Cobra Insurance: A Complete Guide to Understanding Your Health Coverage Options

What Is Cobra Insurance?

Definition and Origin of COBRA

If you’ve ever lost a job or experienced a reduction in work hours, you’ve probably heard the term COBRA insurance thrown around like a safety net. But what exactly is it? COBRA stands for the Consolidated Omnibus Budget Reconciliation Act, a U.S. federal law passed in 1985 that gives employees and their families the right to continue their group health insurance coverage after certain qualifying events. These events often include job loss (whether voluntary or involuntary), reduction in work hours, divorce, or even the death of the covered employee.

Think of COBRA as a temporary bridge. Imagine you’re crossing from one job to another, but there’s a gap in between. Instead of falling into the uncertainty of being uninsured, COBRA allows you to stay on your employer’s health plan for a limited time. That means you keep the same doctors, benefits, and coverage you had before—no sudden disruptions.

What makes COBRA particularly significant is that it applies to employers with 20 or more employees, ensuring that a large portion of the workforce has access to continued coverage. According to the U.S. Department of Labor, millions of Americans rely on COBRA each year to avoid gaps in health insurance. While it’s not always the cheapest option, its reliability and familiarity make it a popular choice during transitions.

In simple terms, COBRA is about continuity and stability in moments when life feels uncertain. It doesn’t replace your need for long-term insurance, but it gives you breathing room—something that’s incredibly valuable when you’re navigating major life changes.

How Cobra Insurance Works

Understanding how COBRA insurance works can feel a bit like reading the fine print of a complicated contract, but it’s actually more straightforward than it seems. When you experience a qualifying event—like losing your job—your employer is required to notify your health plan administrator. After that, you’ll receive a COBRA election notice explaining your rights and how to enroll.

Here’s where things get real: unlike employer-sponsored insurance where your company pays a portion of your premium, with COBRA, you pay the entire premium yourself, plus a small administrative fee (usually up to 2%). That means if your employer was covering 70% of your health insurance before, you’re now responsible for 100% of the cost. This is why many people are shocked when they see their COBRA premium for the first time.

But despite the cost, the process is relatively flexible. You typically have 60 days to decide whether to enroll after receiving your election notice. If you choose COBRA, your coverage is retroactive to the date you lost your previous insurance, ensuring no gap in coverage.

Another key detail is payment. You’ll need to make your first premium payment within 45 days of enrolling, and after that, payments are usually due monthly. Missing a payment can result in losing coverage entirely, so staying organized is crucial.

In essence, COBRA works like a continuation plan: same benefits, same network, but a different payment structure. It’s designed to give you time—time to find a new job, explore other insurance options, or simply regain stability. And while it may not be the most budget-friendly choice, it offers something priceless: peace of mind during uncertain times.

Who Is Eligible for Cobra Insurance?

Qualifying Events Explained

Eligibility for COBRA insurance isn’t random—it’s tied to specific life events known as qualifying events. These events trigger your right to continue your employer-sponsored health coverage, and understanding them can make all the difference when planning your next steps.

The most common qualifying event is job loss, whether you quit, were laid off, or even terminated (as long as it wasn’t due to gross misconduct). But that’s just the tip of the iceberg. Other qualifying events include a reduction in work hours that causes you to lose eligibility for health benefits, divorce or legal separation from the covered employee, and even the death of the employee who held the insurance.

For dependent children, qualifying events can also include aging out of a parent’s health plan, typically at age 26. Imagine being a recent college graduate, suddenly responsible for your own insurance—COBRA can act as a temporary cushion during that transition.

What’s important to remember is that these events must result in a loss of coverage under the employer’s plan. If your situation doesn’t lead to losing your health benefits, COBRA may not apply. Employers are required to notify the plan administrator within a certain timeframe after a qualifying event, and from there, the process begins.

Statistics show that job-related qualifying events account for the majority of COBRA enrollments, especially during economic downturns. For instance, during periods of high unemployment, COBRA participation tends to spike as more individuals seek to maintain their existing coverage.

In a way, qualifying events are like triggers that activate your safety net. They’re not always pleasant—often tied to stressful life changes—but they open the door to continued healthcare coverage when you need it most.

Covered Individuals Under COBRA

COBRA isn’t just for employees—it extends its protection to a broader group known as qualified beneficiaries. This includes not only the employee who was covered under the group health plan but also their spouse and dependent children. Each of these individuals has an independent right to elect COBRA coverage, which adds an extra layer of flexibility.

Let’s say an employee loses their job but decides not to continue coverage. Their spouse and children can still choose COBRA independently. This is especially important in situations like divorce or separation, where one party may lose access to the original health plan but still needs coverage.

Another interesting aspect is that COBRA treats each beneficiary separately when it comes to decisions and payments. That means a family could have a mix of coverage choices—some opting for COBRA while others explore alternative insurance options like marketplace plans.

Employers play a crucial role in notifying all qualified beneficiaries. Once a qualifying event occurs, the plan administrator must send out notices detailing each individual’s rights. From there, each person has the option to enroll or decline coverage.

This structure ensures that no one is left without options. It recognizes that healthcare needs vary from person to person, even within the same family. For example, a dependent child with ongoing medical treatments may benefit more from staying on COBRA, while a healthy spouse might opt for a more affordable marketplace plan.

In essence, COBRA’s coverage isn’t one-size-fits-all—it’s adaptable and inclusive, designed to meet the diverse needs of families during transitional periods.

Benefits of Cobra Insurance

Continuity of Coverage

One of the biggest reasons people turn to COBRA insurance—despite its higher cost—is the simple promise of continuity. Imagine you’re in the middle of ongoing treatment, maybe for a chronic condition like diabetes or something more serious like cancer. The last thing you want during a job transition is to switch doctors, restart deductibles, or risk disruptions in care. COBRA eliminates that uncertainty by allowing you to keep the exact same health insurance plan you had while employed.

This continuity isn’t just about convenience—it can be medically critical. Many treatments rely on consistent provider relationships and approved care plans. Switching insurance mid-treatment can lead to delays, denied claims, or even starting over with new providers who aren’t familiar with your case. With COBRA, your network of doctors, specialists, and hospitals remains unchanged, which can make a huge difference in outcomes and peace of mind.

Another often-overlooked benefit is how COBRA handles deductibles and out-of-pocket limits. If you’ve already met a portion of your annual deductible under your employer-sponsored plan, that progress carries over when you switch to COBRA. This can save you hundreds—or even thousands—of dollars compared to starting fresh with a new insurance plan.

From a psychological perspective, continuity also provides stability during what is often a stressful time. Losing a job or going through a major life event can feel like the ground is shifting beneath you. Keeping your health insurance consistent acts like an anchor, giving you one less thing to worry about.

In real-world terms, COBRA is like hitting the “pause” button on your insurance situation. It buys you time—time to evaluate new job opportunities, compare insurance options, or simply recover from a major life change without sacrificing your healthcare access.

Access to the Same Network and Providers

Healthcare isn’t just about coverage—it’s about relationships and trust. Over time, you build connections with doctors who understand your medical history, preferences, and concerns. COBRA insurance allows you to maintain those relationships without interruption, which is a major advantage compared to switching to a completely new plan.

Think about it: finding a new primary care physician or specialist isn’t always easy. You might face long wait times, limited availability, or the challenge of transferring medical records. With COBRA, none of that changes. You continue seeing the same providers, using the same facilities, and following the same care plans.

This is particularly valuable for individuals with complex or ongoing healthcare needs. For example, someone undergoing physical therapy after surgery or receiving mental health support benefits greatly from consistent care. Disrupting those services can set back progress and add unnecessary stress.

There’s also the issue of prescription medications. Different insurance plans have different formularies, meaning your medication might not be covered—or could cost significantly more—under a new plan. COBRA ensures that your current prescriptions remain covered under the same terms, avoiding unexpected expenses or the need to switch medications.

From a logistical standpoint, staying within the same network simplifies everything. There’s no need to verify whether your doctor is “in-network” or worry about surprise out-of-network charges. Everything continues as it was, just with a different payment responsibility.

In a world where healthcare can often feel complicated and fragmented, COBRA offers something refreshingly simple: consistency. It allows you to maintain control over your healthcare journey, even when other parts of your life are in flux.

Drawbacks of Cobra Insurance

High Premium Costs

Now let’s address the elephant in the room: COBRA insurance is expensive. There’s no sugarcoating it. When you were employed, your employer likely covered a significant portion of your health insurance premium—sometimes as much as 70% or more. With COBRA, that subsidy disappears, and you’re responsible for paying the full premium yourself, plus an additional administrative fee of up to 2%.

To put this into perspective, the average annual premium for employer-sponsored health insurance in the U.S. exceeded $23,000 for family coverage in recent years, according to the Kaiser Family Foundation. While employees typically paid only a fraction of that amount during employment, COBRA requires you to shoulder the entire cost. That can translate to hundreds or even thousands of dollars per month.

For someone who has just lost their job or experienced a reduction in income, these costs can feel overwhelming. It’s like going from sharing the bill at a restaurant to suddenly paying for the entire table. And unlike other insurance options, COBRA doesn’t offer income-based subsidies, which means the price remains the same regardless of your financial situation.

This is why many people view COBRA as a short-term solution rather than a long-term strategy. It’s often used as a bridge—something to rely on temporarily while exploring more affordable options like marketplace plans or new employer-sponsored coverage.

That said, the high cost doesn’t automatically make COBRA a bad choice. For some individuals, especially those with significant medical needs, the benefits of continuity and comprehensive coverage outweigh the financial burden. It becomes a question of value rather than just price.

Still, it’s essential to go into COBRA with your eyes wide open. Understanding the true cost—and how it fits into your budget—is crucial for making an informed decision.

Limited Duration of Coverage

Another important limitation of COBRA insurance is its temporary nature. It’s not designed to be a permanent solution, and the coverage period is strictly defined by law. For most qualifying events, COBRA coverage lasts up to 18 months, although certain circumstances can extend this period to 29 or even 36 months.

At first glance, 18 months might seem like plenty of time. But life has a way of moving quickly, especially during periods of transition. Before you know it, that window can close, leaving you scrambling to find alternative coverage.

Extensions are possible in specific situations, such as when a qualified beneficiary becomes disabled or experiences a second qualifying event. However, these extensions come with additional requirements and often higher premiums, making them less accessible for some individuals.

The limited duration means that COBRA should be viewed as a temporary safety net rather than a long-term plan. It’s like renting a place while you search for a permanent home—you wouldn’t want to stay there indefinitely, but it serves an important purpose in the meantime.

This time constraint also adds a layer of urgency to your decision-making. While you’re covered under COBRA, it’s wise to actively explore other options, such as employer-sponsored plans from a new job, health insurance marketplaces, or government programs like Medicaid.

The key takeaway here is that COBRA buys you time—but not forever. Using that time wisely can make all the difference in ensuring you have continuous, affordable health coverage in the long run.

Cobra Insurance Costs Explained

Premium Breakdown and Administrative Fees

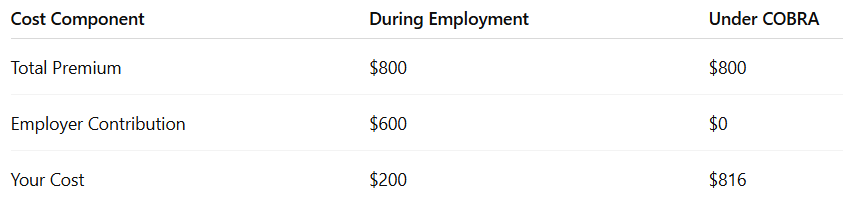

Understanding the cost structure of COBRA insurance is essential if you’re trying to decide whether it’s the right option for you. At its core, COBRA pricing is straightforward but often surprising. You’re responsible for paying 100% of the health insurance premium, plus an additional 2% administrative fee, which brings the total to 102% of the plan’s cost.

Let’s break that down in practical terms. When you were employed, your employer likely covered a significant portion of your premium. For example, if the total monthly cost of your health plan was $800, you might have only paid $200, with your employer covering the remaining $600. Under COBRA, you now pay the full $800—plus an extra $16 administrative fee—bringing your total to $816 per month.

Here’s a simple comparison:

This sudden increase can feel like a financial shock, especially if you’re already dealing with a loss of income. However, it’s important to remember that you’re paying for the same level of coverage, which often includes comprehensive benefits and a wide provider network.

Another detail to keep in mind is payment timing. COBRA allows a 45-day grace period for the first payment, but after that, monthly premiums must be paid on time to avoid losing coverage. There’s little room for error here—missing a payment could result in cancellation with no option for reinstatement.

While the numbers can be intimidating, having a clear understanding of how premiums are calculated helps you make a more informed decision. It’s not just about the price—it’s about what you’re getting in return.

Factors That Influence Costs

COBRA insurance costs aren’t entirely fixed—they can vary based on several factors tied to your specific situation and the plan you’re continuing. One of the biggest influences is the type of health plan you had through your employer. For instance, a comprehensive PPO plan with low deductibles will generally cost more than a high-deductible health plan (HDHP).

Another key factor is geographic location. Healthcare costs vary widely across the United States, and those regional differences are reflected in insurance premiums. If you live in an area with higher medical costs, your COBRA premiums are likely to be higher as well.

Age also plays a role. Older individuals typically face higher insurance premiums due to increased healthcare needs. While COBRA itself doesn’t adjust pricing based on age within a group plan, the underlying cost of the plan may already reflect age-related risk factors.

Family size is another important consideration. Covering a spouse and dependents significantly increases the total premium. A single individual might find COBRA manageable, while a family of four could face much higher monthly costs.

Lastly, changes in the employer’s health plan can impact your COBRA costs. If your former employer modifies the plan—such as increasing premiums or altering benefits—those changes will apply to your COBRA coverage as well.

All these variables make it clear that COBRA isn’t a one-size-fits-all solution. The cost you pay depends on a combination of factors, and understanding them can help you better evaluate whether COBRA aligns with your financial and healthcare needs.

How Long Does Cobra Coverage Last?

Standard Coverage Periods

When people first hear about COBRA insurance, one of the most common questions that pops up is: “How long can I actually stay on this plan?” The answer isn’t one-size-fits-all, but there are clear guidelines that determine how long your coverage can last. In most cases, COBRA provides up to 18 months of continued health insurance coverage following a qualifying event such as job loss or a reduction in work hours.

That 18-month window is essentially your transition period—a buffer zone where you can maintain your existing healthcare plan while figuring out your next move. Think of it like a temporary extension cord for your benefits. It keeps everything running smoothly while you plug into a new, more permanent solution.

However, not all qualifying events are treated equally. For example, if the qualifying event involves divorce, legal separation, or the death of the covered employee, COBRA coverage can extend up to 36 months for dependents. Similarly, if a dependent child loses coverage due to aging out of a parent’s plan, they may also qualify for up to 36 months of continuation coverage.

It’s important to note that the countdown starts from the date of the qualifying event—not from when you elect COBRA. This detail can catch people off guard, especially if they delay their enrollment decision. Even though COBRA allows retroactive coverage, the clock doesn’t reset.

Another nuance is that coverage can end earlier than expected if certain conditions occur. For instance, if you fail to pay your premiums on time, your COBRA coverage can be terminated immediately. Additionally, if your former employer stops offering a group health plan altogether, COBRA coverage may no longer be available.

In practical terms, understanding the timeline helps you plan ahead. Eighteen months might sound like a long time, but when you factor in job searches, financial adjustments, and life changes, it can pass quickly. That’s why it’s wise to treat COBRA as a temporary bridge rather than a destination.

Extensions and Special Circumstances

While the standard COBRA coverage period is fairly straightforward, there are specific situations where you may qualify for an extension. These extensions can provide additional months of coverage, but they come with conditions and sometimes higher costs.

One of the most common extensions occurs in cases of disability. If a qualified beneficiary is determined to be disabled by the Social Security Administration within the first 60 days of COBRA coverage, the coverage period can be extended from 18 months to 29 months. However, there’s a catch: during the additional 11 months, premiums can increase to 150% of the plan cost, making it significantly more expensive.

Another scenario involves what’s known as a second qualifying event. Let’s say you initially qualified for COBRA due to job loss, and then during your coverage period, you experience another event—such as divorce or the death of the covered employee. In such cases, dependents may be eligible to extend their coverage up to a total of 36 months from the date of the original qualifying event.

These extensions are helpful, but they’re not automatic. You must notify your plan administrator within a specific timeframe and provide the necessary documentation to qualify. Missing these deadlines can result in losing your eligibility for extended coverage.

There’s also an important financial consideration. While extensions provide more time, they often come with increased premiums, which can strain your budget. It’s like extending a hotel stay—convenient, but potentially costly if you’re not prepared.

Ultimately, extensions are designed to offer additional support during challenging circumstances, but they require careful planning and awareness. Knowing your options—and acting within the required timelines—can make a significant difference in maintaining uninterrupted health coverage.

How to Enroll in Cobra Insurance

Step-by-Step Enrollment Process

Enrolling in COBRA insurance might sound intimidating at first, but once you break it down, the process is fairly manageable. It follows a structured sequence designed to ensure you have enough time to make an informed decision without losing your coverage.

The process begins when a qualifying event occurs. Your employer is responsible for notifying the health plan administrator within a specific timeframe, typically within 30 days. Once that notification is processed, the plan administrator sends you a COBRA election notice, which outlines your rights, coverage options, and costs.

When you receive this notice, the clock starts ticking. You have 60 days to decide whether to enroll in COBRA coverage. This decision period is crucial because it allows you to compare COBRA with other options, such as marketplace insurance or coverage through a new employer.

If you decide to enroll, you’ll need to complete the election form provided in the notice. This form typically includes details about who in your family will be covered and the type of coverage you’re selecting. Once submitted, your COBRA coverage becomes retroactive to the date you lost your previous insurance, ensuring there’s no gap in coverage.

After enrolling, you have 45 days to make your first premium payment. This initial payment often covers the period from the date of the qualifying event to the current date, which can result in a larger upfront cost. Subsequent payments are usually due monthly.

The key to navigating this process smoothly is staying organized. Keep track of deadlines, maintain copies of all documents, and ensure your payments are made on time. Missing a deadline or payment can lead to losing coverage, and in most cases, there’s no second chance to reinstate it.

In essence, enrolling in COBRA is about following a clear roadmap. Each step builds on the previous one, and as long as you stay on track, the process is straightforward and reliable.

Important Deadlines to Remember

Deadlines are the backbone of the COBRA insurance process, and missing even one can have serious consequences. Unlike some aspects of healthcare that offer flexibility, COBRA operates on strict timelines that must be followed precisely.

The first critical deadline is the 60-day election period. This begins either from the date you receive your COBRA notice or the date your coverage would otherwise end—whichever is later. During this time, you must decide whether to enroll. If you miss this window, you lose your right to COBRA coverage entirely.

Next comes the 45-day payment deadline for your initial premium. This payment is essential to activate your coverage. Even though COBRA is retroactive, your coverage isn’t fully secured until this payment is made. Think of it as locking in your decision.

After the initial payment, ongoing premiums must be paid on a monthly basis. Most plans offer a 30-day grace period for these payments, but relying on that grace period can be risky. A missed payment can result in immediate termination of coverage, leaving you uninsured.

Another important timeline involves notifying the plan administrator of certain events, such as disability or a second qualifying event. These notifications must be made within specific timeframes—often within 60 days—to qualify for extensions.

Keeping track of these deadlines might feel overwhelming, especially during a stressful life transition. However, setting reminders, using calendars, or even writing down key dates can make a big difference.

In practical terms, think of COBRA deadlines as non-negotiable checkpoints. Staying ahead of them ensures that your coverage remains intact and that you avoid unnecessary complications during an already challenging time.

Cobra Insurance vs Other Health Insurance Options

Cobra vs Marketplace Insurance

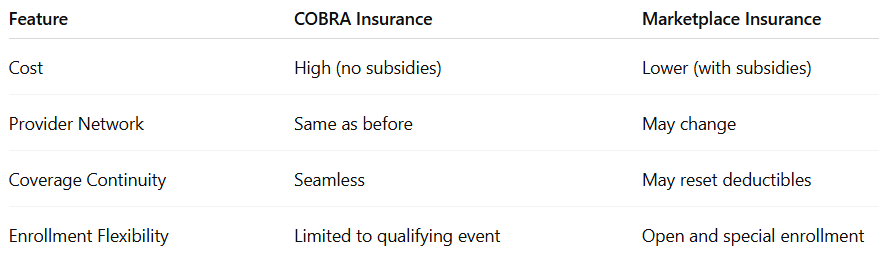

When deciding whether to choose COBRA insurance or a plan from the Health Insurance Marketplace, the choice often comes down to a balance between cost and convenience. COBRA offers familiarity—you keep your existing plan, doctors, and benefits—but it usually comes at a higher price.

Marketplace insurance, on the other hand, introduces variety and potential savings. Plans available through the Affordable Care Act (ACA) marketplace often come with income-based subsidies, which can significantly reduce monthly premiums. For many individuals, especially those who have recently lost income, these subsidies make marketplace plans far more affordable than COBRA.

However, affordability isn’t the only factor. Marketplace plans may have different provider networks, meaning your current doctors might not be included. You could also face new deductibles and out-of-pocket limits, essentially starting from scratch.

Here’s a quick comparison:

The decision often depends on your personal situation. If you’re in the middle of treatment or value continuity, COBRA might be worth the cost. If you’re relatively healthy and looking to save money, a marketplace plan could be a better fit.

Cobra vs Medicaid and Medicare

Comparing COBRA insurance with Medicaid and Medicare introduces a different perspective, as these programs serve specific populations and come with unique benefits.

Medicaid is designed for individuals and families with limited income. It often provides low-cost or even free coverage, making it an attractive alternative to COBRA for those who qualify. Unlike COBRA, Medicaid doesn’t require you to pay full premiums, but eligibility depends on income and state-specific guidelines.

Medicare, on the other hand, is primarily for individuals aged 65 and older or those with certain disabilities. If you’re eligible for Medicare, it often makes more sense to enroll in it rather than continue with COBRA, as Medicare typically offers more comprehensive and cost-effective coverage for that demographic.

One important detail is that COBRA doesn’t coordinate seamlessly with Medicare. Delaying Medicare enrollment while on COBRA can lead to late enrollment penalties, which can increase your healthcare costs in the long run.

In essence, while COBRA serves as a bridge, Medicaid and Medicare function as more permanent solutions for those who qualify. Understanding where you fit within these options can help you make a smarter, more sustainable choice.

Tips for Choosing the Right Health Coverage

Evaluating Your Healthcare Needs

Choosing the right health insurance after a major life change can feel like standing in front of a massive menu with no descriptions—everything looks important, but what actually fits your needs? Before automatically defaulting to COBRA insurance, it’s worth taking a step back and carefully evaluate your personal healthcare situation. This isn’t just about comparing prices; it’s about understanding how you actually use healthcare in your day-to-day life.

Start by asking yourself a few honest questions. Do you visit doctors frequently, or only for occasional checkups? Are you currently managing a chronic condition that requires ongoing treatment or prescriptions? If the answer is yes, COBRA might be a strong contender because it allows you to maintain continuity with your existing providers and treatment plans. On the other hand, if you’re generally healthy and rarely need medical care, a lower-cost marketplace plan with a higher deductible might make more financial sense.

Another key factor is your prescription medication needs. Medications can vary significantly in cost depending on the insurance plan’s formulary. With COBRA, you keep the same coverage, meaning your prescriptions are likely to remain consistent in both availability and pricing. Switching plans could introduce unexpected changes—higher co-pays, different covered drugs, or even the need for prior authorizations.

You should also think about your risk tolerance. Are you comfortable taking on a higher deductible in exchange for lower monthly premiums, or do you prefer predictable costs even if it means paying more upfront? COBRA typically offers more comprehensive coverage, which can reduce out-of-pocket surprises, but it comes with higher monthly costs.

Timing matters too. If you expect to secure a new job with benefits in the near future, COBRA can act as a short-term bridge. But if your employment situation is uncertain, exploring longer-term options might be more practical.

Ultimately, evaluating your healthcare needs is about aligning your insurance choice with your real-life habits and priorities. It’s not just a financial decision—it’s a strategic one that can impact your well-being, access to care, and peace of mind.

Cost-Saving Strategies

Let’s be real—health insurance costs can add up quickly, especially when you’re paying the full premium under COBRA. But here’s the good news: there are practical strategies you can use to reduce your overall expenses without sacrificing the coverage you need.

One of the smartest moves is to compare COBRA with marketplace plans as soon as you become eligible. Even if COBRA feels like the easiest option, marketplace plans may offer significant savings through subsidies, especially if your income has decreased. Taking the time to explore these options can potentially save you hundreds of dollars each month.

Another effective strategy is to use COBRA selectively. You don’t necessarily have to keep it for the entire coverage period. For example, you might start with COBRA to maintain continuity during a critical treatment phase, then switch to a more affordable plan once your situation stabilizes. This hybrid approach allows you to balance cost and care effectively.

If you do choose COBRA, consider adjusting your healthcare spending habits. Opt for generic medications when possible, use in-network providers, and take advantage of preventive care services that are often covered at no additional cost. Small changes like these can make a noticeable difference over time.

You can also explore Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs) if they’re available to you. These accounts allow you to set aside pre-tax dollars for medical expenses, effectively reducing your overall healthcare costs.

For those facing financial hardship, it’s worth checking whether you qualify for Medicaid or other state-based assistance programs. These programs can provide comprehensive coverage at a fraction of the cost—or even for free—depending on your eligibility.

Think of cost-saving strategies like fine-tuning a budget. It’s not about cutting corners on your health—it’s about making smarter choices that align with your financial reality. With a little planning and awareness, you can navigate this transition without feeling overwhelmed by expenses.

Conclusion

COBRA insurance stands as a crucial safety net in the complex world of healthcare coverage, հատկապես during times of uncertainty like job loss, life transitions, or unexpected changes in eligibility. It offers something that many alternatives can’t: seamless continuity. You keep your doctors, your plan, and your peace of mind—all without interruption. That consistency can be invaluable, especially when ongoing treatments or established provider relationships are at stake.

At the same time, COBRA isn’t without its challenges. The cost can be significantly higher than what you’re used to paying, and the coverage is inherently temporary. It’s designed to give you time—not to serve as a permanent solution. That’s why understanding how it works, who qualifies, and how it compares to other options is essential for making a well-informed decision.

The real power lies in using COBRA strategically. For some, it’s the perfect short-term bridge while transitioning to a new job or exploring other insurance plans. For others, it may not be the most cost-effective choice, especially when alternatives like marketplace plans or Medicaid are available.

What matters most is aligning your choice with your personal needs—your health, your finances, and your future plans. When you approach the decision thoughtfully, COBRA becomes more than just a fallback option; it becomes a tool that helps you stay in control during uncertain times.

FAQs About Cobra Insurance

1. Is COBRA insurance worth the cost?

COBRA insurance can absolutely be worth the cost, but it depends heavily on your individual circumstances. If you’re in the middle of ongoing medical treatment, have established relationships with healthcare providers, or want to avoid resetting deductibles, COBRA offers unmatched continuity. However, for those who are generally healthy and looking to minimize expenses, marketplace plans with subsidies may provide better value. The key is weighing the importance of stability against the financial impact.

2. Can I cancel COBRA coverage early?

Yes, you can cancel COBRA coverage at any time. There’s no requirement to keep it for the full duration of the coverage period. Many people use COBRA as a temporary solution and switch to another plan once they find a more affordable or suitable option. Just keep in mind that once you cancel COBRA, you typically can’t re-enroll, so it’s important to have another coverage plan lined up.

3. What happens if I miss a COBRA payment?

COBRA does offer a short grace period for monthly payments, usually around 30 days. However, if you fail to make your payment within that timeframe, your coverage can be terminated permanently. Unlike some other insurance options, COBRA doesn’t usually allow reinstatement after termination due to non-payment. Staying on top of deadlines is critical to maintaining your coverage.

4. Can I switch from COBRA to marketplace insurance?

Yes, you can switch from COBRA to a marketplace plan, but timing matters. You can enroll in a marketplace plan during the annual open enrollment period or if you qualify for a special enrollment period. Losing COBRA coverage (voluntarily or due to expiration) can trigger a special enrollment opportunity, allowing you to transition without a gap in coverage.

5. Does COBRA cover dental and vision insurance?

COBRA can include dental and vision coverage if those benefits were part of your employer-sponsored plan. Just like your medical insurance, you’ll need to pay the full premium for these additional coverages. While it increases your overall cost, it also ensures continuity for services like routine checkups, eyewear, and dental procedures.

SOURCEs

https://www.dol.gov/general/topic/health-plans/cobra

https://www.healthcare.gov/unemployed/cobra-coverage/

https://www.cms.gov/CCIIO/Programs-and-Initiatives/Other-Insurance-Protections/cobra_qna

https://www.kff.org/health-costs/report/2023-employer-health-benefits-survey/