What Is Occupational Accident Insurance for Truckers? A Complete Guide

Understanding Occupational Accident Insurance

Definition and Core Concept

If you’ve spent any time around the trucking industry, you’ve probably heard the term occupational accident insurance tossed around like it’s just another piece of paperwork. But here’s the reality—it’s one of the most important safety nets a trucker can have, especially if you’re working as an independent contractor or owner-operator.

At its core, occupational accident insurance (often called “occ acc” insurance) is a type of policy designed to protect truck drivers financially if they get injured on the job. Think of it as a customized safety cushion built specifically for the trucking lifestyle. Unlike general health insurance, this policy is tailored to cover work-related injuries that happen while you’re on the road, loading cargo, or even handling equipment.

Now, here’s where things get interesting. Many truckers don’t fall under traditional employment structures. Instead of being full-time employees, they’re often classified as independent contractors. That classification changes everything—especially when it comes to insurance. Without employer-provided workers’ compensation, drivers are left to figure out their own protection. That’s exactly where occupational accident insurance steps in.

Picture this: you’re hauling a load across state lines, and something goes wrong—maybe a slip while securing cargo or a highway accident. Medical bills pile up fast, and suddenly you’re not just dealing with an injury—you’re dealing with lost income too. Occupational accident insurance helps bridge that gap by covering medical costs, lost wages, and sometimes even long-term disability.

In simple terms, it’s not just insurance—it’s peace of mind for a job that rarely stays predictable.

How It Differs from Traditional Workers’ Compensation

At first glance, occupational accident insurance and workers’ compensation might seem like twins separated at birth. Both are designed to cover injuries that happen on the job. But dig a little deeper, and you’ll see they operate very differently—and those differences matter a lot for truckers.

Workers’ compensation is typically required by law for companies with employees. It provides broad protection, including medical care, wage replacement, and legal protections. If you’re a company driver, your employer likely already has this in place. You don’t have to think twice about it.

But here’s the catch: independent truckers usually aren’t eligible for workers’ comp. Why? Because they’re not technically “employees.” They’re self-employed, which means the responsibility falls squarely on their shoulders. That’s where occupational accident insurance becomes the go-to alternative.

One major difference lies in flexibility. Workers’ comp is heavily regulated by state laws, meaning coverage and costs are fairly standardized. Occupational accident insurance, on the other hand, is more customizable. Policies can vary depending on the provider, allowing truckers to tailor coverage based on their needs and budget.

Another key distinction is cost. Occupational accident insurance is often more affordable than workers’ compensation. That’s a big deal in an industry where margins can be tight. However, the trade-off is that it may not offer the same level of legal protection or comprehensive coverage.

There’s also the question of control. With occupational accident insurance, truckers have more say in their policy choices—coverage limits, benefit structures, and even add-ons. It’s like building your own safety net instead of being handed a one-size-fits-all solution.

So, while both options aim to protect workers, occupational accident insurance is specifically designed to fill the gap for truckers who operate outside traditional employment systems. And in an industry built on independence, that flexibility can make all the difference.

Why Truckers Need Occupational Accident Insurance

Risks Associated with Truck Driving

Let’s be real for a second—truck driving isn’t just another desk job. It’s a profession that demands long hours, constant focus, and the ability to handle unpredictable situations on the road. Every mile comes with its own set of risks, and those risks aren’t just hypothetical—they’re very real and, unfortunately, quite common.

According to data from the Federal Motor Carrier Safety Administration (FMCSA), thousands of large truck crashes occur every year in the U.S. alone. Even if you’re the safest driver out there, you can’t control everything—weather conditions, reckless drivers, mechanical failures, or even poorly loaded cargo can turn a routine trip into a dangerous situation in seconds.

And it’s not just about highway accidents. Think about the daily tasks truckers perform—loading and unloading cargo, climbing in and out of the cab, handling heavy equipment, and working in unfamiliar environments. These activities can lead to injuries like slips, falls, back strains, and repetitive stress injuries. Over time, even small physical stresses can add up and impact your ability to work.

Now imagine getting injured in the middle of a job. You’re not just dealing with pain—you’re suddenly facing medical bills, downtime, and lost income. For truckers who rely on every haul to make a living, even a short break from work can hit hard financially.

This is where occupational accident insurance becomes more than just a “nice-to-have.” It acts like a financial buffer, helping you stay afloat when things go sideways. It covers not only immediate medical costs but also helps replace lost income while you recover.

Driving a truck is a bit like walking a tightrope—you’re skilled, experienced, and careful, but there’s always an element of risk. Occupational accident insurance is the safety net underneath that rope, ready to catch you when something unexpected happens.

Legal and Financial Considerations

Beyond the physical risks, there’s a whole other layer to think about—legal and financial responsibilities. Trucking isn’t just about moving freight; it’s also about navigating contracts, compliance requirements, and liability issues. And if you’re an independent contractor, those responsibilities fall directly on you.

Many trucking companies require independent drivers to carry occupational accident insurance as part of their contract. Why? Because it protects both parties. If a driver gets injured, the company avoids potential legal complications, and the driver has a clear path to financial support.

Without this type of insurance, things can get messy fast. Imagine trying to cover hospital bills out of pocket after an accident. A single emergency room visit can cost thousands of dollars, and more serious injuries—like fractures or surgeries—can easily climb into the tens of thousands. Add rehabilitation and ongoing treatment, and the numbers become overwhelming.

There’s also the issue of income protection. If you’re unable to drive for weeks or months, how do you pay your bills? Rent, truck payments, fuel costs, and daily expenses don’t just pause because you’re injured. Occupational accident insurance helps fill that gap by providing disability benefits, ensuring you still have a stream of income during recovery.

From a legal standpoint, occupational accident insurance can also help reduce disputes. Unlike workers’ compensation, which often involves legal processes and claims disputes, occ acc policies tend to be more straightforward and faster when it comes to payouts—depending on the provider.

At the end of the day, it’s about protecting your livelihood. Trucking is more than just a job—it’s a business, especially for owner-operators. And like any business, it needs protection against unexpected setbacks. Occupational accident insurance is one of the smartest ways to safeguard both your income and your future in an industry where uncertainty is part of the journey.

Who Needs Occupational Accident Insurance?

Owner-Operators

If there’s one group that benefits the most from occupational accident insurance, it’s owner-operators. Why? Because they’re essentially running their own trucking business. And when you’re your own boss, you don’t have the luxury of employer-provided safety nets.

Owner-operators wear multiple hats—they’re the driver, the manager, the accountant, and the decision-maker all rolled into one. That independence is empowering, but it also comes with responsibility. One of those responsibilities is making sure you’re financially protected if something goes wrong.

Without occupational accident insurance, an injury could mean more than just physical pain—it could mean losing your entire source of income. Unlike company drivers, there’s no employer to step in and cover medical expenses or provide wage replacement. Everything comes out of your own pocket unless you have the right coverage in place.

Think about your truck for a moment. You wouldn’t drive without insurance for your vehicle, right? So why take that risk with your own health and ability to earn? Your body is your most valuable asset in this business, and protecting it should be a top priority.

Another factor to consider is contract requirements. Many freight carriers and logistics companies require owner-operators to carry occupational accident insurance before they can haul loads. It’s not just about protection—it’s about staying eligible for work.

There’s also the flexibility aspect. As an owner-operator, you can choose a policy that fits your specific needs. Whether you want higher disability benefits, additional coverage options, or lower premiums, occupational accident insurance allows you to customize your protection.

In a way, it’s like building your own safety system. You decide how strong you want that system to be. And in an industry where unexpected events can happen at any moment, having that control can make a huge difference.

Independent Contractors vs Company Drivers

The trucking world isn’t one-size-fits-all, and neither are insurance needs. The difference between independent contractors and company drivers plays a huge role in determining whether occupational accident insurance is necessary—or even essential.

Let’s start with company drivers. If you’re employed by a trucking company, there’s a good chance you’re covered under workers’ compensation insurance. That means if you get injured on the job, your employer’s policy typically takes care of medical expenses and lost wages. In this case, occupational accident insurance may not be necessary, though some drivers still opt for additional coverage for extra peace of mind.

Now, flip the script to independent contractors. This is where things change dramatically. Independent drivers are not considered employees, which means they’re usually not eligible for workers’ compensation benefits. That leaves a significant gap in protection—one that occupational accident insurance is designed to fill.

It’s a bit like the difference between renting and owning a home. When you rent, the landlord handles major issues. When you own, everything is on you. Independent contractors are in that “ownership” position when it comes to their work and insurance.

Another key difference is cost responsibility. Company drivers don’t typically pay directly for workers’ comp—it’s covered by the employer. Independent contractors, on the other hand, must pay for their own occupational accident insurance. While that might seem like a downside, the upside is flexibility and often lower premiums compared to traditional workers’ comp.

There’s also a strategic element. Some contractors choose occupational accident insurance because it allows them to maintain their independent status while still having a level of protection. It’s a way to balance freedom with security.

So, who really needs occupational accident insurance? If you’re a company driver, it’s optional. But if you’re an independent contractor or owner-operator, it’s not just important—it’s practically essential for protecting your income, your health, and your future on the road.

What Does Occupational Accident Insurance Cover?

Medical Expenses Coverage

When people think about insurance, the first thing that usually comes to mind is medical bills—and for good reason. In the trucking world, even a minor injury can quickly spiral into a stack of expenses that feels impossible to manage. That’s why medical expense coverage sits at the heart of occupational accident insurance.

Imagine you’re on a delivery run, and while securing cargo, you slip and injure your back. At first, it seems manageable, but then the pain worsens. You end up needing a doctor’s visit, diagnostic scans like MRIs, physical therapy sessions, and possibly even surgery. Without insurance, these costs can pile up fast—often reaching tens of thousands of dollars depending on the severity of the injury.

Occupational accident insurance is designed to step in during exactly these moments. It typically covers a wide range of medical-related expenses, including hospital stays, doctor visits, prescription medications, rehabilitation, and sometimes even chiropractic care. The goal is simple: to ensure that you’re not forced to choose between getting proper treatment and protecting your finances.

What makes this coverage particularly valuable for truckers is its job-specific focus. Unlike standard health insurance, which may have limitations around work-related injuries, occupational accident policies are built specifically for incidents that happen while you’re performing your duties. Whether you’re driving, loading freight, or handling equipment, you’re covered within the scope of your work.

Another important aspect is the speed of access to care. Many policies are structured to provide relatively quick claim processing, helping you get the treatment you need without long delays. In a profession where time off the road directly impacts your income, that speed can make a huge difference.

At the end of the day, medical expense coverage isn’t just about paying bills—it’s about getting you back on your feet and back on the road as quickly and safely as possible. And in trucking, where your ability to work is tied directly to your physical condition, that kind of support is invaluable.

Disability Benefits

Now let’s talk about something that doesn’t get enough attention but should—what happens when you can’t work. Because in trucking, if you’re not driving, you’re not earning. It’s that simple.

This is where disability benefits within occupational accident insurance come into play. These benefits are designed to replace a portion of your income if you’re temporarily or permanently unable to work due to a job-related injury. Think of it as a financial lifeline during one of the most vulnerable times in your career.

There are typically two main types of disability coverage: temporary total disability (TTD) and permanent total disability (PTD). Temporary benefits kick in when you’re expected to recover but need time off, while permanent benefits apply in more severe cases where returning to work isn’t possible.

Let’s put this into perspective. Suppose you’re involved in a highway accident that leaves you with a serious leg injury. Your doctor advises you to stay off the road for three months. During that time, your bills don’t stop—truck payments, insurance premiums, rent, groceries—they all keep coming. Without disability benefits, you’d be dipping into savings or, worse, going into debt.

Occupational accident insurance helps ease that burden by providing weekly or monthly payments based on a percentage of your income. While it may not replace your full earnings, it can cover essential expenses and keep you financially stable during recovery.

Some policies even offer customizable benefit periods and payout limits, allowing you to tailor coverage based on your financial needs. This flexibility is especially useful for owner-operators who may have higher expenses compared to company drivers.

In a way, disability benefits act like a backup engine for your finances. When your primary source of income stalls, this system kicks in to keep things moving. And in an industry where downtime can be costly, having that backup can mean the difference between recovery and financial strain.

Accidental Death and Dismemberment (AD&D)

No one likes to think about worst-case scenarios, but in a high-risk profession like trucking, it’s something you can’t completely ignore. That’s where Accidental Death and Dismemberment (AD&D) coverage becomes an important part of occupational accident insurance.

This component provides financial compensation in the event of a fatal accident or severe injury resulting in loss of limbs, vision, or other life-altering conditions. It’s not just about the driver—it’s about protecting the people who depend on them.

Imagine a scenario where a tragic accident occurs on the road. Without AD&D coverage, the financial impact on a driver’s family can be devastating. Funeral costs, outstanding debts, and the sudden loss of income can create an overwhelming situation. AD&D benefits are designed to provide a lump-sum payment to help families navigate these challenges.

But it’s not only about death benefits. Dismemberment coverage also plays a crucial role. If a driver suffers a severe injury—like losing a hand or eyesight—it can permanently affect their ability to work. In such cases, AD&D provides compensation that can help cover long-term expenses, lifestyle adjustments, and even career transitions.

What makes this coverage particularly meaningful is its role in long-term financial planning. It ensures that even in the most difficult circumstances, there’s a safety net in place for you or your loved ones.

Think of AD&D as a form of legacy protection. It’s not something you hope to ever use, but having it in place provides a sense of security that goes beyond day-to-day operations. In an unpredictable industry like trucking, that peace of mind is something you simply can’t put a price on.

What Is Not Covered?

Common Exclusions

While occupational accident insurance offers a solid layer of protection, it’s not a catch-all solution. Like any insurance policy, it comes with limitations and exclusions—and understanding these is just as important as knowing what’s covered.

One of the most common exclusions involves injuries that occur outside of work-related activities. If you’re off duty and get injured at home or during personal time, your occupational accident policy typically won’t apply. This is because the coverage is specifically designed for job-related incidents.

Another key exclusion is intentional self-inflicted injuries or incidents involving illegal activities. For example, if an accident occurs while driving under the influence of drugs or alcohol, the claim may be denied. Insurance providers expect policyholders to follow safety regulations and laws, and violations can void coverage.

Pre-existing conditions can also be a gray area. Some policies may limit or exclude coverage for injuries related to conditions you had before obtaining the insurance. It’s crucial to read the fine print and understand how your policy handles these situations.

There are also limits on coverage amounts. Even though medical expenses and disability benefits are included, they often come with caps or maximum payouts. If your expenses exceed those limits, you’ll be responsible for the remaining costs.

Another important point is that occupational accident insurance typically does not provide the same legal protections as workers’ compensation. For instance, workers’ comp often prevents employers from being sued, while occupational accident policies don’t always offer that same level of liability protection.

Understanding these exclusions is like knowing the boundaries of a map. It helps you navigate your coverage more effectively and avoid surprises when you need it most. The key takeaway? Don’t just assume you’re fully covered—take the time to understand exactly where your protection begins and ends.

How Occupational Accident Insurance Works

Claims Process Explained

Understanding how occupational accident insurance actually works in real life is where things start to click. It’s one thing to know what’s covered, but it’s another to see how the process unfolds when you actually need to use it. And let’s be honest—when an accident happens, the last thing you want is confusion or delays.

The process usually begins the moment an injury occurs. First, you seek medical attention—this part is non-negotiable. Your health comes first, always. Once you’re stable, the next step is to report the incident to your insurance provider or, in some cases, your motor carrier if they’re involved in your policy setup. Timing matters here. Many policies require injuries to be reported within a specific window, sometimes as short as 24 to 72 hours.

After reporting, you’ll typically need to file a formal claim. This involves submitting documentation such as medical records, incident reports, and sometimes statements from witnesses or your employer/contractor. Think of it as building a clear story of what happened and why the claim is valid.

Once everything is submitted, the insurance company reviews your case. This is where they verify details—was the injury work-related? Does it fall within the policy coverage? Are there any exclusions that apply? If everything checks out, the claim moves forward, and benefits begin to roll out. These could include direct payments for medical expenses or scheduled disability payments.

One thing that stands out about occupational accident insurance is that the process is often faster and less bureaucratic than traditional workers’ compensation claims. There’s usually less legal back-and-forth, which means you can focus more on recovery and less on paperwork battles.

However, it’s still important to stay organized. Keep copies of every document, track your medical visits, and maintain communication with your insurer. Think of it like maintaining your truck—regular attention and proper documentation keep everything running smoothly.

In essence, the claims process is your bridge between an unexpected accident and financial stability. The smoother that bridge is, the easier it becomes to move from recovery back to work.

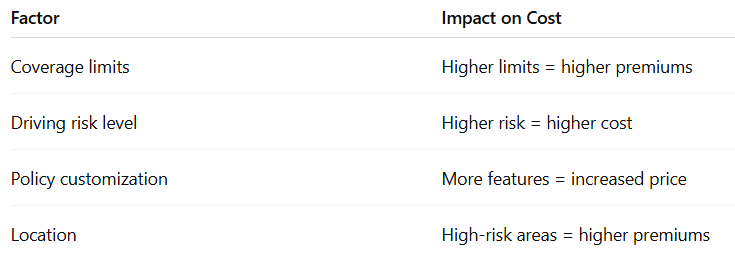

Premium Costs and Factors Affecting Pricing

Let’s talk money—because no matter how good a policy sounds, it has to fit your budget. The cost of occupational accident insurance can vary quite a bit, and understanding what drives those costs can help you make smarter decisions.

On average, occupational accident insurance is significantly cheaper than workers’ compensation, which is one of the main reasons many independent truckers choose it. Depending on the provider and coverage level, premiums can range from around $100 to $300 per month per driver. But why such a wide range? It all comes down to a few key factors.

First, there’s coverage limits. The higher your benefits—whether for medical expenses, disability, or AD&D—the higher your premium will be. It’s similar to choosing between basic and premium fuel; better performance comes at a higher cost.

Next is your driving profile and risk exposure. Factors like your driving history, the type of cargo you haul, and how often you’re on the road can influence pricing. For example, hauling hazardous materials or driving long-haul routes may increase your risk level, which can lead to higher premiums.

Another important factor is policy customization. Many occupational accident policies allow you to tailor coverage, such as choosing waiting periods for disability benefits or setting maximum payout limits. While customization is a big advantage, it also means the final cost depends on the choices you make.

Location can also play a role. Insurance providers often consider regional risk factors, including accident rates and healthcare costs in your operating areas. Even though you’re constantly moving as a trucker, your primary base of operations can influence your premium.

Here’s a simple breakdown to give you a clearer picture:

At the end of the day, the goal is to find a balance. You don’t want to underinsure and risk financial trouble, but you also don’t want to overpay for coverage you may not need. Think of it like tuning your engine—you want optimal performance without unnecessary strain on your resources.

Pros and Cons of Occupational Accident Insurance

Advantages

Occupational accident insurance has gained serious traction in the trucking industry, and it’s not hard to see why. For many drivers, especially independent contractors, it offers a practical and flexible solution to a complex problem.

One of the biggest advantages is affordability. Compared to workers’ compensation, occupational accident insurance is often much more budget-friendly. This makes it accessible for owner-operators who are already managing fuel costs, maintenance, and other business expenses.

Another major benefit is flexibility. Unlike workers’ comp, which is heavily regulated, occupational accident policies can be customized to fit your needs. Want higher disability benefits? Lower premiums? Specific coverage limits? You have options. It’s like building a plan that works specifically for your lifestyle and risk level.

There’s also the speed factor. Claims under occupational accident insurance are often processed faster and with less legal complexity. That means quicker access to funds when you need them most—whether it’s for medical bills or replacing lost income.

Additionally, it supports independent work structures. Trucking thrives on independence, and this type of insurance aligns perfectly with that model. It allows drivers to maintain their contractor status while still having a safety net in place.

Finally, many policies include 24/7 coverage, meaning you’re protected even when you’re off duty in some cases. This added layer of protection can be a game-changer, especially for drivers who spend most of their time on the road.

Disadvantages

Of course, no insurance policy is perfect, and occupational accident insurance is no exception. While it offers many benefits, there are some drawbacks that every trucker should carefully consider.

One of the main disadvantages is limited coverage compared to workers’ compensation. While it covers many essential areas, it may not provide the same level of comprehensive protection, especially when it comes to long-term care or legal benefits.

Another concern is the lack of legal protection. Workers’ compensation typically includes employer liability protection, which can prevent lawsuits. Occupational accident insurance doesn’t always offer this, which could leave room for disputes in certain situations.

There are also coverage caps to think about. Most policies have maximum limits on medical expenses and disability benefits. If your injury leads to costs that exceed those limits, you’ll be responsible for the difference.

Exclusions can also be a sticking point. As mentioned earlier, not all scenarios are covered, and failing to understand these exclusions can lead to unpleasant surprises when filing a claim.

Lastly, because these policies are less regulated, quality can vary between providers. Not all insurance companies offer the same level of service or reliability, so choosing the right provider becomes crucial.

In short, occupational accident insurance is a powerful tool—but only when you understand both its strengths and its limitations.

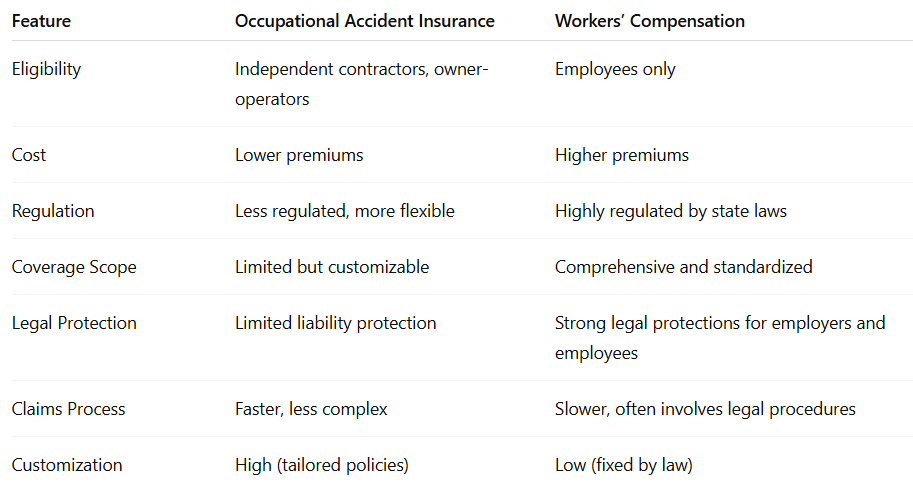

Occupational Accident Insurance vs Workers’ Compensation

Key Differences Table

When it comes to protecting yourself as a trucker, the debate between occupational accident insurance and workers’ compensation often feels like choosing between two very different roads. Both lead to protection, but the journey—and the experience along the way—can be completely different.

To really understand which option fits your situation, it helps to break things down side by side. Think of this comparison like looking under the hood of two trucks. From the outside, they may seem similar, but the internal mechanics tell a very different story.

Here’s a clear comparison to help you visualize the differences:

Now, let’s unpack what this really means in everyday terms.

If you’re a company driver, workers’ compensation is like a factory-installed safety system—it comes with the job, and you don’t have to think much about it. It’s comprehensive, reliable, and backed by legal frameworks that ensure you’re protected in most scenarios.

On the other hand, occupational accident insurance is more like a custom aftermarket upgrade. It gives you control, flexibility, and affordability, but it requires you to make informed decisions about what you need. It’s ideal for independent drivers who don’t have access to workers’ comp but still want a solid layer of protection.

One key difference that often surprises people is the legal aspect. Workers’ compensation typically prevents employees from suing their employers for workplace injuries, creating a structured system for handling claims. Occupational accident insurance doesn’t always include this safeguard, which can lead to different legal dynamics.

Another big factor is speed and simplicity. Occupational accident claims are often processed faster, which can be a huge advantage when you’re dealing with immediate expenses and lost income. Workers’ comp, while thorough, can sometimes feel like navigating a maze of paperwork and regulations.

So which is better? It really depends on your role in the industry. If you’re an independent contractor, occupational accident insurance isn’t just an option—it’s often the most practical solution available. If you’re an employee, workers’ compensation provides a level of protection that’s hard to beat.

Understanding these differences isn’t just about choosing a policy—it’s about choosing how you protect your livelihood in an industry where every decision counts.

How to Choose the Right Policy

Key Features to Look For

Choosing the right occupational accident insurance policy can feel a bit like shopping for a truck—there are plenty of options, and every detail matters more than you think. The goal isn’t just to get insured; it’s to get the right kind of protection that actually works when you need it.

One of the first things to look at is coverage limits. This includes maximum payouts for medical expenses, disability benefits, and accidental death coverage. A policy with low limits might save you money upfront, but it could leave you exposed in a serious situation. Always think long-term—what would you need if the worst happened?

Next, pay attention to disability benefit structure. How much will you receive if you’re unable to work? How long do payments last? Is there a waiting period before benefits kick in? These details can make a huge difference when you’re relying on that income to stay afloat.

Another important feature is 24-hour coverage. Some policies only cover work-related incidents, while others extend protection beyond the job. For truckers who spend most of their time on the road, having broader coverage can add an extra layer of security.

You’ll also want to evaluate the claims process and provider reputation. A policy is only as good as the company backing it. Look for insurers with a track record of fast claims processing and strong customer support. Reviews and industry recommendations can give you valuable insight here.

Customization options are another big plus. The ability to tailor your policy means you can align coverage with your specific needs, whether that’s higher medical limits or additional riders for specialized risks.

In simple terms, choosing a policy is about asking the right questions. Not just “How much does it cost?” but “What does it actually do for me when things go wrong?”

Tips for Truckers Before Buying

Before you sign on the dotted line, it’s worth taking a step back and approaching the decision strategically. Buying occupational accident insurance isn’t just another expense—it’s an investment in your stability and peace of mind.

Start by assessing your personal risk level. What kind of routes do you drive? How often are you on the road? Do you handle heavy or hazardous cargo? The more risk you face, the more comprehensive your coverage should be.

Next, take a close look at your financial situation. How long could you survive without income if you were injured? Do you have savings to fall back on? These questions help determine how much disability coverage you’ll need.

It’s also smart to compare multiple providers. Don’t settle for the first quote you receive. Different insurers offer different benefits, pricing structures, and levels of service. Comparing options can help you find the best value without sacrificing coverage.

Make sure you read the fine print—yes, even the boring parts. Understanding exclusions, waiting periods, and payout limits can prevent unpleasant surprises later. If something isn’t clear, ask questions until it is.

Another tip is to work with a knowledgeable insurance agent who understands the trucking industry. They can help you navigate options and recommend policies that align with your specific needs.

Finally, think of insurance as part of your overall business strategy. Just like maintaining your truck or planning your routes, protecting yourself financially is essential for long-term success.

Conclusion

Occupational accident insurance isn’t just another checkbox in the trucking world—it’s a critical layer of protection that can make or break your financial stability when the unexpected happens. In an industry defined by independence, long hours, and constant risk, having a safety net tailored to your unique needs is not just smart—it’s necessary.

For independent contractors and owner-operators, this type of insurance fills a gap that traditional systems like workers’ compensation simply don’t cover. It provides support where it matters most: medical expenses, lost income, and long-term security. While it may not offer the same level of comprehensive protection as workers’ comp, its flexibility, affordability, and accessibility make it a powerful alternative.

At the same time, it’s important to approach it with a clear understanding. Knowing what’s covered, what’s not, and how the policy works ensures that you’re not caught off guard when you need it most. The right policy doesn’t just protect your wallet—it protects your ability to keep moving forward in a demanding profession.

In trucking, every mile counts. And with occupational accident insurance in place, you’re not just driving—you’re driving with confidence, knowing that no matter what the road throws your way, you’ve got a plan to handle it.

FAQs

1. Is occupational accident insurance required for truckers?

It’s not always legally required, but many trucking companies and contracts mandate it for independent drivers. Even when it’s optional, it’s highly recommended due to the risks involved.

2. How much does occupational accident insurance cost?

Costs typically range from $100 to $300 per month, depending on coverage limits, risk factors, and customization options.

3. Can company drivers get occupational accident insurance?

Yes, but it’s usually unnecessary since most company drivers are covered by workers’ compensation through their employer.

4. Does occupational accident insurance cover off-duty injuries?

It depends on the policy. Some offer 24/7 coverage, while others only cover work-related incidents.

5. What happens if my expenses exceed policy limits?

You’ll be responsible for any costs beyond the coverage limits, which is why choosing adequate coverage is crucial.

SOURCEs

https://www.nhtsa.gov/road-safety

https://www.progressivecommercial.com/

https://www.ooidainsurance.com/