What is Qualified Small Employer Health Reimbursement Arrangement (QSEHRA)

How QSEHRA Works

Employer Contributions Explained

When you strip away the legal jargon, QSEHRA works a lot like setting a monthly healthcare budget for your employees—except it comes with structured rules and powerful tax advantages. As an employer, you decide how much you’re willing to contribute toward each employee’s healthcare costs, and that contribution becomes the backbone of your QSEHRA plan.

Here’s where it gets interesting: unlike traditional group insurance, there’s no guessing game around rising premiums or unexpected renewals. You define a fixed monthly allowance, and that’s your maximum financial commitment. Whether you choose $200 or $800 per employee per month, the control stays entirely in your hands. This predictability is one of the biggest reasons small businesses gravitate toward QSEHRA.

However, it’s not a free-for-all. The IRS sets annual contribution limits, and employers must stay within those boundaries. Contributions can also vary based on family status (single vs. family), but they must be offered fairly across employees within the same class. In other words, you can’t randomly give one employee a significantly better deal without a valid structure behind it.

Another important detail: QSEHRA is entirely employer-funded. Employees cannot contribute to it, which simplifies administration but also places the responsibility squarely on the business. Think of it as a defined benefit with a defined cap—clean, controlled, and transparent.

Employers also have flexibility in how they structure reimbursements. You can choose to reimburse only health insurance premiums, or you can include other qualified medical expenses like prescriptions, doctor visits, or even mental health services. This flexibility allows you to tailor the benefit to your team’s needs without overcomplicating things.

In practice, many businesses use QSEHRA administration software to handle contributions, track reimbursements, and ensure compliance. It’s like having a digital assistant that keeps everything running smoothly behind the scenes. Without it, managing receipts, verifying expenses, and maintaining documentation could quickly become overwhelming.

So, if you’re picturing QSEHRA as a rigid system, think again. It’s more like a customizable framework—one that gives you control over costs while still offering meaningful support to your employees.

Employee Reimbursement Process

Now let’s flip the perspective. From the employee’s point of view, QSEHRA feels less like a corporate policy and more like a personal health spending account—except the money comes from their employer and is tax-free when used correctly.

The process starts with the employee purchasing their own health insurance plan. This could be through the Health Insurance Marketplace, a private insurer, or even a broker. The key requirement is that the coverage meets Minimum Essential Coverage (MEC) standards. Without MEC, reimbursements may become taxable, which defeats one of QSEHRA’s biggest advantages.

Once the employee has coverage, they can begin submitting expenses for reimbursement. This typically involves uploading proof—like a premium invoice or medical receipt—through an online portal or app. The employer (or a third-party administrator) reviews the submission to ensure it qualifies under IRS guidelines.

After approval, the reimbursement is issued—usually through payroll or direct deposit. And here’s the best part: these reimbursements are generally tax-free for both the employer and the employee. That’s a win-win scenario that traditional salary increases simply can’t match.

The system also encourages smarter healthcare decisions. Since employees are choosing their own plans and managing their own expenses, they tend to become more engaged and cost-conscious. It’s similar to how people shop differently when they’re spending their own money versus someone else’s.

There is, however, a learning curve. Employees need to understand what qualifies as an eligible expense, how to submit claims, and how their reimbursements interact with premium tax credits if they’re using the Marketplace. Clear communication from the employer is crucial here—otherwise, confusion can creep in.

In many ways, the reimbursement process is where QSEHRA truly shines. It transforms employees from passive participants in a company-selected plan into active decision-makers who can tailor their healthcare to their own lives.

Eligibility Requirements

Employer Eligibility Criteria

Not every business can jump on the QSEHRA bandwagon—and that’s by design. The program is specifically tailored for small employers, and the eligibility criteria reflect that focus.

To qualify, a business must have fewer than 50 full-time equivalent (FTE) employees. This threshold aligns with the Affordable Care Act’s definition of an “Applicable Large Employer” (ALE). Once a company crosses that 50-employee mark, it enters a different regulatory landscape and must consider other options like ICHRA or traditional group plans.

Another key requirement is that the employer cannot offer a group health insurance plan alongside QSEHRA. It’s an either-or situation. This rule ensures that QSEHRA remains a standalone benefit rather than a supplement to existing group coverage.

The plan must also be offered on equal terms to all eligible employees. While you can vary allowances based on family size or age (within limits), you can’t discriminate in a way that favors certain individuals unfairly. Think of it as leveling the playing field while still allowing some structured flexibility.

There are also administrative obligations. Employers must provide a formal written notice to employees at least 90 days before the start of the plan year. This notice outlines key details like allowance amounts and instructions for claiming reimbursements. Skipping this step can lead to penalties, so it’s not something to overlook.

In short, QSEHRA is designed for a very specific audience: small businesses that want to offer health benefits without the complexity of traditional insurance. If you fit that profile, it can be an incredibly effective tool—but stepping outside those boundaries can quickly lead to compliance issues.

Employee Eligibility Rules

From the employee side, eligibility is generally broad—but not entirely universal. Most full-time employees are eligible to participate in a QSEHRA, but employers can exclude certain categories, such as part-time workers, seasonal employees, or those under a certain age or tenure requirement.

For example, an employer might require employees to complete 90 days of service before becoming eligible. This helps prevent administrative headaches associated with high turnover, especially in industries like retail or hospitality.

One of the most critical requirements is that employees must have Minimum Essential Coverage (MEC) to receive tax-free reimbursements. Without it, any reimbursements they receive could be treated as taxable income. That’s a detail employees can’t afford to ignore.

There’s also an interesting interaction with premium tax credits. If an employee qualifies for subsidies through the Health Insurance Marketplace, their QSEHRA allowance can reduce or even eliminate those credits. This creates a bit of a balancing act, where employees need to evaluate which option provides the greatest financial benefit.

Communication is key here. Employers should make sure employees understand how QSEHRA works, what’s required of them, and how it impacts their individual situation. Without that clarity, even the best-designed plan can fall short.

Ultimately, QSEHRA eligibility rules aim to strike a balance between inclusivity and practicality. They ensure that the benefit is accessible while maintaining the structure needed for compliance and sustainability.

QSEHRA Contribution Limits

Annual Limits Set by IRS

One of the defining features of QSEHRA is its built-in financial boundaries, set annually by the IRS. These limits are crucial because they prevent the arrangement from becoming an open-ended liability for employers while still allowing meaningful contributions.

For 2026, contribution limits have continued to adjust with inflation. While exact figures may vary slightly year to year, they typically fall in the range of several thousand dollars annually for individual coverage and significantly higher for family coverage. For example, recent limits have hovered around $6,000–$7,000 for individuals and $12,000–$14,000 for families.

These caps represent the maximum allowable reimbursement, not a required amount. Employers can choose to offer less, depending on their budget and goals. This flexibility is what makes QSEHRA so appealing—it adapts to your financial reality rather than forcing you into a fixed structure.

It’s also worth noting that these limits are prorated monthly. So if an employee becomes eligible halfway through the year, their maximum allowance is adjusted accordingly. This ensures fairness and prevents over-allocation.

From a strategic standpoint, setting the right contribution level is key. Offer too little, and the benefit may not feel meaningful. Offer too much, and you risk straining your budget without maximizing ROI. It’s a balancing act that requires careful consideration.

Adjustments and Proration Rules

Proration is where things get a bit more nuanced—but also more logical once you understand the reasoning behind it. Essentially, QSEHRA allowances are calculated on a monthly basis, which allows for flexibility when employees join or leave mid-year.

Let’s say you offer $600 per month. If an employee becomes eligible in July, they would only have access to six months’ worth of reimbursements for that year. This ensures that benefits are distributed fairly and proportionally.

Adjustments can also occur when an employee’s family status changes. For instance, if someone gets married or has a child, their allowance may increase to reflect family coverage levels. These life events introduce a dynamic element to QSEHRA that traditional plans often struggle to accommodate.

Employers need to track these changes carefully and update allowances accordingly. This is another area where administration software can be incredibly helpful, automating adjustments and reducing the risk of errors.

Understanding proration isn’t just about compliance—it’s about fairness. It ensures that every employee receives benefits aligned with their actual period of eligibility, creating a system that feels both logical and equitable.

Tax Advantages of QSEHRA

Tax Benefits for Employers

If there’s one area where QSEHRA truly shines, it’s in the tax department. For small business owners trying to stretch every dollar, the tax efficiency of this arrangement can feel like finding an extra gear you didn’t know your engine had. Unlike traditional salary increases or bonuses—which are taxed heavily—QSEHRA contributions are 100% tax-deductible for employers.

What does that actually mean in practice? Every dollar you reimburse through QSEHRA reduces your taxable business income. So instead of simply increasing payroll expenses (and the associated payroll taxes), you’re channeling those funds into a structured benefit that delivers more value per dollar spent. It’s like getting a discount on employee compensation without reducing what your team receives.

There’s also the matter of payroll tax savings. QSEHRA reimbursements are not subject to FICA taxes (Social Security and Medicare), which can add up quickly if you’re managing a growing team. Over time, this creates a noticeable difference in your overall compensation costs compared to traditional wage increases.

Another underrated advantage is budget predictability. Because you define contribution limits upfront, you eliminate the volatility associated with group insurance premiums. No surprise hikes, no last-minute renegotiations—just a clear, controlled expense that fits neatly into your financial planning.

From a compliance standpoint, as long as you follow IRS rules and maintain proper documentation, QSEHRA remains a clean and efficient benefit structure. Many employers work with third-party administrators to ensure everything is handled correctly, reducing the risk of costly mistakes.

In essence, QSEHRA allows employers to optimize both cost and value simultaneously. You’re not just offering a benefit—you’re doing it in a way that aligns with smart financial strategy. And in a world where margins matter, that’s a powerful combination.

Tax Benefits for Employees

Now flip the lens to the employee side, and the tax advantages become even more compelling. Imagine receiving money from your employer to cover health expenses—and not having to pay income tax on it. That’s exactly what QSEHRA offers, provided certain conditions are met.

When employees maintain Minimum Essential Coverage (MEC), all eligible reimbursements they receive through QSEHRA are completely tax-free. This includes health insurance premiums and other qualified medical expenses under IRS Section 213(d). Compared to receiving a taxable salary increase, this is a significantly more efficient way to cover healthcare costs.

Think about it this way: if an employee receives a $5,000 salary raise, a portion of that disappears into federal and state taxes. But if that same $5,000 is provided through QSEHRA reimbursements, they get the full value—no deductions, no surprises. It’s a cleaner, more direct form of financial support.

However, there’s an important nuance involving premium tax credits. If an employee qualifies for subsidies through the Health Insurance Marketplace, their QSEHRA allowance may reduce or eliminate those credits. This creates a decision point: should they take the employer benefit, the subsidy, or a combination of both?

This is where things can get a bit tricky, and employees often benefit from consulting a tax advisor or using online calculators to determine the best option. Employers can help by providing clear guidance, but ultimately, the decision depends on each individual’s financial situation.

The bottom line? QSEHRA doesn’t just provide healthcare support—it does so in a way that maximizes take-home value. For employees, that’s not just a perk; it’s a meaningful financial advantage that can make a real difference in their day-to-day lives.

QSEHRA vs Other Health Reimbursement Arrangements

QSEHRA vs ICHRA

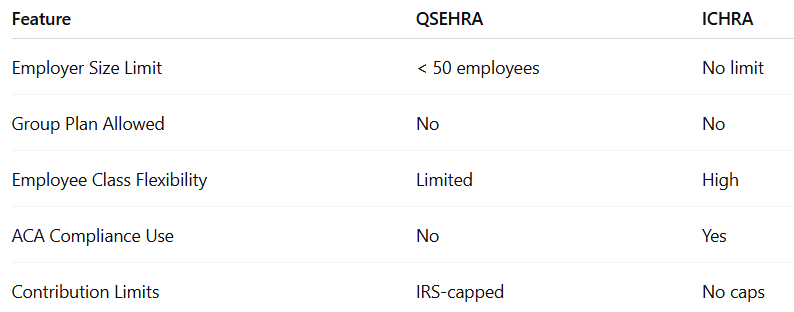

At first glance, QSEHRA and ICHRA (Individual Coverage Health Reimbursement Arrangement) might seem like close cousins—and in many ways, they are. Both allow employers to reimburse employees for individual health insurance premiums and medical expenses. But when you look closer, the differences start to matter, especially as your business grows.

The most obvious distinction lies in eligibility. QSEHRA is specifically designed for businesses with fewer than 50 full-time employees, while ICHRA has no such limit. This makes ICHRA a more scalable option for larger organizations or companies planning rapid growth.

Another key difference is flexibility in employee classes. ICHRA allows employers to create different classes of employees (such as full-time, part-time, or remote workers) and offer different reimbursement levels to each group. QSEHRA, on the other hand, requires more uniformity, with only limited variation based on family status.

There’s also a difference in how these arrangements interact with the Affordable Care Act. ICHRA can be used by larger employers to satisfy employer mandate requirements, while QSEHRA cannot. This makes ICHRA a more strategic choice for companies approaching or exceeding the 50-employee threshold.

Here’s a quick comparison to make things clearer:

Choosing between the two often comes down to your company’s size, growth trajectory, and how much customization you need. For small businesses just starting out, QSEHRA offers simplicity and structure. For larger or more complex organizations, ICHRA provides greater flexibility and scalability.

QSEHRA vs Traditional Group Insurance

Comparing QSEHRA to traditional group health insurance is like comparing a custom-built solution to an off-the-shelf package. Both have their place, but they serve different needs and priorities.

With group insurance, the employer selects a plan (or a few options), negotiates premiums, and shares costs with employees. This model offers familiarity and simplicity from the employee’s perspective, but it comes with significant downsides—especially for small businesses. Premiums can be unpredictable, plan options are limited, and administrative complexity can become overwhelming.

QSEHRA flips that model. Instead of choosing a plan, the employer sets a defined contribution, and employees select their own coverage. This creates a more personalized experience while giving employers tighter control over costs.

Another major difference is portability. Group insurance is tied to employment, meaning employees typically lose coverage when they leave the company. With QSEHRA, employees own their individual plans, so they can keep their coverage regardless of job changes.

Cost structure is another critical factor. Group plans often involve shared premiums, deductibles, and co-pays, which can add up quickly. QSEHRA, by contrast, allows employers to cap their spending while still offering meaningful support.

That said, group insurance does have its advantages. It can provide a sense of stability and may offer broader coverage networks in some cases. For certain industries or employee demographics, that consistency can be valuable.

Ultimately, the choice between QSEHRA and traditional insurance comes down to priorities: flexibility vs. familiarity, cost control vs. standardization. For many small businesses in 2026, flexibility is winning.

Pros and Cons of QSEHRA

Key Advantages

Let’s be honest—no healthcare solution is perfect. But QSEHRA comes pretty close for small businesses looking for a balance between affordability and effectiveness. Its advantages aren’t just theoretical; they play out in real-world scenarios every day.

One of the biggest wins is cost control. You decide how much to contribute, and that’s the end of the story. No surprise premium increases, no hidden fees—just a predictable expense that fits your budget.

Then there’s flexibility. Employees aren’t stuck with a one-size-fits-all plan. They can choose coverage that aligns with their personal needs, whether that’s a high-deductible plan with lower premiums or a more comprehensive option.

Another major advantage is tax efficiency. Both employers and employees benefit from tax savings, making QSEHRA a financially smart choice on both sides.

There’s also the matter of employee satisfaction. Giving people control over their healthcare decisions can lead to higher engagement and overall happiness. It’s like the difference between being handed a meal and being allowed to choose from a menu—you’re more likely to enjoy the outcome when you have a say in it.

Finally, QSEHRA is relatively easy to administer, especially with modern software solutions. Automation handles much of the heavy lifting, from tracking reimbursements to ensuring compliance.

Potential Drawbacks

Of course, QSEHRA isn’t without its limitations. Ignoring these would be like only reading the highlights of a contract—you need the full picture to make an informed decision.

One of the main drawbacks is the contribution cap. Because the IRS sets limits, employers can’t offer unlimited reimbursements. For some businesses, especially those in high-cost healthcare markets, this can feel restrictive.

Another challenge is the lack of group bargaining power. Employees are purchasing individual plans, which may not always offer the same pricing or network advantages as group insurance.

There’s also a learning curve. Employees need to understand how to choose a plan, submit expenses, and navigate reimbursement rules. Without proper guidance, this can lead to confusion or underutilization of benefits.

Additionally, QSEHRA cannot be combined with a group health plan. For businesses that want to offer both, this creates a limitation that may require exploring alternatives like ICHRA.

Lastly, compliance still matters. While QSEHRA is simpler than many traditional options, it’s not completely hands-off. Employers must follow IRS rules, provide notices, and maintain proper documentation.

Understanding these drawbacks doesn’t diminish QSEHRA’s value—it simply helps you use it more effectively.

How to Set Up a QSEHRA

Step-by-Step Implementation

Setting up a QSEHRA might sound like something that requires a legal team, a benefits consultant, and a week of uninterrupted focus—but in reality, it’s much more approachable when broken down into clear steps. Think of it less like assembling a complex machine and more like following a well-structured recipe. Each step builds on the previous one, and by the end, you’ve created a fully functional, compliant health benefit for your team.

The process begins with defining your budget and contribution strategy. This is where you decide how much you’re willing to reimburse employees each month or year. It’s not just a financial decision—it’s also a strategic one. Are you trying to attract top talent? Retain your current team? Offer a baseline benefit? Your goals will shape the numbers you choose.

Next comes plan design. You’ll determine whether reimbursements will cover only insurance premiums or include additional medical expenses. You’ll also decide if allowances will vary based on family size. This step is crucial because it defines how flexible and valuable your QSEHRA will feel to employees.

Once the structure is in place, you’ll need to create formal plan documents. These aren’t optional—they’re required by the IRS. The documents outline how the plan works, who’s eligible, and how reimbursements are handled. Many employers use third-party administrators or software platforms to generate these documents automatically, which reduces the risk of errors.

After that, it’s time to notify your employees. The IRS requires that you provide written notice at least 90 days before the plan starts (or as soon as possible for new hires). This notice should clearly explain how QSEHRA works, what employees need to do, and how it affects things like tax credits.

Then comes the operational phase: managing reimbursements. Employees submit proof of expenses, and you approve and reimburse them accordingly. This is where automation tools can save you hours of manual work, ensuring everything runs smoothly and stays compliant.

Finally, you’ll want to monitor and adjust your plan over time. Are employees using the benefit? Are contribution levels appropriate? A QSEHRA isn’t a “set it and forget it” system—it’s something you can refine as your business evolves.

When you look at it step by step, setting up a QSEHRA becomes far less intimidating. It’s a structured process, yes—but one that’s entirely manageable with the right approach and tools.

Compliance and Documentation

If QSEHRA were a game, compliance would be the rulebook—and it’s not something you can afford to skim. While the arrangement is designed to simplify health benefits, it still operates within a framework of IRS regulations that must be followed carefully.

The cornerstone of compliance is having proper plan documentation. This includes a formal written plan that outlines all the details of your QSEHRA. It’s not just a formality—it’s a legal requirement. Without it, your plan could be considered non-compliant, which may lead to penalties.

Another critical element is the employee notice requirement. Employers must provide a written notice that includes specific information, such as the employee’s allowance and instructions for maintaining Minimum Essential Coverage (MEC). Missing this step can result in fines, so it’s important to treat it as a priority.

You’ll also need to ensure that all reimbursements are for qualified medical expenses. This means verifying receipts and maintaining records. It might sound tedious, but it’s essential for preserving the tax-free status of the benefit.

There’s also the matter of reporting. Employers must report QSEHRA benefits on employees’ W-2 forms, even though the reimbursements are not taxable. This adds another layer of administrative responsibility that needs to be handled correctly.

Because of these requirements, many businesses choose to work with QSEHRA administration platforms. These tools automate documentation, track compliance, and reduce the risk of human error. It’s like having a built-in safety net that ensures everything stays within the rules.

Compliance isn’t the most exciting part of QSEHRA—but it’s arguably the most important. When handled properly, it allows you to enjoy all the benefits of the arrangement without worrying about legal or financial complications.

Common Mistakes to Avoid with QSEHRA

Compliance Pitfalls

Even though QSEHRA is designed to be simpler than traditional health plans, it’s not immune to mistakes. And when those mistakes involve compliance, the consequences can be more than just inconvenient—they can be costly.

One of the most common pitfalls is failing to provide proper documentation. Without a formal plan document, your QSEHRA doesn’t meet IRS requirements. It’s like trying to drive without a license—you might get away with it for a while, but eventually, it catches up with you.

Another frequent issue is missing the employee notice deadline. This might seem like a small administrative detail, but the IRS takes it seriously. Late or incomplete notices can result in penalties, which defeats the purpose of choosing a cost-effective benefit in the first place.

There’s also the risk of reimbursing ineligible expenses. Not every healthcare-related cost qualifies under IRS rules, and approving the wrong expense can jeopardize the tax-free status of the entire arrangement. This is why verification and record-keeping are so important.

Some employers also overlook the requirement to report QSEHRA benefits on W-2 forms. Even though the reimbursements aren’t taxable, they still need to be documented properly. Skipping this step can lead to confusion and potential compliance issues.

These pitfalls aren’t inevitable—they’re preventable with the right systems and attention to detail. But they highlight an important truth: even a “simple” benefit like QSEHRA requires discipline and structure to get right.

Strategic Errors Businesses Make

Beyond compliance, there’s another layer of mistakes that’s more subtle—but just as impactful. These are the strategic missteps that can limit the effectiveness of your QSEHRA, even if everything is technically done correctly.

One common error is setting contribution levels too low. While it’s tempting to minimize costs, offering a benefit that doesn’t meaningfully help employees can backfire. It may be technically compliant, but it won’t move the needle in terms of satisfaction or retention.

On the flip side, some businesses set contributions too high without fully considering long-term sustainability. This can create financial strain, especially if the company grows quickly or faces economic challenges.

Another mistake is poor communication. QSEHRA requires employees to take an active role in their healthcare decisions, and without clear guidance, they may feel overwhelmed or confused. This can lead to underutilization of the benefit, which defeats its purpose.

There’s also the issue of not leveraging technology. Trying to manage QSEHRA manually can lead to errors, inefficiencies, and unnecessary stress. Modern tools exist for a reason—they simplify administration and improve accuracy.

Finally, some businesses fail to review and adjust their plans over time. A QSEHRA that worked perfectly two years ago might not be as effective today. Regular evaluation ensures that your benefit continues to align with your goals and your employees’ needs.

Avoiding these strategic errors isn’t about perfection—it’s about awareness. When you understand where things can go wrong, you’re far better equipped to make them go right.

Conclusion

QSEHRA represents a shift in how small businesses approach healthcare benefits—moving away from rigid, one-size-fits-all solutions toward something far more adaptable and human-centered. It gives employers control over costs while giving employees control over their choices, and that balance is what makes it so compelling in today’s workplace.

For businesses operating with tight budgets and big ambitions, QSEHRA offers a way to compete without overextending. It’s not just about saving money—it’s about using resources more intelligently. And for employees, it transforms healthcare from a passive benefit into an active decision-making process.

The real power of QSEHRA lies in its simplicity and flexibility. When implemented thoughtfully and managed correctly, it becomes more than just a benefit—it becomes a strategic advantage.

FAQs

1. What does QSEHRA stand for?

QSEHRA stands for Qualified Small Employer Health Reimbursement Arrangement, a program that allows small businesses to reimburse employees for healthcare expenses tax-free.

2. Who is eligible for QSEHRA?

Employers with fewer than 50 full-time employees who do not offer group health insurance can set up a QSEHRA. Employees must meet eligibility criteria and have Minimum Essential Coverage.

3. Are QSEHRA reimbursements taxable?

No, reimbursements are generally tax-free for both employers and employees, as long as the employee maintains qualifying health coverage.

4. Can QSEHRA be used with Marketplace subsidies?

Yes, but it may reduce or eliminate eligibility for premium tax credits. Employees should evaluate which option is more beneficial.

5. How is QSEHRA different from ICHRA?

QSEHRA is limited to small employers and has contribution caps, while ICHRA offers more flexibility and is available to businesses of any size.

SOURCEs

https://www.irs.gov/publications/p969

https://www.irs.gov/pub/irs-drop/n-17-67.pdf

https://www.healthcare.gov/glossary/minimum-essential-coverage/

https://www.congress.gov/bill/114th-congress/house-bill/34

https://www.peoplekeep.com/qsehra

https://www.takecommandhealth.com/qsehra-guide