-insurance can sneak into travel insurance, especially in policies that cover emergency medical care abroad.

Let’s say you’re traveling in Europe, and you suddenly require emergency surgery. The bill totals $20,000.

Your travel insurance policy:

Deductible: $500

Co-insurance: 80/20

Emergency medical coverage: up to $100,000

Here’s how it breaks down:

You pay $500 deductible.

Remaining: $19,500.

Insurance pays 80% = $15,600.

You pay 20% = $3,900.

Yikes. That vacation got expensive fast.

Always read the co-insurance terms of travel insurance policies. Some offer 100% coverage after deductible, while others share costs. Don’t assume you're covered without checking the fine print.

Co-insurance vs. Deductible

These two terms are often misunderstood—so let’s clear the fog.

Deductible: The fixed amount you pay before your insurance kicks in.

Co-insurance: The percentage you pay after you’ve met your deductible.

Think of it like this:

You’re climbing a mountain (your medical bill).

The deductible is the first part—you climb it alone.

After that, your insurance joins the hike—but you still share the rest of the journey (co-insurance).

Finally, once you hit the peak (your out-of-pocket max), insurance carries you the rest of the way.

They’re both your financial responsibility—but at different stages.

The Role of Out-of-Pocket Maximum

Here’s the good news: you’re not paying co-insurance forever.

Enter the out-of-pocket maximum—a cap on how much you pay in total for covered services in a year.

Once you reach this amount:

Insurance pays 100% of covered costs.

Your co-insurance? Gone.

Your deductible? Already met.

Co-pays? Waived on many plans.

For example:

Deductible: $2,000

Out-of-pocket max: $6,000

Co-insurance: 80/20

You’d pay:

$2,000 (deductible)

$4,000 (your 20% co-insurance portion)

Total: $6,000 → after this, insurance pays 100%.

This max is your financial safety net. Without it, there’d be no cap to your medical spending.

How to Calculate Your Co-insurance Costs

Let’s say you want to estimate how much you’d owe for a $10,000 surgery under your plan. Here’s the step-by-step method:

Know your deductible: e.g., $1,500

Subtract deductible from total bill: $10,000 - $1,500 = $8,500

Apply co-insurance percentage: You pay 20% of $8,500 = $1,700

Add deductible back: $1,500 + $1,700 = $3,200 total out-of-pocket

Easy formula:

(Total Cost - Deductible) × Your Co-insurance % + Deductible = Your Total Cost

Use this before big procedures. It helps avoid sticker shock.

Tips for Managing High Co-insurance Plans

High co-insurance can feel brutal. But there are ways to ease the burden:

Use HSA or FSA: These tax-advantaged accounts help you pay medical costs with pre-tax dollars.

Shop around: Use insurance tools to compare procedure costs across providers.

Negotiate bills: Hospitals often reduce bills for self-pay or high-deductible patients.

Ask for generic meds: Brand-name drugs can dramatically increase your co-insurance.

Reach out for payment plans: Providers will usually let you split the bill over months.

Being proactive is your best defense.

How to Compare Insurance Plans with Different Co-insurance

Choosing the right insurance plan can feel like solving a puzzle with a blindfold. Between monthly premiums, deductibles, and co-insurance rates—it’s easy to get overwhelmed. But here's a truth bomb: comparing co-insurance percentages could save you thousands over time.

Let’s say you’re offered two plans:

At first glance, Plan A seems cheaper due to the lower premium. But if you anticipate medical costs (say you’re managing a chronic illness or planning a surgery), Plan B could be the smarter choice.

Let’s do the math for a $20,000 medical bill in one year:

Plan A:

Deductible: $1,500

Remaining: $18,500 × 20% = $3,700

Total out-of-pocket: $5,200

Plan B:

Deductible: $1,000

Remaining: $19,000 × 10% = $1,900

Total out-of-pocket: $2,900

That’s a $2,300 difference, not to mention you’re already paying more per month in Plan B—but if you reach your out-of-pocket max, the savings may offset the higher premium.

Pro tip: Always balance monthly premium with:

Likely healthcare usage

Prescription needs

Access to specialists

Co-insurance percentages

It’s not just about what you pay each month—it’s about what you’ll owe when it matters most.

Common Misconceptions About Co-insurance

Let’s bust some myths—because co-insurance is often misunderstood (and sometimes purposely misrepresented).

Misconception #1: Co-insurance is the same as a co-pay

Nope. A co-pay is a fixed amount you pay for a service (like $25 for a doctor visit). Co-insurance is a percentage of the total cost of care after your deductible is met.

Misconception #2: Co-insurance applies to everything

Not always. Some plans exempt preventive care (like vaccines and annual checkups) from co-insurance. Others apply it only to hospital stays or specialist visits.

Misconception #3: You always know what you’ll pay

Since co-insurance is percentage-based, your costs vary depending on the provider’s billing and the complexity of services. It’s not always predictable unless you get a pre-authorization or estimate from your provider.

Misconception #4: Insurance pays 80% of the entire bill

Not quite. They pay 80% of the allowed amount—a pre-negotiated rate between providers and insurers. If your provider charges more, you may be responsible for the balance unless they’re in-network.

Clearing up these misconceptions can help you avoid surprise bills and make smarter insurance choices.

Conclusion

Co-insurance might sound like just another piece of complicated insurance jargon—but it's actually one of the most critical elements in determining how much money comes out of your pocket. Whether you’re dealing with health insurance, dental care, travel emergencies, or property coverage, understanding how co-insurance works empowers you to make better decisions, plan your budget, and protect yourself from financial surprises.

Let’s be real—most people don’t take the time to read their policy until they’re facing a $10,000 medical bill. Don’t be that person. Learn how to calculate your costs now, compare plans wisely, and ask the right questions before signing up for any insurance coverage.

Co-insurance can be your friend—or your financial enemy. The difference? Knowledge. Now that you’ve got it, you’re one step ahead.

FAQs

1. What does 80/20 co-insurance mean?

It means that after you've met your deductible, your insurance will cover 80% of the cost of covered services, and you're responsible for the remaining 20%.

2. Is co-insurance applied before or after the deductible?

Co-insurance only applies after you’ve met your deductible. First, you pay the deductible. Then, co-insurance kicks in for the remaining balance.

3. How can I avoid high co-insurance costs?

Choose in-network providers, ask for estimates in advance, utilize HSAs or FSAs, and pick insurance plans with lower co-insurance percentages—if it fits your budget and needs.

4. Are co-insurance percentages negotiable?

Not typically. However, you can often negotiate the total bill amount with your provider, especially if you're paying out of pocket or have high co-insurance responsibilities.

5. Can co-insurance apply to prescriptions?

Yes, depending on the plan. Some insurance policies apply co-insurance percentages to certain prescription tiers, especially high-cost specialty medications.