Truck Driver Health Insurance: A Practical Guide for Drivers, Owner-Operators, and Families

Truck driver health insurance is not just another monthly bill. It is the safety net that keeps one bad diagnosis, one ER visit, or one prescription refill from turning into a financial pileup. When you drive for a living, your body is part of the business. Your eyes, back, heart, legs, sleep, blood pressure, and mental focus are not side issues; they are the engine behind every mile you run and every load you deliver.

The problem is that health insurance can feel confusing, especially for truckers. A company driver may have benefits through a carrier but still wonder whether the deductible is too high or whether the plan works away from home. An owner-operator may be staring at marketplace plans, private quotes, association memberships, and supplemental policies, trying to figure out what is real coverage and what is just shiny marketing. A leased operator might sit somewhere in the middle, technically self-employed but still connected to a fleet that offers limited benefits.

This guide breaks the whole thing down in plain English. You will learn what types of health insurance for truck drivers exist, how to compare plans, what owner-operators should pay special attention to, and how to avoid paying for coverage that does not actually help on the road. The goal is not to turn you into an insurance expert. The goal is to help you ask smarter questions before you sign up, so your coverage works when you need it most.

Why Health Insurance Matters for Truck Drivers

Health insurance matters for truck drivers because trucking is hard on the body in ways that sneak up over time. Sitting for long hours, eating whatever is available near a fuel island, sleeping at odd times, dealing with delivery pressure, and spending days or weeks away from home can wear down even the toughest driver. You might feel fine today, but blood pressure, diabetes, sleep apnea, joint pain, and heart issues often build quietly in the background. Health coverage gives you access to preventive care, checkups, screenings, and early treatment before small issues become career-ending problems.

There is also the practical side: your medical condition can affect your ability to keep driving. Commercial drivers must meet medical standards to maintain a valid DOT medical certificate, and untreated health conditions can threaten that certificate. For example, uncontrolled high blood pressure, unmanaged diabetes, serious sleep problems, or certain heart conditions can make it harder to pass a DOT physical. A good insurance plan helps you stay ahead of those issues instead of scrambling after a failed exam.

Truckers are also exposed to everyday risks that office workers rarely face. Climbing in and out of trailers, securing freight, walking across icy lots, fueling in bad weather, and driving through traffic all increase the chance of injury. Even a simple fall can lead to imaging, therapy, specialist visits, and time off the road. Without insurance, those costs can hit like a blown steer tire at highway speed.

The best way to think about truck driver medical insurance is as business protection and family protection at the same time. For company drivers, it protects income and household stability. For owner-operators, it protects the business because the driver is the business. If the person behind the wheel cannot afford treatment, the truck payment, insurance, fuel card, and family budget can all get squeezed fast.

The Real Health Risks of Life on the Road

Life on the road creates a unique health profile. According to CDC/NIOSH research on long-haul truck drivers, drivers have historically shown higher rates of obesity and smoking than the general working population, with occupational health researchers pointing to long sitting periods, limited food options, irregular sleep, and demanding schedules as major contributors. Those numbers are not meant to shame anyone. They simply show that trucking is not a normal workplace, and the health plan you choose needs to match the reality of the job.

Think about a typical day behind the wheel. You may start before sunrise, drink coffee to stay alert, grab a breakfast sandwich because it is quick, sit through traffic, wait at a dock for hours, then push hard to make up time. By the time you park, the best meal option may be fried, salty, oversized, or all three. Add stress, loneliness, noise, vibration, and inconsistent sleep, and the body starts paying interest on that lifestyle debt.

Common health concerns among truck drivers include high blood pressure, type 2 diabetes, sleep apnea, back pain, neck pain, knee problems, digestive issues, anxiety, depression, and cardiovascular disease. Many of these conditions are manageable when caught early. But early care requires access: primary care visits, lab work, prescriptions, follow-ups, durable medical equipment, and sometimes specialists. That is where health insurance becomes more than paperwork.

A strong health insurance plan for truckers should make it easier to get care even when you are not near home. Drivers need plans with practical networks, telehealth options, pharmacy access, and urgent care coverage that works across regions. The right plan helps you treat your body like a fleet asset, because that is exactly what it is. You would not run a truck for years without oil changes, filters, inspections, and repairs. Your health deserves at least the same level of maintenance.

Why Going Uninsured Can Cost More Than Premiums

Going without health insurance may look cheaper month to month, but it can become brutally expensive after one medical event. A single emergency room visit can create bills for the hospital, the physician, imaging, lab work, medication, and follow-up care. If an injury keeps you off the road, the financial damage does not stop with medical bills. Lost income, late truck payments, missed household bills, and credit card debt can start stacking up before you even feel healthy again.

For owner-operators, the risk is even sharper. When you are self-employed, there may be no paid sick leave, no employer disability cushion, and no benefits department to help you navigate the system. If you are uninsured and need surgery, ongoing medication, or specialist treatment, the business can stall. A truck sitting still does not generate revenue, but fixed costs keep rolling like mile markers on the interstate.

Health insurance also helps with negotiated rates. Insured patients usually benefit from rates negotiated between providers and insurers, while uninsured patients may receive full billed charges unless they negotiate directly or qualify for financial assistance. That difference can be massive. Even when you have a deductible, the plan’s negotiated pricing can reduce the amount you owe compared with walking in as a cash-pay patient.

There is also peace of mind, and that matters more than people admit. Driving already demands attention, patience, and emotional control. Worrying about what would happen if chest pain, a bad infection, or a serious injury shows up on the road adds another layer of stress. Affordable health insurance for truck drivers is not always easy to find, but going uninsured is rarely a clean win. It is more like running without cargo insurance because “nothing happened last week.” Maybe you get away with it for a while, but the gamble gets ugly when luck runs out.

Main Health Insurance Options for Truck Drivers

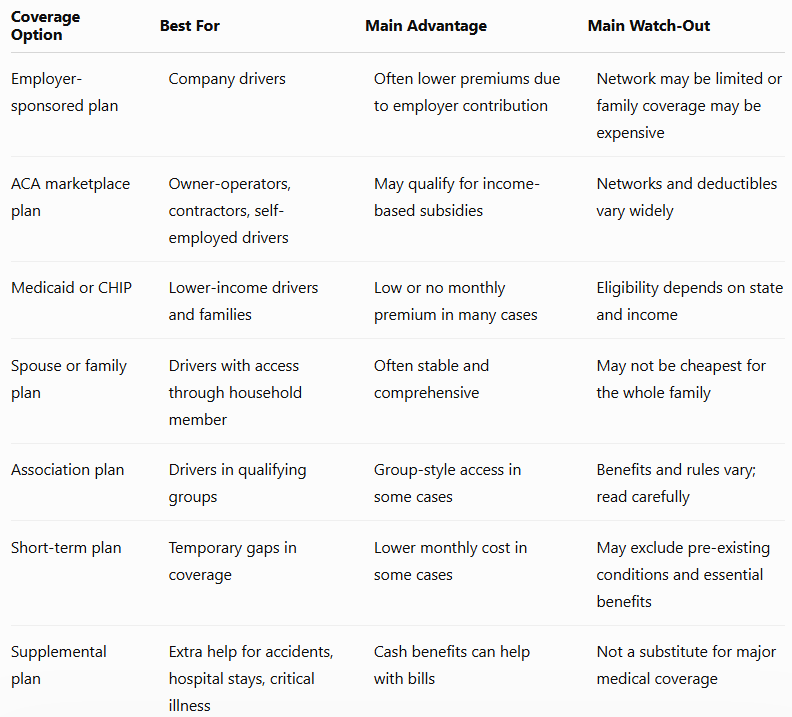

Truck drivers usually have several possible health insurance paths, but the best option depends on employment status, income, state of residence, family situation, and travel patterns. A company driver may get coverage through an employer-sponsored plan. An owner-operator may shop through the ACA marketplace, buy private coverage, use a spouse’s plan, qualify for Medicaid, or combine major medical coverage with supplemental policies. The trick is knowing which option provides real protection and which one leaves dangerous gaps.

Major medical insurance is usually the foundation. This is the kind of insurance that can cover doctor visits, preventive care, hospitalization, emergency services, prescriptions, mental health care, and chronic disease management, depending on the plan. It is different from limited-benefit products that only pay a fixed amount for certain events. Supplemental coverage can be useful, but it should not be confused with full health insurance.

Here is a simple comparison of common truck driver health insurance options:

The main point is simple: do not shop by premium alone. A cheap plan that does not cover your doctors, prescriptions, or out-of-state urgent care may fail the moment you need it. A slightly higher premium can be worth it if the plan has better protection, stronger networks, and predictable costs.

Employer-Sponsored Health Insurance

Employer-sponsored health insurance is often the first place company drivers should look. Many large trucking companies offer medical, dental, vision, and sometimes life or disability benefits. Because the employer may pay part of the premium, this coverage can be more affordable than buying a plan alone. For a driver with a spouse or children, however, the cost can rise quickly once dependents are added.

The biggest advantage of employer coverage is convenience. Enrollment is usually handled through the company, premiums come out of payroll, and the plan documents are presented in a benefits package. Some carriers offer multiple tiers, such as a lower-premium high-deductible plan, a traditional PPO-style plan, or a plan paired with a Health Savings Account. Drivers who rarely see a doctor may be tempted by the lowest premium, but the deductible and out-of-pocket maximum deserve just as much attention.

The biggest question for truckers is whether the network works on the road. A plan may look fine near your home terminal but become frustrating when you need care three states away. Emergency care is generally handled differently than routine care, but urgent care, follow-up appointments, imaging, and prescriptions can still get complicated if you are outside the preferred network. Before enrolling, drivers should ask whether the plan has a national network, how out-of-network claims are handled, and which pharmacy chains are preferred.

Employer-sponsored coverage can be an excellent deal, especially when the company contributes generously. Still, drivers should not enroll blindly. Read the summary of benefits, compare deductibles, check medication coverage, and look at family costs. A good employer plan should help you stay healthy without forcing you to park the truck every time you need routine care.

ACA Marketplace Health Insurance Plans

ACA marketplace plans are one of the most important options for owner-operators, independent contractors, and truck drivers without employer coverage. These plans are sold through federal or state health insurance marketplaces and must generally follow Affordable Care Act rules, including coverage for essential health benefits and protections for pre-existing conditions. Depending on household income and location, some drivers may qualify for premium tax credits that reduce the monthly cost. That can make marketplace coverage far more realistic than private quotes that do not include subsidies.

Marketplace plans are usually grouped into metal tiers: Bronze, Silver, Gold, and Platinum where available. Bronze plans often have lower monthly premiums but higher out-of-pocket costs when you use care. Gold plans usually cost more each month but may reduce the financial shock when you need treatment. Silver plans can be especially important for people who qualify for cost-sharing reductions, though eligibility depends on income and plan selection.

For truckers, the biggest ACA marketplace issue is network design. Some plans are HMOs or EPOs with tighter provider networks, while others may offer broader access. A plan with a narrow local network might work for someone who lives and works in one city, but truck drivers live differently. You may need urgent care near a delivery point, a prescription refill in another state, or telehealth while parked at a rest area.

When comparing ACA plans, do not stop at the premium. Look at the deductible, out-of-pocket maximum, prescription formulary, specialist rules, urgent care coverage, and telehealth access. Also check whether your preferred doctors and pharmacies participate. Health insurance for owner-operator truck drivers needs to be flexible enough for life on the road, not just cheap enough to look good on enrollment day.

Medicaid, CHIP, and State-Based Coverage

Medicaid may be an option for some truck drivers and families, especially during lower-income years, business slowdowns, medical leave, or transitions between jobs. Eligibility depends on state rules, household size, income, and other factors. In states that expanded Medicaid under the Affordable Care Act, more low-income adults may qualify. Children may qualify for CHIP, the Children’s Health Insurance Program, even when adults in the household do not qualify for Medicaid.

This matters because trucking income can be uneven. An owner-operator may gross impressive revenue but still have high expenses for fuel, maintenance, insurance, repairs, permits, factoring, and taxes. A company driver may have strong months followed by slow freight, home time, or health-related downtime. Since eligibility rules can be based on income, drivers should look at actual household numbers rather than assuming they make too much or too little.

Medicaid coverage can be very helpful because premiums and out-of-pocket costs are often low. It can cover doctor visits, hospital care, prescriptions, preventive services, mental health care, and more, depending on the state program. For children, CHIP can provide strong coverage for checkups, immunizations, dental care, vision care, and emergency services. For a trucking family trying to stay afloat, that can be the difference between getting care early and delaying it.

The challenge is that Medicaid is state-based, and truck drivers are mobile. A driver who lives in one state but spends most workdays elsewhere should understand how the plan handles out-of-state care, emergency services, and prescriptions. Medicaid can be excellent coverage for eligible households, but it requires careful attention to state rules. Drivers should confirm details directly with their state Medicaid agency or marketplace before making decisions.

Spouse, Partner, or Family Health Insurance

A spouse, partner, or family health insurance plan can be one of the best options for truck drivers, especially if another household member has access to strong employer benefits. Sometimes the most affordable and comprehensive coverage is not through the trucking job at all. A driver married to a teacher, nurse, government employee, warehouse manager, or corporate worker may find that joining that plan provides better benefits than buying individual coverage.

The key is to compare the full household cost, not just the driver’s premium. Some employer plans are very affordable for employees but expensive when adding spouses or dependents. Others offer generous family coverage that beats marketplace options. You need to look at the premium, deductible, out-of-pocket maximum, copays, prescription costs, and whether your doctors and medications are covered.

Family coverage also matters when the trucker is away from home. A spouse may be the one taking children to appointments, managing prescriptions, or handling medical bills while the driver is on the road. Having everyone on one plan can make billing and records simpler. On the other hand, splitting coverage may sometimes save money, such as when children qualify for CHIP or when the spouse’s plan is good for dependents but costly for the truck driver.

Do not assume one setup is automatically best. Run the numbers like you would calculate fuel cost, deadhead miles, and maintenance reserves. The cheapest monthly premium may not be the cheapest yearly cost if someone in the family needs regular care. A good family health insurance plan for truck drivers should protect the people at home and the person behind the wheel.

Association, Short-Term, and Supplemental Plans

Association plans, short-term medical plans, accident policies, hospital indemnity plans, and critical illness policies are heavily marketed to self-employed people, including truck drivers. Some of these products can be useful, but drivers need to understand what they are buying. Not every plan called “health coverage” works like major medical insurance. Some pay limited benefits, exclude pre-existing conditions, cap payouts, or leave out major categories of care.

Association health plans may be offered through trade groups, professional organizations, or membership programs. In some cases, they can provide access to group-style benefits, but rules and protections vary. Drivers should read the plan documents, not just the sales page. Ask whether the plan is ACA-compliant, whether it covers pre-existing conditions, what the annual limits are, and whether it includes hospitalization, prescriptions, emergency care, mental health care, and preventive services.

Short-term plans may help during temporary gaps, such as waiting for employer benefits to begin. They may have lower premiums, but the tradeoff can be significant. These plans may not cover pre-existing conditions and may not include all essential health benefits. For a driver with diabetes, high blood pressure, sleep apnea, past injuries, or ongoing prescriptions, that can be a serious problem.

Supplemental policies can still play a role. An accident policy may provide cash after an injury. A hospital indemnity plan may pay a fixed amount for a hospital stay. A critical illness policy may help with expenses after a covered diagnosis. These can help cover deductibles, home bills, or time off, but they should sit beside major medical insurance, not replace it. Think of supplemental coverage like extra straps on a load. Helpful? Absolutely. But you still need the trailer, brakes, and tires.

How Owner-Operators Should Choose Health Insurance

Owner-operators need to shop for health insurance with a business owner’s mindset. Your coverage is not just a personal benefit; it is part of your risk management plan. You already budget for fuel, maintenance, tires, cargo insurance, liability coverage, permits, accounting, and taxes. Health insurance belongs in that same category because one serious medical issue can interrupt income faster than a blown turbo.

The first step is to define your real needs. Are you single or covering a family? Do you take regular prescriptions? Do you have a chronic condition like high blood pressure, diabetes, asthma, or sleep apnea? Do you need access to specialists? Do you travel mostly regional routes or run nationwide? These questions matter because the “best” plan for a healthy local driver may be a poor fit for a long-haul owner-operator with regular medications.

Next, compare total annual cost instead of only monthly premium. A plan with a low premium and a high deductible can work for someone who rarely uses care and has emergency savings. But if you expect regular appointments, lab work, prescriptions, or therapy, a richer plan may cost less over the year. The right choice depends on how likely you are to use care and how much financial risk you can comfortably absorb.

Owner-operators should also consider cash flow. Trucking income can swing from month to month, so a predictable premium may feel safer than unpredictable medical bills. A Health Savings Account-compatible high-deductible health plan may be attractive for some self-employed drivers because it can combine tax advantages with savings for future care, but it only works well if you can actually fund the account. Choosing owner-operator health insurance is not about finding a perfect plan. It is about finding the plan that gives you the strongest protection for the kind of trucking life you actually live.

Premiums, Deductibles, and Out-of-Pocket Maximums

Premiums, deductibles, and out-of-pocket maximums are the three numbers truck drivers must understand before choosing a health plan. The premium is the monthly amount you pay to keep coverage active. The deductible is what you may need to pay for covered services before the insurance starts paying more of the bill. The out-of-pocket maximum is the yearly ceiling on covered in-network costs, after which the plan generally pays 100% of covered in-network services for the rest of the plan year.

A cheap premium can be tempting, especially when freight rates are tight or fuel costs are high. But a low-premium plan with a huge deductible can still leave you exposed. Imagine paying less each month but facing several thousand dollars before the plan helps much with non-preventive care. That might be acceptable if you have savings and rarely need treatment, but it can be stressful if you already know you need regular care.

The out-of-pocket maximum deserves special respect. This number tells you the worst-case scenario for covered in-network medical costs in a bad health year. A driver who needs surgery, hospitalization, or expensive treatment may hit that maximum. Comparing this number across plans helps you understand risk in a way the monthly premium alone cannot show.

When shopping, calculate a realistic yearly estimate. Add twelve months of premiums, expected doctor visits, prescriptions, and possible deductible exposure. Then look at the worst-case number if something major happens. Truckers are used to thinking in operating costs, and health insurance should be treated the same way. The lowest monthly cost is not always the best deal, just like the cheapest tire is not always the smartest tire.

Network Coverage Across States

Network coverage is one of the most important health insurance issues for truck drivers because the job does not stay inside one neat ZIP code. A local worker may only care whether a plan covers doctors near home, but a long-haul driver may need care in Nebraska on Monday, Georgia on Wednesday, and Arizona the next week. A plan that looks strong on paper can become frustrating if it only works well in your home county.

The most flexible plans often have broader provider networks, but they may cost more. PPO-style plans can sometimes offer more out-of-network flexibility than HMO-style plans, though details vary widely. Some marketplace plans use narrow networks to keep premiums down, which may be fine for people who rarely travel. For truckers, network limitations can turn a simple urgent care visit into a billing headache.

Emergency care is usually treated differently from routine care, but drivers should not rely on emergency rooms for everything. Urgent care clinics, retail clinics, telehealth appointments, and national pharmacy chains can be much more practical for everyday problems. Before choosing a plan, search for in-network urgent care locations along your common lanes. Also check whether national pharmacy chains are preferred, because prescription access matters when you are hundreds of miles from home.

This is where the cheapest plan can fail. A lower premium does not help much if every minor medical issue becomes out-of-network. For long-haul truck driver health insurance, a wide network can be worth paying more for, especially if you spend weeks away from your home state. Good coverage should travel with you as much as possible, not sit parked at your home address while you are out earning.

Prescriptions, Telehealth, and Urgent Care

Prescriptions, telehealth, and urgent care are the everyday parts of health insurance that truck drivers often use most. A driver with high blood pressure, diabetes, cholesterol medication, asthma inhalers, sleep apnea supplies, or pain management needs cannot afford constant refill problems. When choosing a plan, check the prescription formulary, preferred pharmacies, mail-order options, and refill rules. A medication that is affordable on one plan may be expensive or restricted on another.

Telehealth can be especially useful for truckers. It allows you to speak with a clinician by phone or video for certain non-emergency issues, medication questions, minor infections, follow-ups, mental health care, and routine guidance. It will not replace every in-person visit, but it can prevent small issues from turning into bigger ones while you are on the road. The CDC has long emphasized that regular physical activity and preventive care help reduce disease risk, and telehealth can be one tool that keeps care from being delayed when your schedule is unpredictable.

Urgent care access is another major factor. Truck drivers often cannot wait three weeks for a primary care appointment when they have a sinus infection, sprain, rash, stomach issue, or minor injury. A plan with affordable urgent care copays and a broad clinic network can save time and money. It can also help you avoid unnecessary emergency room bills when the problem is not truly an emergency.

The smartest move is to test the plan before you need it. Look up in-network urgent care centers near your regular routes. Check pharmacy access along your lanes. Review whether virtual visits are included and what they cost. A plan that handles these routine needs smoothly can make life on the road feel less like a medical guessing game.

Health Insurance for Company Drivers

Company drivers often have a simpler path to health insurance, but simple does not always mean obvious. A carrier may offer several plans, each with different premiums, deductibles, networks, and benefits. During enrollment, it is easy to click through quickly because you are busy, tired, or trying to get back on the road. That rushed decision can cost you for an entire plan year.

The first thing company drivers should check is when coverage begins. Some employers start benefits after a waiting period, while others may offer coverage sooner. A driver switching companies should avoid accidental gaps between the old plan and the new one. Even a short gap can be risky if you need medication, have a family member with ongoing care, or experience an injury.

The second issue is whether the company’s plan fits your lifestyle. A driver who is home daily may be fine with a local network. A regional or over-the-road driver needs to think harder about network reach, urgent care access, pharmacies, and telehealth. Some companies offer wellness programs, smoking cessation support, chronic disease management, or health coaching. These extras can be valuable when they are easy to use.

Company drivers should also compare employee-only coverage with family coverage. Sometimes the employee premium is affordable because the employer contributes heavily, but adding a spouse or children may be expensive. In that case, it may make sense to compare the employer plan with marketplace options, a spouse’s plan, Medicaid, or CHIP for children. Company truck driver health insurance can be a strong benefit, but it still needs to be checked against your real family needs and travel schedule.

Questions to Ask Before Enrolling

Before enrolling in any trucking company’s health plan, ask direct questions. Do not worry about sounding picky. Health insurance is part of your compensation, and you deserve to understand it. The recruiter may talk about “great benefits,” but the benefits summary tells the real story. A good plan should hold up under practical questions, not just sales language.

Start with access. Does the plan use a national network? What happens if you need urgent care away from home? Are telehealth visits included? Which pharmacies are preferred? Are your current medications covered, and do they require prior authorization? If you have a spouse, children, or ongoing medical condition, these questions are not optional. They are the difference between smooth coverage and surprise bills.

Then ask about cost. What is the weekly or monthly payroll deduction? What is the deductible? What is the out-of-pocket maximum? Are there separate deductibles for individuals and families? How much are primary care visits, specialist visits, urgent care visits, emergency room visits, and prescriptions? These numbers help you compare the plan to other options instead of guessing.

Also ask about timing and job changes. When does coverage begin? What happens during orientation? Does coverage continue during medical leave, slow periods, or time off? What are the COBRA options if employment ends? These details matter because trucking careers can change quickly. Asking the right questions before enrolling is like doing a pre-trip inspection. You are looking for weak spots before they become roadside emergencies.

Saving Money Without Cutting Protection

Saving money on truck driver health insurance does not mean buying the cheapest plan you can find. It means reducing waste while keeping real protection. The first savings move is to compare all available options: employer coverage, marketplace plans, spouse coverage, Medicaid or CHIP, and legitimate association plans. Many drivers overpay simply because they renew the same plan every year without checking whether their income, family size, route pattern, or medication needs have changed.

Preventive care can also save money over time. Many major medical plans cover certain preventive services without charging a copay when you use in-network providers. Annual checkups, blood pressure checks, cholesterol screenings, diabetes screenings, vaccinations, and counseling can catch problems before they become expensive. That matters in trucking because small health issues can quietly threaten your DOT card, income, and long-term career.

Prescription savings are another big area. Always check whether your medication is generic, preferred, non-preferred, or specialty under the plan’s formulary. Use preferred pharmacies when possible. Ask doctors whether a lower-cost alternative is available. For maintenance medications, mail-order refills may help some drivers, especially those who are away from home for long stretches. Just make sure delivery timing fits your schedule.

You can also save by using the right care setting. Emergency rooms are for emergencies, not routine problems. Telehealth, primary care, urgent care, and retail clinics are often more affordable for non-emergency issues. The goal is not to avoid care; it is to get the right level of care at the right place. Smart use of affordable truck driver health insurance can keep you healthier and keep more money in your pocket.

Tax Considerations for Self-Employed Drivers

Self-employed truck drivers should pay close attention to the tax side of health insurance. In many cases, self-employed individuals may be able to deduct eligible health insurance premiums, subject to IRS rules and limitations. This can include medical, dental, and qualifying long-term care insurance premiums for the driver, spouse, dependents, and certain children under age limits. The details can be complex, so owner-operators should work with a tax professional who understands trucking.

This matters because health insurance should be viewed as part of the business picture, not just the household budget. An owner-operator already tracks fuel, maintenance, tires, repairs, permits, tolls, parking, factoring fees, insurance, and depreciation. Health insurance premiums may also affect taxable income when handled correctly. Keeping clean records is essential because messy bookkeeping can cause missed deductions or problems during tax time.

Health Savings Accounts can also be useful for some self-employed drivers who choose an HSA-qualified high-deductible health plan. An HSA lets eligible individuals set aside money for qualified medical expenses with tax advantages. The account can be used for deductibles, copays, prescriptions, and other qualified costs. Unlike a “use it or lose it” workplace flexible spending account, HSA funds can generally roll over from year to year.

Do not choose a plan only because of tax benefits, though. A high-deductible plan paired with an HSA can be powerful, but only if you can handle the deductible and contribute to the account. If cash flow is tight and regular medical care is needed, a different plan may be better. The smartest approach is to combine insurance planning, tax planning, and business budgeting instead of treating them as separate lanes.

Conclusion

Truck driver health insurance is one of the most important decisions a driver can make, whether you are a company driver, leased operator, independent contractor, or full owner-operator. Trucking is demanding work, and the health risks are real. Long hours, irregular sleep, limited food choices, stress, and physical strain can create medical problems that affect both your life and your livelihood. Good coverage helps you catch problems early, manage ongoing conditions, protect your DOT medical certification, and avoid crushing medical bills.

The best plan depends on your situation. Company drivers should carefully review employer benefits instead of assuming the cheapest payroll deduction is best. Owner-operators should compare marketplace plans, spouse coverage, Medicaid or CHIP eligibility, association options, and supplemental coverage with a clear eye on total yearly cost. Long-haul drivers should pay special attention to national networks, telehealth, urgent care access, and pharmacy availability. Families should compare household costs, not just individual premiums.

The biggest mistake is shopping by premium alone. A low monthly payment can hide a high deductible, narrow network, weak prescription coverage, or poor out-of-state access. A strong plan should match the way you actually live and work. It should help you get care on the road, handle routine prescriptions, protect your family, and reduce financial risk if something serious happens.

Your truck needs maintenance to keep earning. So do you. Health insurance is not just protection against disaster; it is a tool for staying in the driver’s seat longer, healthier, and with less stress hanging over every mile.

FAQs About Truck Driver Health Insurance

1. What is the best health insurance for truck drivers?

The best health insurance for truck drivers depends on whether you are a company driver, owner-operator, leased operator, or part of a family plan. Company drivers should usually start with employer-sponsored coverage because the employer may pay part of the premium. Owner-operators often compare ACA marketplace plans, spouse coverage, Medicaid eligibility, and private options. Long-haul drivers should prioritize broad networks, telehealth, prescription access, and urgent care coverage across multiple states.

2. Can owner-operator truck drivers get health insurance?

Yes, owner-operator truck drivers can get health insurance through ACA marketplace plans, private insurers, spouse or family plans, Medicaid if eligible, association plans, or a combination of major medical and supplemental coverage. Marketplace plans are often a strong starting point because they may offer income-based premium tax credits. Owner-operators should compare total annual cost, not just monthly premiums. They should also check whether the plan works well outside their home state.

3. Is short-term health insurance a good idea for truckers?

Short-term health insurance may help during a temporary gap, but it is usually not the best long-term solution for truck drivers. These plans may exclude pre-existing conditions, limit benefits, or leave out major categories of care. That can be risky for drivers with ongoing prescriptions, sleep apnea, diabetes, high blood pressure, or past injuries. Short-term coverage should be reviewed carefully and not confused with comprehensive major medical insurance.

4. What should truck drivers look for in a health insurance plan?

Truck drivers should look for a plan with affordable total yearly costs, a manageable deductible, a clear out-of-pocket maximum, strong prescription benefits, telehealth, urgent care coverage, and a network that works beyond their home area. Over-the-road drivers should be especially careful with narrow local networks. A plan that is cheap but hard to use on the road may not be a good value. The right plan should fit the driver’s routes, health needs, and family budget.

5. Can self-employed truck drivers deduct health insurance premiums?

Self-employed truck drivers may be able to deduct eligible health insurance premiums, subject to IRS rules and personal tax circumstances. This can be valuable for owner-operators, but the rules can be detailed. Drivers should keep clean records and work with a tax professional who understands trucking businesses. Health insurance should be included in the overall business budget alongside fuel, repairs, permits, insurance, and taxes.

SOURCEs

https://www.cdc.gov/mmwr/preview/mmwrhtml/mm6405a1.htm

https://www.healthcare.gov/self-employed/coverage/

https://www.healthcare.gov/coverage/what-marketplace-plans-cover/

https://www.healthcare.gov/choose-a-plan/plans-categories/

https://www.healthcare.gov/lower-costs/save-on-monthly-premiums/

https://www.medicaid.gov/medicaid/

https://www.medicaid.gov/chip/

https://www.irs.gov/publications/p535