Co-payment vs Co-insurance: Understanding the Key Differences in Health Insurance

Let’s face it—health insurance is confusing. It’s packed with jargon that sounds like it was invented just to make your eyes glaze over. And two of the most commonly misunderstood terms? Co-payment and co-insurance. You’ve probably seen these words while skimming through your insurance documents or when trying to figure out why your medical bill is higher than expected.

But here's the truth: understanding the difference between co-payment and co-insurance can save you a ton of money—and a mountain of frustration. These two cost-sharing terms play a huge role in how much you'll actually pay for your healthcare, beyond just your monthly premium. So, if you've ever wondered, "Why am I still paying more even though I have insurance?" — this article is for you.

In this deep dive, we’ll break down what each term means, how they work, when they apply, and which one might be better for your situation. Ready to finally make sense of co-pays and co-insurance? Let’s go.

What is Co-payment?

Co-payment, often shortened to co-pay, is a fixed amount you pay upfront for specific health care services. Think of it as the cover charge at a club—you pay a set fee just to get in, no matter what the drinks cost inside. That fee doesn’t fluctuate based on the cost of the service. Whether your doctor charges $120 or $200 for a visit, your co-pay stays the same.

For example, you might have a co-pay of:

$25 for a primary care visit

$50 for a specialist visit

$10 for a generic prescription drug

The beauty of co-pays is predictability. You know exactly how much you're going to pay when you walk into your doctor’s office or the pharmacy. No surprises. It's simple, which is why a lot of people prefer insurance plans with co-pays—they’re easy to budget for.

But here's the catch: co-pays usually don't kick in until after you've met your deductible (we'll talk more about that later). And not all services may require a co-pay. For some things—like hospital stays or surgeries—you may have to deal with co-insurance instead.

What is Co-insurance?

Now, let’s talk about co-insurance. Unlike co-payments, which are fixed fees, co-insurance is a percentage of the total cost of a healthcare service that you’re responsible for after you’ve met your deductible.

Let’s say your insurance policy has an 80/20 co-insurance split. That means your insurance company pays 80% of the cost, and you pay the remaining 20%. So if you have a $1,000 medical bill and your deductible has been met, you’re responsible for $200. That’s your co-insurance.

Some common co-insurance breakdowns include:

70/30

80/20

90/10

The downside? Costs can vary wildly depending on the type of service. You won’t know the exact amount you owe until you get the final bill. So while co-insurance might seem fair (you’re sharing costs with the insurer), it can be unpredictable—especially for major procedures or unexpected emergencies.

Unlike co-pays, co-insurance is more common with expensive services like hospitalizations, surgeries, or advanced imaging (MRI, CT scans). It’s the insurance company’s way of saying, “We’ll help, but you still need to pitch in.”

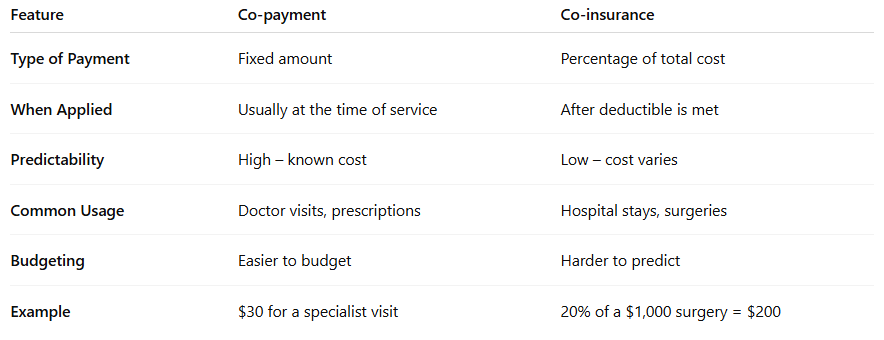

Key Differences Between Co-payment and Co-insurance

Let’s put these two side by side and break it down even further. Here's a table to visualize the differences:

See how different they are? While both are out-of-pocket costs, they work very differently and impact your wallet in unique ways. That’s why it’s crucial to understand both when shopping for insurance.

How Co-payment Works in Real-Life Scenarios

Let’s paint the picture. Imagine you’re feeling under the weather, so you schedule a visit to your primary care doctor. When you show up, the front desk asks for a $25 co-pay before you even see the doctor. That’s it. No mystery bill arriving weeks later, no math equations required—it’s clean, simple, and paid on the spot.

Now let’s look at a few more real-life examples where co-payments are commonly used:

Doctor Visits

Whether it’s a routine checkup, a sore throat, or a minor injury, co-pays apply the moment you step into most clinics. Your insurance might list something like:

$25 for primary care visits

$40 for specialists (like dermatologists or cardiologists)

No matter what the doctor charges your insurance company, your cost remains fixed.

Prescription Medications

Most plans divide prescription drugs into “tiers.” For example:

Tier 1 (Generic): $10 co-pay

Tier 2 (Preferred Brand): $25 co-pay

Tier 3 (Non-preferred Brand): $50 co-pay

So if you need antibiotics that fall into Tier 1, you just pay $10—even if the drug costs $90 retail. It’s a sweet deal when it works in your favor.

Emergency Room Visits

Here’s where co-pays can get a little painful. Some insurance plans have steep co-pays for ER visits—anywhere from $150 to $500. Why? To discourage unnecessary visits and encourage urgent care or primary care for non-emergencies. But remember, even after paying your ER co-pay, you could still be responsible for additional charges if the service is billed as “out-of-network” or not fully covered.

Bottom line? Co-pays are straightforward, make budgeting easier, and are especially helpful for those who make frequent doctor visits. But they don’t cover everything, and they often don’t apply until your deductible is met for certain services.

How Co-insurance Works in Real-Life Scenarios

Now let’s turn the tables and talk co-insurance. This is where things start to get a bit trickier—and more expensive—especially for larger medical services. Co-insurance doesn’t kick in until you’ve met your deductible. After that, it’s a shared cost arrangement between you and your insurer.

Let’s say you’ve met your deductible and you’re scheduled for a surgery that costs $5,000. If your plan has 80/20 co-insurance, you’ll pay 20%—that’s $1,000. Your insurance covers the remaining $4,000.

Hospital Stays

You’ve got to stay overnight in the hospital. Depending on your plan, you could be looking at co-insurance of 20% of the total cost. Hospital bills can skyrocket quickly, and 20% of a $10,000 stay means you're paying $2,000 out-of-pocket. Ouch, right?

Surgeries

Even outpatient procedures, like getting your tonsils removed or a minor orthopedic surgery, can cost thousands. With co-insurance, your share fluctuates with the service cost. So the more complex (and expensive) the surgery, the more you’ll pay—even with insurance.

Diagnostic Testing

Let’s say your doctor orders an MRI that costs $2,500. You’ve already met your deductible. With 20% co-insurance, that’s a $500 bill for you. And if you haven’t met your deductible yet? You could be paying the full amount upfront until you hit that threshold.

So what's the takeaway? Co-insurance is less predictable than co-pays. It’s harder to budget and can be a real wallet-buster during emergencies or major treatments. But it’s also the tradeoff for having lower monthly premiums in some plans.

The Role of Deductibles in Co-payment and Co-insurance

Let’s zoom in on one of the most important—and often overlooked—factors: the deductible. This is the amount you pay out-of-pocket before your insurance begins covering costs. It affects how both co-payments and co-insurance work.

How it Ties In

Co-payments: In some plans, you owe a co-pay even before you meet your deductible. Other plans won’t let you use co-pays until you’ve hit that threshold.

Co-insurance: This almost always kicks in after you’ve met your deductible.

For example, if your deductible is $1,500 and you have a $2,000 hospital bill:

You pay the first $1,500 in full (your deductible)

Then, co-insurance applies to the remaining $500

If your co-insurance is 20%, you pay $100 more

High-Deductible Health Plans (HDHPs)

These are designed to lower your monthly premium, but they come with higher deductibles (sometimes $5,000 or more). Until you meet that deductible, you’re covering the full cost of most services.

Understanding how deductibles fit into your plan is critical to avoiding surprises. People often make the mistake of thinking their insurance will pay immediately, only to get hit with a massive bill because they haven’t hit their deductible yet.

Understanding Out-of-Pocket Maximums

Now here’s the silver lining: every health insurance plan has an out-of-pocket maximum. This is the cap on how much you have to pay in a given year—including deductibles, co-pays, and co-insurance. Once you hit that number, your insurance covers 100% of any additional medical costs for the rest of the year.

Let’s say your plan’s out-of-pocket maximum is $6,000:

You pay your $2,000 deductible

You rack up another $4,000 in co-insurance and co-pays

That’s $6,000 total

After that? You pay nothing more for covered services that year

This limit is a life-saver in situations involving chronic illness, major surgeries, or accidents. Without it, medical debt would spiral out of control for many people.

Pros and Cons of Co-payment

Co-payments might seem like a godsend when you first look at them, especially if you’re the kind of person who likes predictability and hates surprise bills. But like anything else in the insurance world, they come with their own set of advantages and drawbacks.

Pros of Co-payment

Predictable Costs

You always know what you’ll be paying when you visit a doctor or pick up a prescription. That’s great for budgeting. Need to see your primary care physician once a month? That’s $25 each time. Easy.Encourages Preventive Care

Because co-pays are usually low, you’re more likely to go for checkups and address issues early—before they become expensive problems. Insurance companies love this too; it reduces their costs in the long run.Quick Transactions

Co-pays are typically paid at the time of service, which speeds up the billing process. You walk in, pay your fee, get treated, and go. No waiting around for a surprise bill later.More Affordable Day-to-Day Care

For people with ongoing conditions that require frequent visits to specialists or medications, co-pays keep those costs manageable.

Cons of Co-payment

Doesn’t Always Apply to Major Expenses

Co-pays don’t cover everything. Major services like hospital stays or advanced diagnostic testing often fall under co-insurance, leaving you with bigger bills than expected.Can Add Up Over Time

While a $30 co-pay doesn’t sound bad, if you’re visiting multiple doctors and specialists monthly, those fees can add up fast.Not Always Counted Toward Deductibles

Depending on your insurance provider, co-pays may not contribute to your annual deductible. That means you could still owe a lot before your full benefits kick in.Limited Transparency

While you know what you’ll pay for the visit, you might not realize that additional procedures during that visit aren’t included in the co-pay. Surprise charges can still happen.

Bottom line: co-pays are great for everyday care, but they won’t always protect you from big medical expenses.

Pros and Cons of Co-insurance

Now let’s flip the coin. Co-insurance comes with a very different structure, and whether you love it or hate it usually depends on how much medical care you need in a year.

Pros of Co-insurance

Shared Financial Responsibility

You’re not footing the entire bill alone. Once your deductible is met, your insurance helps out, which can be a huge relief for expensive procedures.May Result in Lower Premiums

Plans with higher co-insurance often come with lower monthly premiums. If you’re healthy and rarely see the doctor, this might save you money overall.Caps Through Out-of-Pocket Maximums

Co-insurance won’t bleed you dry forever. Once you hit your out-of-pocket max, you’re done paying—no matter how expensive the care gets after that.Better Coverage for Serious Events

If something major happens (like surgery or hospitalization), co-insurance ensures you’re only responsible for a percentage—rather than the entire cost—once deductibles are met.

Cons of Co-insurance

Unpredictable Costs

Unlike co-pays, you can’t always know what your share will be. Medical costs vary wildly between providers, regions, and procedures.Surprise Bills

If you haven’t met your deductible, you might be on the hook for the entire cost of care. People often forget this until the bill arrives.Hard to Budget For

Because you’re paying a percentage, it’s tough to plan your finances—especially in emergencies or for new diagnoses that require ongoing treatment.High Costs for Big Procedures

20% of $5,000 might not sound bad until you realize that’s still $1,000. And that’s just for one service. If you need follow-ups, rehab, or prescriptions, those costs can balloon fast.

In short, co-insurance is more “fair” in theory but riskier in practice if you’re not prepared or don’t have savings set aside.

Which is Better: Co-payment or Co-insurance?

Here’s the million-dollar question: Which one should you prefer?

Well… it depends.

Choose Co-payment If:

You visit doctors regularly for chronic conditions or maintenance

You value budget-friendly, predictable expenses

You’re looking for an easy-to-understand plan

Choose Co-insurance If:

You’re healthy and rarely use medical services

You want lower monthly premiums

You have an emergency fund or Health Savings Account (HSA) to handle unexpected costs

The “best” option really boils down to how often you seek care, your financial flexibility, and how much risk you’re willing to tolerate. For people who need regular treatments, co-pay-heavy plans can offer peace of mind. For the relatively healthy, co-insurance can save you money in the long run.

Pro tip? Hybrid plans that use both co-pays and co-insurance are common. So the real trick is to understand when each applies and plan accordingly.

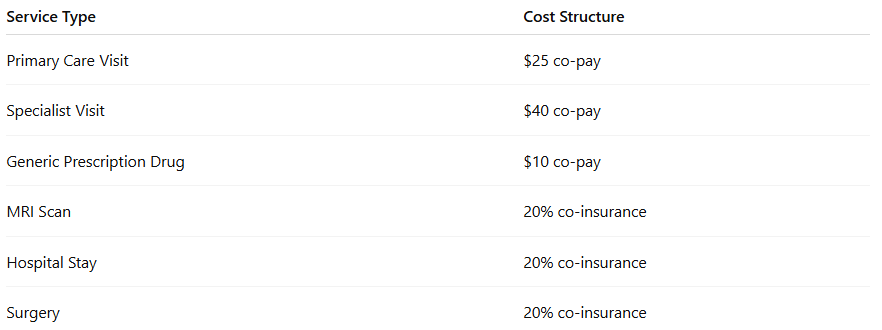

How Insurance Plans Mix Co-payments and Co-insurance

Most insurance plans don’t stick with one or the other. Instead, they create a blended structure that uses co-pays for some services and co-insurance for others.

Here’s a breakdown of how that might look:

Insurance companies design plans this way to balance affordability with risk. They know you’ll probably visit your primary care doc a few times a year—but they also want to share the cost of high-ticket services like surgeries and ER visits.

If you're evaluating different policies, be sure to read the fine print. Understand which services have co-pays, which fall under co-insurance, and how your deductible fits into it all.

Choosing the Right Plan Based on Co-payment or Co-insurance

Let’s get real—selecting a health insurance plan isn’t exactly a fun weekend activity. But if you want to avoid financial disasters down the line, choosing the right plan is crucial. And one of the biggest factors? How the plan handles co-payment and co-insurance.

So how do you decide?

Step 1: Assess Your Health Needs

Ask yourself:

Do you have chronic conditions that require regular doctor visits or prescriptions?

Are you planning any major surgeries or procedures?

Do you rarely see the doctor and consider yourself pretty healthy?

If you answered “yes” to frequent visits and medications, a co-pay-focused plan might save you money and reduce anxiety about surprise bills. But if you’re healthy and visit the doctor once a year (if that), you might benefit from a lower-premium plan with co-insurance.

Step 2: Examine Your Financial Flexibility

Do you have an emergency fund?

Can you cover a few thousand dollars in unexpected bills?

Would a high monthly premium strain your budget?

If you’re financially tight each month, you might prefer a lower-premium plan with higher co-insurance. But make sure you have some safety net. Those 20% medical bills add up fast in emergencies.

Step 3: Compare Plan Summaries

Every insurance provider offers a Summary of Benefits and Coverage (SBC). It breaks down:

Co-payments for doctor visits and prescriptions

Co-insurance rates for procedures and hospitalization

Deductibles

Out-of-pocket maximums

Use these summaries to compare apples to apples.

Step 4: Consider Your Preferred Providers

Some plans offer lower co-pays or co-insurance if you stay “in-network.” Always check whether your favorite doctors, hospitals, or clinics are covered under the plan. Going out-of-network can skyrocket your costs—especially under co-insurance structures.

Step 5: Think Long-Term

Maybe this year you’re healthy, but what about next year? Planning a pregnancy? Considering elective surgery? Aging parents? Life changes fast. Choose a plan that gives you flexibility without punishing you financially when things change.

Co-payment and Co-insurance in Different Types of Health Insurance

Not all health insurance is created equal. How co-payments and co-insurance are handled varies widely depending on the type of plan you have.

Let’s break it down.

Employer-Sponsored Health Plans

These are the most common in the U.S. Most employers subsidize a chunk of the premium and offer plans with:

Low co-pays for primary care and specialists

Reasonable co-insurance for major procedures

Out-of-pocket maximums to protect you

These plans often have more predictable structures and broader provider networks, which is why people generally prefer them.

Individual or Family Plans (Marketplace)

If you’re self-employed or don’t have job-sponsored insurance, you’ll likely buy a plan on the health insurance marketplace.

These plans vary widely. Some have:

Very low premiums but high deductibles and co-insurance

Others offer low co-pays but higher premiums

You’ll need to pay close attention to the metal tiers (Bronze, Silver, Gold, Platinum). Generally:

Bronze = Low premiums, high co-insurance

Platinum = High premiums, low co-pays/co-insurance

Medicare

Medicare comes with a completely different structure.

Medicare Part B involves co-insurance (typically 20%) for outpatient care after meeting the deductible.

Medicare Advantage Plans (Part C) often include fixed co-pays for most services.

Supplemental plans (Medigap) can help cover co-insurance costs not paid by Original Medicare.

Medicaid

Medicaid usually has very minimal or no co-payments and almost no co-insurance. It’s designed for low-income individuals and families, so cost-sharing is limited to protect beneficiaries.

But again—rules vary by state. Some states require small co-pays, especially for non-emergency services.

FAQs About Co-payment and Co-insurance

1. Can I have both co-payment and co-insurance in one plan?

Yes, most modern health insurance plans include both. For example, you may pay a co-pay for office visits and co-insurance for surgeries or hospital stays.

2. Do co-payments count toward my deductible?

Not always. It depends on your plan. Some plans count co-pays toward the deductible, while others only count them toward your out-of-pocket max.

3. How do I know which services are subject to co-pay or co-insurance?

Your insurance company provides a “Summary of Benefits and Coverage.” Review it carefully—it lists what’s covered, what’s not, and what cost-sharing applies.

4. Are co-insurance payments based on the provider’s price or the insurance’s allowed amount?

Co-insurance is based on the allowed amount, which is the rate negotiated between your insurer and the provider—not the provider’s retail price.

5. Which is cheaper in the long run—co-pay or co-insurance?

There’s no one-size-fits-all answer. If you have frequent, routine healthcare needs, co-pays might save you more. If you rarely need care, a co-insurance plan with lower premiums might be cheaper overall.

Conclusion

Health insurance is like a puzzle—and co-payment and co-insurance are two of the most important pieces. While both involve you sharing the cost of care with your insurance provider, they work in completely different ways. Co-pays offer simplicity and predictability, while co-insurance brings risk and flexibility into the mix.

Choosing the right type of cost-sharing comes down to understanding your own health, financial situation, and risk tolerance. Don’t just look at the premium. Dive deep into the co-pay and co-insurance details to get the full picture of what your healthcare will really cost you.

And remember—knowledge is power. The more you understand your health insurance, the better decisions you’ll make and the less likely you are to get blindsided by medical bills.

FAQs

1. What happens if I don’t meet my deductible—do I still pay co-insurance?

Nope. You typically have to meet your deductible before co-insurance kicks in. Until then, you’re responsible for the full cost of care (unless the service is covered without a deductible, like preventive care).

2. Are co-pays always required at the time of the visit?

Usually, yes. Most providers ask for co-pays upfront when you check in, especially for doctor visits and prescriptions.

3. Can I negotiate co-insurance charges with a provider?

Sometimes. While insurance companies set the allowed amount, providers may offer payment plans or discounts—especially for large bills. It never hurts to ask.

4. Does using an in-network provider affect co-insurance?

Absolutely. In-network providers have pre-negotiated rates. Out-of-network care may come with higher co-insurance—or might not be covered at all.

5. Do all insurance plans have co-pays and co-insurance?

Not always. Some high-deductible plans rely almost entirely on co-insurance. Others may use co-pays more heavily. Always check the plan details before signing up.

SOURCEs

https://www.healthcare.gov/glossary/

https://content.naic.org/consumer.htm

https://www.verywellhealth.com

Explore Group Health Insurance Solutions and Protect Your Team Today! Check out these helpful articles too: