ICHRA Explained: A Modern Approach to Employee Health Benefits

What is ICHRA?

Definition and Core Concept

If you’ve ever felt like traditional employer-sponsored health insurance is too rigid, too expensive, or just plain outdated, you’re not alone. That frustration is exactly where ICHRA (Individual Coverage Health Reimbursement Arrangement) steps in and flips the script. Instead of employers choosing a one-size-fits-all group plan, ICHRA allows businesses to give employees a set allowance of tax-free money to purchase their own individual health insurance. Sounds simple, right? But beneath that simplicity lies a powerful shift in how healthcare benefits are structured.

Think of ICHRA like giving employees a health benefits wallet instead of a preselected meal. Rather than being told, “This is your plan, take it or leave it,” employees get the freedom to shop on the individual marketplace and choose coverage that actually fits their needs—whether that’s a low premium plan, a family-focused policy, or something in between. Employers reimburse those expenses, making it a win-win scenario.

What makes ICHRA particularly appealing is its adaptability. It doesn’t matter if a company has five employees or five hundred—this model scales effortlessly. Employers can define contribution amounts based on classes of employees, such as full-time, part-time, or seasonal workers. This level of customization is something traditional group plans simply can’t match.

At its core, ICHRA is about shifting control. Instead of employers bearing the burden of selecting and managing complex insurance plans, they define budgets. Instead of employees being passive recipients, they become active decision-makers. In a world where personalization is everything—from Netflix recommendations to fitness plans—ICHRA brings that same philosophy to healthcare.

How ICHRA Differs from Traditional Group Health Plans

Traditional group health insurance has long been the default option for businesses, but let’s be honest—it’s not always ideal. Employers typically choose a single plan (or a limited set of plans), negotiate with insurers, and then offer those options to employees. While this model works in some cases, it often leaves employees stuck with coverage that doesn’t align with their personal or family needs.

ICHRA completely changes that dynamic. Instead of managing a group policy, employers simply decide how much they want to contribute. Employees then go out and purchase their own insurance through the individual market or exchanges. This creates a more decentralized system where each person gets exactly what they need.

One major difference lies in cost predictability. With traditional group plans, premiums can fluctuate year after year, often increasing unexpectedly. That unpredictability can wreak havoc on a company’s budget. ICHRA, on the other hand, gives employers full control over how much they spend. They set the allowance, and that’s it—no surprises.

Another key distinction is portability. With group insurance, employees typically lose coverage when they leave a job. With ICHRA, the insurance policy belongs to the individual, not the employer. That means employees can keep their coverage even if they switch jobs, creating a sense of continuity that’s often missing in traditional setups.

There’s also the matter of inclusivity. Group plans often struggle to accommodate diverse employee needs—think freelancers, remote workers, or employees spread across different states. ICHRA thrives in these scenarios because it doesn’t rely on a centralized plan. Everyone can choose coverage available in their own region.

In many ways, comparing ICHRA to traditional group insurance is like comparing streaming services to cable TV. One gives you flexibility, control, and personalization; the other offers a fixed package that may or may not fit your preferences. As businesses continue to evolve, it’s no surprise that more are leaning toward the flexibility that ICHRA provides.

History and Evolution of ICHRA

Regulatory Background

To really understand why ICHRA exists, you have to look at the regulatory landscape that shaped it. Before ICHRA came into play, employers had limited options when it came to reimbursing employees for individual health insurance. In fact, earlier attempts to do so often ran into compliance issues with the Affordable Care Act (ACA), which imposed strict rules on employer-sponsored health benefits.

For a while, this created a kind of stalemate. Employers wanted flexibility, but regulations kept pushing them toward traditional group plans. Then came the introduction of Qualified Small Employer HRAs (QSEHRAs) in 2017, which allowed small businesses to reimburse employees for individual coverage—but with strict limitations on company size and contribution amounts.

ICHRA emerged in 2020 as a more flexible and scalable solution. The U.S. Departments of Treasury, Labor, and Health and Human Services jointly created rules that allowed employers of any size to offer tax-free reimbursements for individual health insurance, as long as certain conditions were met. This was a game-changer.

What made ICHRA particularly significant was its ability to satisfy the ACA’s employer mandate. Large employers (those with 50 or more full-time employees) are required to offer affordable health coverage or face penalties. ICHRA provided a way to meet that requirement without relying on traditional group plans, opening the door for widespread adoption.

The regulatory framework also introduced the concept of employee classes, allowing employers to offer different reimbursement amounts to different groups of workers. This added a layer of strategic flexibility that businesses had been craving for years.

In essence, ICHRA wasn’t just a new option—it was the result of years of policy evolution aimed at balancing flexibility with compliance. It bridged the gap between employer needs and regulatory requirements, creating a solution that works in the real world.

Why ICHRA Was Introduced

The introduction of ICHRA wasn’t random—it was a direct response to growing dissatisfaction with the traditional health insurance model. Employers were facing rising premiums, complex administration, and limited flexibility. Employees, meanwhile, were increasingly demanding more personalized benefits.

Healthcare costs have been climbing steadily for decades. According to industry data, employer-sponsored family health insurance premiums have increased by over 50% in the past decade alone. That kind of growth isn’t sustainable for many businesses, especially small and mid-sized companies trying to compete for talent while managing tight budgets.

ICHRA was designed to address these pain points head-on. By shifting from a defined-benefit model (where employers promise a specific insurance plan) to a defined-contribution model (where employers set a budget), businesses gain control over costs. It’s a bit like switching from an all-you-can-eat buffet to a prepaid card—you decide how much you’re willing to spend upfront.

Another major driver was workforce diversity. Today’s employees aren’t all sitting in the same office, working the same hours, or living in the same city. Remote work, gig economy roles, and multi-state teams have made it harder for group plans to keep up. ICHRA offers a solution that adapts to this new reality by letting employees choose plans available in their own location.

There’s also a philosophical shift at play. Modern employees value autonomy and choice more than ever. Whether it’s choosing their own work schedule or customizing their benefits, people want options. ICHRA aligns perfectly with this mindset by giving employees control over their healthcare decisions.

Ultimately, ICHRA was introduced to bring flexibility, transparency, and sustainability to a system that was struggling to keep up with modern demands. And judging by its growing adoption, it’s doing exactly that.

How ICHRA Works

Employer Contributions Explained

At the heart of ICHRA lies a concept that feels almost refreshingly straightforward: employers decide how much they’re willing to contribute, and that’s the budget—no hidden surprises, no unpredictable premium hikes sneaking up at renewal time. Instead of negotiating complex insurance contracts every year, businesses define a monthly allowance for employees. This allowance is entirely employer-funded and can vary based on employee classes such as full-time, part-time, seasonal, or even geographic location.

Now, here’s where it gets interesting. Unlike traditional plans that lock everyone into the same structure, ICHRA allows employers to tailor contributions with precision. For example, a company might offer higher reimbursements for employees with families and lower ones for single employees. It’s not about favoritism—it’s about aligning benefits with real-world needs. This flexibility creates a more balanced and efficient allocation of resources.

Another major advantage is cost control. Employers aren’t at the mercy of insurance carriers dictating next year’s premiums. If a business decides it can afford $400 per employee per month, that’s the limit. This predictability is a huge relief, especially for small and mid-sized companies trying to manage cash flow without sacrificing employee benefits.

There’s also a strategic layer to how contributions are structured. Businesses can design their ICHRA offerings to meet Affordable Care Act (ACA) requirements, ensuring that the coverage is considered “affordable” and avoids potential penalties. This makes ICHRA not just a flexible option, but a compliant one for larger organizations.

Think of employer contributions in ICHRA like setting a benefits budget rather than buying a fixed product. Instead of saying, “Here’s the plan we chose,” employers are saying, “Here’s what we’re investing in your health—now choose what works best for you.” That subtle shift changes everything, creating a system that feels more modern, transparent, and aligned with how people actually live and work today.

Employee Reimbursement Process

Once the employer sets the allowance, the spotlight shifts to employees—and this is where ICHRA truly shines. Employees go out and purchase their own individual health insurance plans, either through public marketplaces like Healthcare.gov or private insurers. The key requirement? The plan must meet minimum essential coverage (MEC) standards.

After securing coverage, employees submit proof of their insurance and eligible medical expenses to the employer or a third-party administrator. These expenses can include monthly premiums, prescriptions, and other qualified healthcare costs. Once verified, the employer reimburses the employee up to their allocated allowance—and here’s the best part: these reimbursements are tax-free.

The process might sound administrative, but in practice, it’s often streamlined through digital platforms that automate claims submission and approval. Many companies partner with ICHRA administrators who handle compliance, documentation, and reimbursements, making the experience smooth for both employers and employees.

From the employee’s perspective, this model offers a sense of ownership. Instead of being passively enrolled in a plan, they actively choose coverage that fits their lifestyle. Maybe someone prefers a high-deductible plan with lower premiums because they rarely visit the doctor. Another employee might opt for comprehensive coverage due to ongoing medical needs. ICHRA accommodates both without forcing a compromise.

There’s also a psychological benefit here. When employees see exactly how much their employer is contributing—and how those funds are used—it creates a stronger sense of value. It’s not just a vague “benefits package” anymore; it’s tangible support they can see and manage.

In many ways, the reimbursement process mirrors how modern financial tools work—transparent, flexible, and user-driven. And in a world where people are used to managing everything from banking to shopping through apps, this approach feels intuitive rather than complicated.

Key Features of ICHRA

Flexibility and Customization

If there’s one word that defines ICHRA, it’s flexibility. Traditional health plans often feel like trying to fit everyone into the same pair of shoes—some people manage, but many end up uncomfortable. ICHRA flips that idea by letting each employee pick their own “fit,” while employers design the overall framework.

One of the standout features is the ability to create employee classes. Employers can segment their workforce into categories—full-time, part-time, remote workers, salaried staff, hourly employees—and offer different reimbursement levels to each group. This isn’t just convenient; it’s strategic. Businesses can align benefits with workforce structure without violating regulations, as long as they follow class rules properly.

Customization also extends to geographic differences. Imagine a company with employees in both New York and a smaller rural town. The cost of health insurance can vary dramatically between these locations. With ICHRA, employers can adjust allowances to reflect these differences, ensuring fairness without overpaying or under-supporting certain groups.

Another layer of flexibility comes from plan choice. Employees aren’t limited to a narrow selection curated by HR. They can explore a wide range of options on the individual market, comparing premiums, deductibles, provider networks, and coverage levels. This turns health insurance from a static benefit into a personalized experience.

Even timing can be flexible. Employers can choose when to implement ICHRA and how reimbursement cycles work, allowing them to integrate it smoothly into their existing operations. It’s not a rigid system—it adapts to the business, not the other way around.

This level of customization is one of the main reasons ICHRA is gaining traction. In a workplace where personalization is increasingly expected—from flexible schedules to remote work options—it only makes sense that healthcare benefits follow the same trend.

Tax Advantages

Let’s talk about one of the most compelling aspects of ICHRA: tax efficiency. Both employers and employees benefit from significant tax advantages, making it not just a flexible option, but a financially smart one.

For employers, contributions made through ICHRA are tax-deductible business expenses. This reduces overall taxable income while still providing meaningful benefits to employees. It’s a straightforward way to invest in workforce well-being without increasing tax burden.

Employees, on the other hand, receive reimbursements that are completely tax-free, as long as they maintain qualifying health coverage. That means no federal income tax, no payroll tax—just pure value. Compare that to a salary increase, which would be taxed before it even reaches the employee’s pocket, and the advantage becomes clear.

There’s also an interesting interaction with premium tax credits (PTCs) available through ACA marketplaces. Employees offered an affordable ICHRA generally cannot claim these credits, but if the ICHRA is deemed unaffordable, they may opt out and still qualify. This creates a nuanced decision-making process where employees can evaluate which option provides the most financial benefit.

From a broader perspective, these tax advantages make ICHRA a highly efficient way to deliver healthcare benefits. It’s not just about saving money—it’s about maximizing the value of every dollar spent.

Think of it like this: instead of pouring money into a system with hidden inefficiencies, ICHRA channels funds directly to where they’re needed, with minimal loss along the way. That kind of efficiency is rare, especially in the complex world of healthcare.

ICHRA vs QSEHRA vs Group Insurance

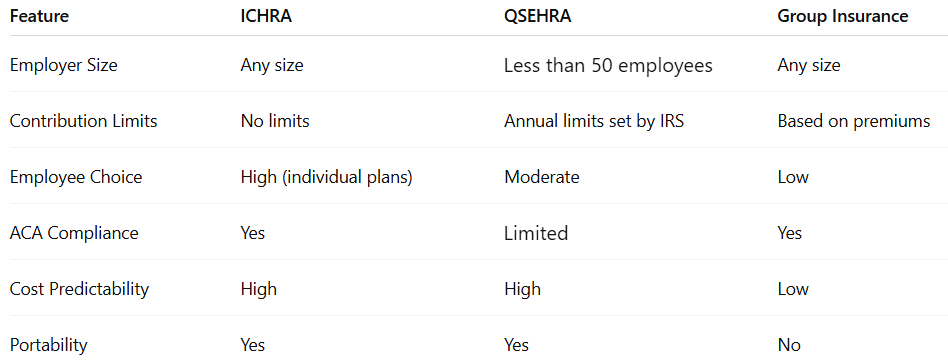

Comparison Table

When comparing ICHRA, QSEHRA, and traditional group insurance, the differences can feel overwhelming at first. But once you break it down, the distinctions become much clearer. Each option serves a different purpose, and understanding those nuances is key to making the right choice.

This table highlights a fundamental truth: ICHRA offers the most flexibility and scalability among the three. While QSEHRA is a great option for small businesses, it comes with contribution caps that can limit its effectiveness. Traditional group insurance, while familiar, often lacks the adaptability modern businesses need.

Which Option is Best for Different Business Sizes

Choosing between these options isn’t about picking the “best” one universally—it’s about finding the best fit for a specific business context. For small businesses with fewer than 50 employees, QSEHRA can be a simple and effective starting point. It’s relatively easy to implement and provides a structured way to reimburse employees for healthcare costs.

However, as businesses grow, the limitations of QSEHRA become more apparent. Contribution caps can restrict how competitive the benefits package is, making it harder to attract and retain talent. That’s where ICHRA steps in as a more scalable solution.

For mid-sized and large companies, ICHRA offers a compelling alternative to traditional group plans. It allows organizations to meet ACA requirements while maintaining control over costs and offering employees greater choice. This is particularly valuable for companies with diverse or geographically dispersed teams.

Traditional group insurance still has its place, especially for organizations that prefer a more hands-off approach for employees. Some workers may appreciate the simplicity of being enrolled in a pre-selected plan without having to make decisions themselves. But for companies looking to modernize their benefits strategy, it often feels like an outdated model.

In many ways, the decision comes down to philosophy. Do you want a centralized system that treats everyone the same, or a flexible one that adapts to individual needs? As workplaces continue to evolve, more businesses are leaning toward the latter—and ICHRA is leading that shift.

Benefits of ICHRA for Employers

Cost Control and Predictability

If there’s one pain point that keeps employers up at night when it comes to healthcare, it’s unpredictability. Traditional group health insurance has a habit of creeping up in cost year after year, often without warning. One renewal cycle looks manageable, the next feels like a budget crisis. This is exactly where ICHRA changes the game in a very practical, almost refreshing way.

With ICHRA, employers flip from a defined-benefit model to a defined-contribution model. That might sound like jargon, but the idea is simple: instead of committing to whatever premiums insurers decide, businesses set a fixed monthly allowance per employee. That’s the ceiling. No surprise increases. No last-minute negotiations. Just clear, controlled spending.

Imagine running a business where you already juggle payroll, operations, marketing, and growth targets. The last thing you need is a volatile expense like healthcare throwing everything off balance. ICHRA acts like a stabilizer. You decide the number, and the system works around it—not the other way around. According to industry insights, companies adopting defined contribution health models have reported more stable year-over-year benefits spending, often reducing unexpected cost spikes significantly.

There’s also a strategic advantage here. Employers can gradually adjust contributions over time based on company performance, hiring goals, or economic conditions. In a strong year, they might increase allowances to stay competitive. In tighter times, they can hold steady without the pressure of external premium hikes. That kind of flexibility is rare in traditional insurance models.

Another angle worth considering is transparency. With ICHRA, the cost of benefits is no longer hidden inside complex insurance contracts. It’s visible, straightforward, and easy to communicate. Employees know exactly what’s being offered, and employers know exactly what they’re spending.

In a way, ICHRA turns healthcare from a reactive expense into a proactive strategy. And for businesses trying to grow sustainably, that shift isn’t just helpful—it’s essential.

Simplified Administration

Let’s be honest—managing a traditional group health plan can feel like navigating a maze blindfolded. There are enrollment periods, compliance rules, insurer negotiations, claims issues, and endless paperwork. For many businesses, especially smaller ones without dedicated HR teams, this administrative burden becomes overwhelming.

ICHRA simplifies much of that complexity by removing the need to manage a group insurance policy altogether. Employers are no longer responsible for selecting plans, negotiating premiums, or dealing with insurance carriers on behalf of employees. Instead, their role becomes more focused: define contributions, ensure compliance, and facilitate reimbursements.

Now, you might be thinking—doesn’t reimbursement add its own layer of complexity? It can, but this is where modern technology steps in. Most companies use ICHRA administration platforms or third-party providers that handle documentation, claims verification, and compliance automatically. Employees upload proof of coverage or expenses, the system verifies eligibility, and reimbursements are processed seamlessly.

This shift significantly reduces the administrative workload. HR teams can redirect their energy toward more impactful initiatives like employee engagement, culture building, and talent development instead of getting bogged down in insurance logistics.

There’s also less back-and-forth communication. In traditional setups, employees often go to HR with questions about coverage, claims, or provider networks—questions HR may not always be equipped to answer. With ICHRA, employees interact directly with insurers or marketplaces when choosing plans, which cuts down on confusion and miscommunication.

Another subtle but important benefit is scalability. As a company grows, managing a group plan becomes increasingly complex. ICHRA scales much more smoothly because the core structure—set contributions and reimbursements—remains consistent regardless of workforce size.

In short, ICHRA doesn’t just save money—it saves time, energy, and mental bandwidth. And in today’s fast-moving business environment, that kind of efficiency can make a meaningful difference.

Benefits of ICHRA for Employees

Choice and Portability

From an employee’s perspective, traditional health insurance can sometimes feel like being handed a pre-packed lunch—you didn’t choose it, and it might not suit your taste, but it’s what you’ve got. ICHRA replaces that experience with something far more empowering: choice.

Instead of being limited to one or two employer-selected plans, employees can explore a wide range of individual health insurance options. They can compare premiums, deductibles, coverage levels, and provider networks to find something that genuinely fits their needs. Whether someone prioritizes low monthly costs or comprehensive coverage, ICHRA gives them the freedom to decide.

This level of control is especially valuable in today’s diverse workforce. Think about it—an early-career professional, a parent with two kids, and someone managing a chronic condition all have very different healthcare needs. Expecting a single group plan to serve all of them equally well is unrealistic. ICHRA acknowledges that reality and adapts accordingly.

Then there’s the concept of portability, which is often overlooked but incredibly important. With traditional employer-sponsored insurance, coverage is tied to the job. Leave the company, and you lose the plan. That disruption can be stressful, especially during career transitions.

With ICHRA, the insurance policy belongs to the individual. If an employee changes jobs, they can often keep their existing plan (as long as they continue paying premiums). That continuity provides peace of mind and eliminates the need to start from scratch every time they switch roles.

There’s also a psychological shift that comes with ownership. When employees choose and manage their own plans, they tend to be more engaged and informed about their healthcare decisions. It’s no longer a passive benefit—it’s an active part of their financial and personal well-being.

In a world where people value autonomy more than ever, this combination of choice and portability makes ICHRA feel less like a perk and more like a modern necessity.

Personalized Coverage Options

Healthcare isn’t one-size-fits-all, and deep down, everyone knows it. Yet for decades, that’s exactly how employer-sponsored insurance has operated. ICHRA breaks away from that mold by enabling truly personalized coverage.

Employees can tailor their insurance plans to match their unique situations. Someone who rarely visits the doctor might choose a high-deductible health plan (HDHP) with lower premiums, pairing it with a Health Savings Account (HSA) for added tax benefits. On the other hand, someone who expects frequent medical visits might opt for a plan with higher premiums but lower out-of-pocket costs.

This personalization extends beyond just cost structures. Employees can select plans that include their preferred doctors, specialists, and hospitals. They can prioritize mental health coverage, maternity benefits, or specific prescription drug coverage depending on their needs. It’s a level of customization that traditional group plans rarely achieve.

Another important aspect is family coverage. Employees with dependents can choose plans that adequately cover their entire household, rather than trying to fit into a plan designed for a generalized workforce. This makes ICHRA particularly appealing for working parents or caregivers.

There’s also an educational component here. As employees explore their options, they naturally become more informed about how health insurance works—deductibles, copays, networks, and all the details that often feel confusing. Over time, this leads to better decision-making and more efficient use of healthcare resources.

In many ways, ICHRA aligns healthcare with how people already approach other areas of life. Just like choosing a phone plan, a streaming subscription, or even a gym membership, individuals can pick what works best for them instead of settling for a default option.

That sense of personalization doesn’t just improve satisfaction—it can lead to better health outcomes, because people are more likely to use coverage that actually fits their needs.

Common Challenges and Considerations

Compliance Requirements

While ICHRA offers flexibility and innovation, it’s not a free-for-all. There are important compliance requirements that employers need to understand and follow carefully. Ignoring these rules isn’t just risky—it can lead to penalties or disqualification of the plan.

One of the biggest considerations is ACA compliance, especially for Applicable Large Employers (ALEs). To meet the employer mandate, the ICHRA offered must be considered affordable and provide minimum value. This involves calculating affordability based on employee income and ensuring the allowance is sufficient to cover a baseline insurance plan.

There are also strict rules around employee classes. Employers can’t arbitrarily offer ICHRA to some employees while excluding others within the same class. The classifications must be legitimate—such as full-time vs. part-time—and meet minimum class size requirements in certain cases.

Documentation is another key area. Employers must provide formal ICHRA notices to employees, explaining how the benefit works, how to opt in or out, and how it interacts with premium tax credits. These notices must be delivered within specific timeframes, typically at least 90 days before the plan year begins.

Privacy and data handling also come into play. Since reimbursements involve medical expenses, employers must ensure compliance with HIPAA regulations, often by using third-party administrators to handle sensitive information.

All of this might sound daunting, but it’s manageable with the right setup. Many businesses rely on specialized ICHRA providers who handle compliance automatically, reducing the risk of errors.

The key takeaway? ICHRA is flexible, but it’s structured flexibility. When implemented correctly, it offers the best of both worlds—freedom and compliance.

Employee Education and Adoption

Even the best system can fall flat if people don’t understand how to use it. That’s one of the biggest challenges with ICHRA: employee education. For workers who are used to traditional group plans, the shift to choosing their own insurance can feel unfamiliar, even intimidating at first.

Think about it—suddenly, employees are asked to compare plans, evaluate coverage options, and make decisions that directly impact their health and finances. Without proper guidance, that responsibility can feel overwhelming.

This is why communication is critical. Employers need to provide clear, accessible explanations of how ICHRA works, what steps employees need to take, and where they can find help. Many companies offer onboarding sessions, guides, or access to benefits advisors who can walk employees through the process.

There’s also a timing factor. Employees need enough time to explore options and enroll in plans before coverage begins. Rushing this process can lead to poor decisions or missed opportunities.

Adoption tends to improve when employees see the value firsthand. Once they realize they can choose plans that better fit their needs—and that reimbursements are tax-free—the system starts to make sense. Over time, what initially felt complex becomes intuitive.

Another helpful approach is leveraging technology. User-friendly platforms that simplify plan comparison and reimbursement tracking can significantly enhance the experience.

At its core, ICHRA isn’t just a policy change—it’s a mindset shift. And like any shift, it takes time, communication, and support to fully take hold. But once it does, the benefits become hard to ignore.

Conclusion

ICHRA represents a fundamental shift in how healthcare benefits are designed, delivered, and experienced. It moves away from rigid, employer-controlled systems toward a model that prioritizes flexibility, transparency, and individual choice. For employers, it offers predictable costs and reduced administrative burden. For employees, it provides autonomy, portability, and personalized coverage options that align with real-life needs.

As the workforce continues to evolve—with remote work, diverse employee profiles, and increasing demand for customization—ICHRA fits naturally into this new landscape. It’s not just an alternative to traditional group insurance; it’s a modern solution built for the realities of today’s workplace.

Businesses that embrace ICHRA aren’t just adapting to change—they’re staying ahead of it. And employees who take advantage of its flexibility often find themselves more engaged and satisfied with their healthcare decisions.

FAQs

1. Who is eligible for ICHRA?

ICHRA can be offered by employers of any size, but employees must have individual health insurance that meets minimum essential coverage requirements to participate.

2. Can employees choose any health insurance plan with ICHRA?

Yes, employees can select plans from the individual marketplace or private insurers, as long as the coverage meets ACA standards.

3. Is ICHRA better than traditional group health insurance?

It depends on the company’s needs. ICHRA offers more flexibility and cost control, while group plans may be simpler for employees who prefer less decision-making.

4. Are ICHRA reimbursements taxable?

No, reimbursements are tax-free for employees and tax-deductible for employers, making it a highly efficient benefit structure.

5. Can ICHRA be used with Health Savings Accounts (HSAs)?

Yes, but it depends on how the ICHRA is structured. Employees need to be enrolled in an HSA-compatible plan to contribute to an HSA.

SOURCEs

https://www.healthcare.gov/small-businesses/learn-more/individual-coverage-hra/

https://www.irs.gov/pub/irs-drop/n-19-45.pdf

https://www.takecommandhealth.com/ichra-guide

https://www.kff.org/health-costs/report/2023-employer-health-benefits-survey/