Workers' Compensation Benefits: A Complete Guide for Employees and Employers

What Are Workers' Compensation Benefits?

Definition and Purpose of Workers' Compensation

Workers' compensation benefits are designed to act as a financial safety net when things go sideways at work—because, let’s be honest, accidents don’t send a calendar invite before they happen. Whether it’s a construction worker injuring their back or an office employee developing repetitive strain from long hours at a keyboard, these benefits step in to cover the fallout. At its core, workers' compensation is an insurance program mandated by law that ensures employees receive medical care, wage replacement, and support if they’re injured or become ill due to their job.

Think of it like a built-in protection system for both employees and employers. For workers, it removes the stress of paying out-of-pocket for injuries that weren’t their fault. For employers, it limits exposure to costly lawsuits while still fulfilling their duty of care. According to the U.S. Bureau of Labor Statistics, millions of workplace injuries are reported annually, and workers' compensation plays a central role in handling these incidents efficiently.

The purpose goes beyond just money—it’s about recovery and stability. Employees can focus on healing instead of worrying about rent or medical bills stacking up. Employers, on the other hand, maintain workplace morale and compliance with legal standards. It creates a balance where both sides are protected without turning every injury into a legal battlefield.

The No-Fault Insurance Concept Explained

Here’s where things get interesting: workers' compensation operates under a no-fault system. That means it doesn’t matter who caused the accident—benefits are generally provided regardless. You don’t have to prove your boss was negligent, and your employer doesn’t need to prove you were careless. It’s a bit like a handshake agreement baked into law: “We’ll take care of you, and in return, you won’t sue us.”

This concept dramatically speeds up the process. Imagine having to investigate every workplace accident like a courtroom drama—it would slow everything down and leave injured workers hanging. Instead, the no-fault model ensures quick access to benefits, which can be crucial when medical bills and lost wages start piling up.

Of course, there are exceptions. If an injury results from intentional misconduct—like being under the influence of drugs or alcohol—claims can be denied. But in most standard workplace incidents, the system works without assigning blame. It’s efficient, predictable, and ultimately designed to reduce friction during already stressful situations.

From a broader perspective, the no-fault system also stabilizes industries. Businesses can plan financially because they’re insured, and employees have peace of mind knowing they’re covered. It’s not perfect, but it’s one of the most practical solutions societies have developed to handle workplace injuries without constant legal disputes.

History and Evolution of Workers' Compensation Laws

Early Workplace Injury Laws

If you rewind the clock a couple of centuries, workplace injuries were a completely different story—and not in a good way. Back then, if you got hurt on the job, you were pretty much on your own. The legal system heavily favored employers, and workers had to prove negligence under strict doctrines like the “fellow servant rule” or “assumption of risk.” In plain terms, it was incredibly difficult—almost impossible—for injured employees to receive compensation.

Picture a factory worker in the 1800s losing a hand in unsafe machinery. Instead of receiving medical support or financial aid, they often faced unemployment and poverty. Employers weren’t legally obligated to provide safe conditions, and even if they were negligent, proving it in court required time, money, and resources most workers simply didn’t have.

This imbalance sparked growing dissatisfaction during the Industrial Revolution. As workplaces became more dangerous due to mechanization, injuries surged, and public pressure mounted. Governments began to recognize that leaving injured workers without support wasn’t just unethical—it was economically unsustainable.

The first real shift came in Europe in the late 19th century, particularly in Germany under Otto von Bismarck. These early laws laid the groundwork for modern workers' compensation systems by introducing employer-funded insurance schemes. The idea was simple but revolutionary: workers shouldn’t have to fight in court to receive basic support after being injured on the job.

Modern Legal Framework Across Countries

Fast forward to today, and workers' compensation systems exist in most developed countries, though the specifics vary widely. In the United States, for example, workers' compensation laws are primarily governed at the state level. This means benefits, coverage, and procedures can differ significantly depending on where you live. California’s system looks quite different from Texas, and that can influence everything from payout amounts to claim timelines.

In contrast, countries like Canada and Australia operate more centralized systems, often managed at the provincial or national level. These systems tend to emphasize rehabilitation and return-to-work programs, reflecting a broader approach to employee well-being. Meanwhile, European nations often integrate workers' compensation into their social insurance frameworks, offering comprehensive healthcare and income support.

Despite these differences, the core principles remain consistent: provide timely medical care, compensate lost wages, and reduce litigation. Over time, laws have also evolved to include mental health conditions, occupational diseases, and long-term disabilities—areas that were largely ignored in earlier frameworks.

Technology is now shaping the next phase of evolution. Digital claim filing, telemedicine, and AI-driven case management are making the process faster and more transparent. But challenges still exist, especially around fraud prevention and ensuring fair compensation.

The system has come a long way from its rough beginnings, transforming from a rigid, employer-favoring structure into a more balanced and humane framework. And while it’s not flawless, it continues to adapt as workplaces—and the risks associated with them—change over time.

Types of Workers' Compensation Benefits

Medical Benefits

When it comes to workers' compensation, medical benefits are the backbone of the entire system. After all, what’s the point of financial support if you can’t actually get treated? These benefits are designed to cover everything directly related to your workplace injury or illness, ensuring you receive proper care without worrying about the cost.

This includes doctor visits, hospital stays, surgeries, prescription medications, physical therapy, and even specialized treatments like chiropractic care or mental health counseling when applicable. In many cases, employers or insurance providers will require you to see an approved healthcare provider, which can sometimes feel limiting—but it helps streamline costs and maintain consistency in treatment.

One thing many people don’t realize is that medical benefits often extend beyond immediate care. Long-term rehabilitation, assistive devices like wheelchairs, and home modifications may also be covered if they’re deemed necessary for recovery. Imagine sustaining a serious injury that affects mobility—workers' compensation can step in to ensure your living environment adapts to your needs.

According to the National Safety Council, the average cost of a medically consulted workplace injury in the U.S. exceeds $40,000. Without workers' compensation, that kind of expense could be financially devastating. These benefits essentially remove that burden, allowing injured workers to focus entirely on getting better.

However, disputes can arise. Insurance companies may question the necessity of certain treatments, leading to delays or denials. That’s why understanding your rights—and sometimes seeking legal advice—can make a big difference in ensuring you receive appropriate care.

Medical benefits aren’t just about covering bills—they’re about restoring health, independence, and quality of life. And in many cases, they’re the first and most critical step toward getting back on your feet after a workplace injury.

Wage Replacement Benefits

If medical benefits handle the physical recovery, wage replacement benefits are what keep your financial life from falling apart while you’re unable to work. Because let’s face it—injuries don’t pause your rent, bills, or groceries. These benefits are designed to partially replace the income you lose when a workplace injury prevents you from doing your job, either temporarily or long-term.

Typically, wage replacement benefits cover about two-thirds of your average weekly wage, although the exact percentage varies by state or country. It’s not your full paycheck, and that can feel like a pinch, but it’s structured that way to balance support while still encouraging a return to work when possible. Some jurisdictions also set maximum and minimum payout limits, which means high earners might receive less proportionally, while low-income workers are protected from falling too far below a livable threshold.

There are different categories within wage replacement, and they depend on your ability to work. If you can’t work at all during recovery, you’ll receive temporary total disability payments. If you can return to work in a limited capacity—say, light-duty tasks—you might receive partial benefits to make up the difference between your old and new wages.

Timing also matters. In many cases, there’s a waiting period before benefits kick in, often around 3 to 7 days. However, if your disability extends beyond a certain timeframe, those initial days may be reimbursed retroactively. It’s a small detail, but one that can make a meaningful difference during longer recovery periods.

The real value of wage replacement benefits isn’t just financial—it’s psychological. Knowing that you still have income flowing in, even if reduced, can relieve a huge amount of stress. It allows you to focus on healing instead of scrambling for short-term survival. Without it, even minor injuries could spiral into major financial crises.

Disability Benefits

Disability benefits take wage replacement a step further by addressing how long and how severely your ability to work is affected. Not all injuries are created equal—some heal in weeks, while others permanently alter your capacity to earn a living. That’s where disability classifications come into play.

These benefits are structured around two key questions: Can you work at all? and Will you ever return to your previous level of work? Based on the answers, your case is categorized into different types of disability, each with its own compensation model.

For example, someone who suffers a minor fracture may be temporarily unable to work but will fully recover. On the other hand, someone with a spinal injury might face lifelong limitations. Disability benefits are designed to adapt to these vastly different scenarios, offering tailored support that reflects the severity and permanence of the injury.

The calculation of these benefits often involves medical evaluations, work history, and sometimes even vocational assessments. Insurance companies and legal systems may assign a “disability rating,” which quantifies how much your earning capacity has been reduced. This rating plays a significant role in determining how much compensation you’ll receive and for how long.

It’s worth noting that disputes are common in this area. Employers or insurers may argue that a worker is capable of returning to some form of employment, while the worker and their doctor may disagree. These disagreements can lead to independent medical examinations or even legal hearings.

Disability benefits are about more than just money—they represent acknowledgment of long-term impact. They recognize that some injuries don’t just interrupt your career; they reshape it entirely. And in those cases, having a structured system to provide ongoing support can make all the difference.

Temporary vs Permanent Disability

Understanding the difference between temporary and permanent disability is crucial because it directly affects how long you receive benefits—and how those benefits are calculated. It’s not just a technical distinction; it shapes your entire recovery journey and financial outlook.

Temporary disability, as the name suggests, applies when your condition is expected to improve. You might be unable to work for weeks or months, but there’s a clear path toward recovery. During this time, you’ll receive temporary disability payments, which continue until you either return to work or reach what’s called maximum medical improvement (MMI)—the point where your condition stabilizes and is unlikely to improve further.

Permanent disability, on the other hand, comes into play when your injury leads to lasting impairment. This doesn’t always mean you can’t work at all—it could mean you can’t perform the same job or earn the same income as before. Permanent disability is often divided into two categories: partial and total.

Permanent partial disability (PPD): You can still work, but with limitations.

Permanent total disability (PTD): You’re unable to engage in any gainful employment.

The compensation for permanent disability is usually more complex. It may involve lump-sum payments or ongoing benefits, depending on the severity of the impairment and local laws. Some systems use detailed schedules that assign specific values to different types of injuries—for example, losing a finger versus losing a limb.

This distinction matters because it influences not just your finances, but your future planning. Temporary disability is about getting back on your feet. Permanent disability is about adapting to a new reality—and having the support to do so.

Vocational Rehabilitation Benefits

Not every injured worker can simply return to their old job once they recover. Sometimes, the injury changes what you’re physically or mentally قادر of doing. That’s where vocational rehabilitation benefits step in, acting as a bridge between injury and a new form of employment.

Think of it like a career reset button—but with structured support. These benefits are designed to help injured workers gain new skills, find alternative employment, or re-enter the workforce in a different capacity. This could include job training programs, resume assistance, career counseling, and even tuition for educational courses.

For example, imagine a construction worker who suffers a serious back injury and can no longer perform physically demanding tasks. Instead of being left without options, vocational rehabilitation might help them transition into a supervisory role, safety inspector position, or even a completely different field like project management.

These programs are often tailored to the individual, taking into account their previous experience, education level, physical limitations, and local job market conditions. The goal isn’t just to find any job—it’s to find sustainable, meaningful employment that aligns with the worker’s new capabilities.

In some cases, workers may also receive maintenance benefits during their training period, ensuring they still have income while learning new skills. This removes the pressure of choosing between immediate income and long-term stability.

Despite their value, vocational rehabilitation programs are sometimes underutilized. Workers may not be aware they exist, or they may feel hesitant about starting over in a new career. But when used effectively, these benefits can be life-changing. They shift the focus from what was lost to what’s still possible, offering a pathway forward rather than a dead end.

Who Is Eligible for Workers' Compensation?

Covered Employees

Eligibility for workers' compensation might seem straightforward at first glance—if you’re injured at work, you’re covered. But in reality, it’s a bit more nuanced. Not every worker automatically qualifies, and the specifics depend heavily on employment status, job type, and local laws.

Generally speaking, most full-time and part-time employees are covered from the moment they start their job. There’s usually no waiting period for eligibility, which means even new hires are protected. This immediate coverage is one of the system’s strengths, ensuring that workers aren’t left vulnerable during their early days on the job.

Industries with higher risk—like construction, manufacturing, and healthcare—tend to have stricter enforcement of workers' compensation requirements. Employers in these fields are almost always required to carry insurance, given the increased likelihood of workplace injuries.

Interestingly, coverage isn’t limited to physical injuries. Many jurisdictions now recognize occupational illnesses and mental health conditions as valid claims. For instance, prolonged exposure to harmful chemicals or chronic workplace stress can qualify for benefits if properly documented.

However, one key factor is that the injury must be work-related. This doesn’t necessarily mean it has to occur at the workplace. If you’re injured while performing job duties off-site—like making deliveries or attending a work event—you may still be eligible.

Employers are generally required to inform employees about their rights under workers' compensation laws, often through workplace postings or onboarding materials. Still, many workers remain unaware of the full scope of their coverage until they actually need it.

Understanding whether you’re covered isn’t just a technical detail—it’s the foundation of your rights. Knowing where you stand can save time, reduce stress, and ensure you take the right steps if an injury occurs.

Common Eligibility Exceptions

While workers' compensation casts a wide safety net, there are notable exceptions that can catch people off guard. One of the most common exclusions involves independent contractors. Unlike traditional employees, independent contractors are typically not covered under workers' compensation laws, which means they’re responsible for their own insurance.

This distinction has become increasingly relevant in the gig economy. Ride-share drivers, freelance workers, and contract-based professionals often fall into a gray area where coverage isn’t guaranteed. Some companies offer alternative protections, but they don’t always match the scope of traditional workers' compensation.

Another major exception involves injuries resulting from misconduct or policy violations. If an employee is under the influence of drugs or alcohol at the time of the accident, their claim may be denied. Similarly, injuries sustained while intentionally violating safety rules or engaging in horseplay might not qualify.

There are also cases where injuries occur outside the scope of employment. For example, if you’re injured during a personal errand unrelated to your job duties—even if it happens during work hours—you may not be eligible for benefits.

Certain categories of workers, such as seasonal employees, agricultural workers, or domestic workers, may have limited or no coverage depending on local laws. These exceptions vary widely, which makes it essential to understand the regulations specific to your region.

The takeaway here is simple: eligibility isn’t automatic in every situation. Knowing the boundaries of coverage can help you avoid unpleasant surprises and ensure you take appropriate precautions—especially if your work arrangement falls outside traditional employment models.

How to File a Workers' Compensation Claim

Step-by-Step Filing Process

Filing a workers' compensation claim might sound intimidating, but when broken down into steps, it becomes much more manageable. The key is acting quickly and following the correct process—because delays or mistakes can complicate your case.

The process usually starts the moment an injury occurs. The first step is to report the injury to your employer as soon as possible. Many jurisdictions have strict deadlines for reporting, sometimes as short as a few days. Waiting too long can jeopardize your eligibility for benefits.

Next comes seeking medical attention. In some cases, your employer may direct you to a specific healthcare provider. Be sure to clearly explain that your injury is work-related, as this ensures proper documentation for your claim.

Once the injury is reported, your employer should provide you with the necessary claim forms. You’ll need to fill these out accurately, detailing how and when the injury occurred. This information becomes the foundation of your case, so clarity and honesty are essential.

After submission, the insurance company reviews your claim. They may request additional information, conduct investigations, or schedule medical evaluations. This phase can take time, depending on the complexity of the case.

If approved, benefits begin according to your eligibility. If denied, you typically have the right to appeal the decision, which may involve hearings or legal representation.

The process might feel bureaucratic, but each step serves a purpose. It ensures that claims are legitimate while providing a structured path for injured workers to receive support.

Common Mistakes to Avoid

Even small missteps during the claims process can lead to delays—or worse, denials. One of the most common mistakes is failing to report the injury promptly. It might seem harmless to wait a few days, especially if the injury appears minor, but this can raise doubts about the validity of your claim.

Another frequent issue is incomplete or inconsistent documentation. If your account of the incident changes over time, or if medical records don’t align with your report, it can create red flags for insurers. Consistency is key—every detail should match across all documents.

Some workers also make the mistake of not following medical advice. Skipping appointments or ignoring treatment plans can signal that the injury isn’t as serious as claimed, potentially affecting your benefits.

Posting about your injury on social media might seem unrelated, but it can also backfire. Insurance companies sometimes monitor online activity, and posts that contradict your claim—like photos of physical activity—can be used against you.

Avoiding these pitfalls isn’t about being perfect—it’s about being mindful. A careful, well-documented approach can make the difference between a smooth process and a frustrating ordeal.

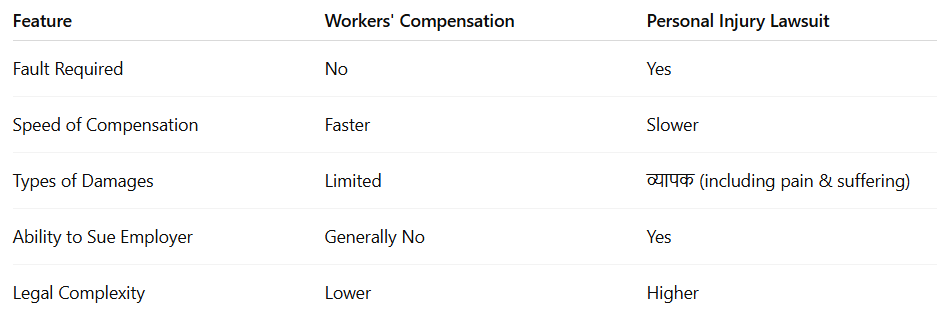

Workers' Compensation vs Personal Injury Lawsuits

Key Differences Explained

At first glance, workers' compensation claims and personal injury lawsuits might seem like two sides of the same coin. Both involve injuries, compensation, and questions about responsibility. But once you dig a little deeper, the differences become crystal clear—and understanding them can completely change how you approach a workplace injury situation.

The most fundamental distinction lies in fault. Workers' compensation operates under that no-fault system discussed earlier. You don’t need to prove your employer did anything wrong to receive benefits. On the flip side, personal injury lawsuits are all about proving negligence. You must demonstrate that another party—often your employer or a third party—failed to act responsibly, and that failure directly caused your injury. That alone makes personal injury cases more complex, time-consuming, and uncertain.

Then there’s the matter of compensation scope. Workers' compensation provides structured benefits: medical expenses, partial wage replacement, disability payments, and sometimes vocational rehabilitation. It’s predictable but limited. Personal injury lawsuits, however, can include a much broader range of damages—like full lost wages, pain and suffering, emotional distress, and even punitive damages in extreme cases. The trade-off? There’s no guarantee you’ll win.

Another key difference is legal access. When you accept workers' compensation benefits, you typically waive your right to sue your employer. It’s part of that built-in compromise: quick benefits in exchange for limited legal action. However, there are exceptions. If a third party—say, a subcontractor or equipment manufacturer—contributed to your injury, you may still be able to file a personal injury claim against them while receiving workers' compensation.

Let’s break it down in a simple comparison table:

One isn’t universally better than the other—it depends on your situation. Workers' compensation is like a safety net: reliable, quick, and structured. Personal injury lawsuits are more like a high-risk, high-reward path. Knowing when each applies can save you from missed opportunities or unnecessary legal battles.

Conclusion

Workers' compensation benefits form a crucial backbone of modern employment systems, quietly supporting millions of workers when things don’t go as planned. From covering medical bills to replacing lost wages and even helping individuals pivot into new careers, the system is designed to provide stability in moments of uncertainty. It’s not flashy, and it’s not always perfect, but it serves a purpose that’s hard to overstate.

What makes this system particularly interesting is the balance it tries to maintain. Employees get timely support without needing to fight lengthy legal battles, while employers gain protection from unpredictable lawsuits. That trade-off—the no-fault structure—is what keeps everything moving efficiently, even if it sometimes limits the scope of compensation.

Still, navigating workers' compensation isn’t always straightforward. Eligibility rules, claim procedures, and benefit types can vary widely depending on where you live and work. A small mistake—like missing a reporting deadline or misunderstanding your rights—can have outsized consequences. That’s why awareness is everything. The more you understand how the system works, the better equipped you are to use it effectively.

It’s also worth recognizing that workplace injuries don’t just affect physical health—they ripple into financial stability, mental well-being, and long-term career paths. Workers' compensation, at its best, acknowledges this broader impact and provides tools to rebuild, not just recover.

So whether you’re an employee wanting to protect your rights or an employer aiming to stay compliant and supportive, understanding workers' compensation benefits isn’t optional—it’s essential. Because when something goes wrong at work, the last thing you want is confusion about what comes next.

FAQs

1. How long do workers' compensation benefits last?

The duration of workers' compensation benefits depends largely on the nature and severity of your injury. Temporary benefits typically last until you recover or reach maximum medical improvement (MMI), while permanent disability benefits can extend for years or even a lifetime in severe cases. Each jurisdiction has its own rules, so timelines can vary significantly. It’s important to stay updated with your case status and medical evaluations, as these directly influence how long benefits continue.

2. Can I choose my own doctor for treatment?

In many cases, your employer or their insurance provider will require you to visit an approved healthcare provider, especially during the initial stages of treatment. However, some regions allow you to switch doctors after a certain period or under specific conditions. Understanding your local regulations can help you make informed decisions about your care without jeopardizing your claim.

3. What happens if my claim is denied?

A denied claim isn’t the end of the road. You typically have the right to appeal the decision, which may involve submitting additional evidence, attending hearings, or consulting with a workers' compensation attorney. Many claims are initially denied due to missing information or technical errors, so addressing those issues can often lead to a successful appeal.

4. Are workers' compensation benefits taxable?

Generally, workers' compensation benefits are not considered taxable income at the federal level in many countries, including the United States. However, there can be exceptions, especially if you’re also receiving other forms of income like Social Security Disability benefits. It’s always a good idea to consult a tax professional to understand your specific situation.

5. Can I return to work while receiving benefits?

Yes, but it depends on your medical condition and work restrictions. If your doctor clears you for light-duty work, you may return in a limited capacity while still receiving partial wage replacement benefits. This arrangement can help you transition back into the workforce without losing financial support entirely.