Workers Compensation Exemption: Complete Guide for Employers and Independent Workers

Understanding Workers Compensation Basics

What Is Workers Compensation Insurance?

Workers compensation insurance is one of those things most people don’t think about until something goes wrong—and when it does, it suddenly becomes incredibly important. At its core, workers compensation is a type of insurance that provides medical benefits and wage replacement to employees who get injured or fall ill due to their job. Think of it as a financial safety net that catches both the worker and the employer when workplace accidents happen.

Imagine a construction worker slipping off a ladder or an office employee developing carpal tunnel syndrome after years of repetitive tasks. Without workers compensation, those situations could spiral into lawsuits, financial hardship, and prolonged disputes. Instead, this system creates a no-fault arrangement. Employees receive compensation without needing to prove employer negligence, and in return, employers are typically protected from costly lawsuits.

In most regions, workers compensation is not optional. Governments mandate it because workplace injuries are more common than people assume. According to labor statistics from various developed economies, millions of workplace injuries occur annually, costing businesses billions in lost productivity and medical expenses. That alone explains why regulations around this insurance are taken so seriously.

For employers, workers compensation premiums are influenced by factors like industry risk, payroll size, and past claims history. High-risk industries such as construction or manufacturing usually face higher premiums compared to office-based businesses. Employees, on the other hand, gain peace of mind knowing that if something happens, they won’t be left covering medical bills out of pocket.

So where does workers compensation exemption fit into all of this? That’s where things start to get interesting—and a bit complicated. Not everyone is required to carry this insurance, and not every worker is automatically covered. Understanding the basics is the first step toward making sense of exemptions and whether they might apply to you.

Why Workers Compensation Laws Exist

Workers compensation laws didn’t just appear out of nowhere—they were born out of necessity during a time when industrial jobs were booming and workplace injuries were alarmingly frequent. Back in the early 20th century, injured workers had limited options. They either returned to work injured, faced financial ruin, or engaged in long, uncertain legal battles with their employers. None of those outcomes were ideal, which is why governments stepped in to create a more balanced system.

The primary goal of these laws is to create fairness. On one side, employees receive guaranteed compensation for work-related injuries. On the other, employers avoid unpredictable lawsuits that could potentially bankrupt their businesses. It’s a trade-off that stabilizes both sides of the workforce equation.

Another key reason these laws exist is to promote safer workplaces. When employers are financially responsible for injuries through insurance premiums, they’re more likely to invest in safety measures, training, and compliance programs. This creates a ripple effect—fewer injuries, lower insurance costs, and a healthier workforce overall.

There’s also a broader economic perspective to consider. Workplace injuries don’t just affect individuals; they impact productivity, healthcare systems, and even national economies. By ensuring injured workers receive timely medical care and wage support, workers compensation laws help keep the workforce active and reduce long-term economic strain.

But here’s where things get nuanced: not every worker fits neatly into the traditional employee category. Freelancers, independent contractors, and business owners often operate outside standard employment structures. This is exactly why workers compensation exemptions exist—to provide flexibility in a system that would otherwise be too rigid.

However, exemptions are not a loophole to be taken lightly. They come with responsibilities, trade-offs, and potential risks that can significantly impact both financial security and legal compliance. Understanding why these laws exist helps clarify why exemptions are carefully regulated and why not everyone qualifies for them.

What Is a Workers Compensation Exemption?

Definition and Core Concept

A workers compensation exemption is essentially a legal provision that allows certain individuals or businesses to opt out of carrying workers compensation insurance. At first glance, that might sound like an easy way to cut costs or simplify operations—but the reality is far more complex.

In simple terms, an exemption means you are choosing not to participate in the standard workers compensation system. This usually applies to specific categories of workers, such as independent contractors, sole proprietors, partners in a business, or corporate officers. These individuals can file formal documentation with the relevant state or regulatory body to declare that they are exempt from coverage requirements.

Why would someone do this? The most common reason is cost savings. Workers compensation insurance can be expensive, particularly in high-risk industries. For small business owners or self-employed individuals, those premiums can feel like a heavy burden. By claiming an exemption, they eliminate that ongoing expense.

However, opting out also means giving up the protections that come with the system. If an exempt individual gets injured on the job, they won’t receive automatic medical coverage or wage replacement through workers compensation. Instead, they must rely on personal health insurance, savings, or other forms of coverage.

There’s also a legal dimension to consider. Filing for an exemption typically involves signing a waiver acknowledging that you understand the risks and are voluntarily choosing to forgo coverage. This isn’t something you can do casually—it requires careful consideration and, in many cases, proper documentation and approval.

Another important aspect is that exemptions are not universally applicable. Each state or country has its own rules about who can qualify and under what conditions. Some jurisdictions are stricter than others, especially in industries where workplace injuries are more likely.

In essence, a workers compensation exemption is a strategic decision. It can offer flexibility and cost savings, but it also shifts responsibility squarely onto the individual or business owner. Understanding this balance is key before deciding whether an exemption is the right move.

Who Typically Seeks Exemption

Not everyone is eligible for a workers compensation exemption, and not everyone would benefit from one even if they were. The individuals who typically pursue exemptions tend to fall into specific categories, each with their own motivations and circumstances.

One of the most common groups is independent contractors. These are individuals who work for themselves rather than being employed by a company. Since they are not technically employees, many jurisdictions do not require them to carry workers compensation insurance. Instead, they can choose whether to obtain coverage or file for an exemption.

Small business owners are another major group. For example, a sole proprietor running a small landscaping business might decide to exempt themselves from coverage to reduce operating costs. Similarly, partners in a business or members of a limited liability company (LLC) often have the option to opt out, depending on local laws.

Corporate officers and executives sometimes seek exemptions as well. In certain states, officers of a corporation who own a significant percentage of the business can file for exemption. This is particularly common in family-owned businesses where the leadership team is closely involved in daily operations.

There are also industry-specific cases. In sectors like construction, exemptions are more tightly regulated due to the higher risk of injury. Some states require contractors to provide proof of exemption status when bidding on projects, ensuring transparency and compliance.

But here’s something that often gets overlooked: just because you can seek an exemption doesn’t mean you should. The decision depends heavily on your risk tolerance, financial situation, and the nature of your work. A freelance graphic designer working from home faces very different risks compared to a roofing contractor working at heights.

In many cases, professionals consult with insurance advisors or legal experts before making this choice. That’s because the consequences of getting it wrong can be significant—not just financially, but legally as well.

Understanding who typically seeks exemptions provides valuable context, but it also highlights an important truth: exemptions are not a one-size-fits-all solution. They are a calculated decision that should be approached with careful thought and a clear understanding of both the benefits and the risks.

Types of Workers Compensation Exemptions

Independent Contractor Exemptions

If there’s one group that frequently navigates the world of workers compensation exemption, it’s independent contractors. These are the freelancers, gig workers, and self-employed professionals who operate outside traditional employment structures. Think of a freelance web developer, a rideshare driver, or even a self-employed electrician—they all fall into this category.

The defining characteristic of an independent contractor is control. They typically decide how, when, and where the work gets done, unlike employees who follow company policies and schedules. Because of this independence, most jurisdictions do not require employers to provide workers compensation coverage for them. Instead, contractors often have the option to file for an exemption or simply operate without coverage.

But here’s where things get tricky. Misclassification is a major issue. Some businesses intentionally—or unintentionally—label employees as independent contractors to avoid paying for workers compensation insurance. Governments have cracked down on this because it shifts risk unfairly onto workers. According to labor enforcement data in several regions, misclassification cases have increased significantly in industries like construction and logistics.

For legitimate independent contractors, the exemption can be appealing. It reduces overhead costs and simplifies administrative responsibilities. However, it also means assuming full responsibility for any injuries or illnesses that occur on the job. Imagine a freelance photographer injuring their back during a shoot—without coverage, medical bills and lost income come straight out of their own pocket.

Many contractors mitigate this risk by purchasing private insurance policies, such as occupational accident insurance or disability coverage. These alternatives can provide some level of protection, though they may not be as comprehensive as traditional workers compensation.

So while the independent contractor exemption offers flexibility, it’s not a free pass. It requires a clear understanding of your legal status, a willingness to accept risk, and often, a backup plan to handle unexpected situations.

Business Owner and Corporate Officer Exemptions

Business owners and corporate officers occupy a unique position when it comes to workers compensation. They’re not just workers—they’re decision-makers, stakeholders, and often the backbone of their companies. Because of this, many jurisdictions allow them to apply for workers compensation exemptions under specific conditions.

Let’s say you own a small construction company. You might have a handful of employees who are required to be covered under workers compensation insurance. But as the owner, you may have the option to exempt yourself. The same applies to corporate officers who hold a significant ownership stake in the business.

Why would someone in this position choose exemption? The answer often comes down to cost and control. Workers compensation premiums can be substantial, especially in high-risk industries. By exempting themselves, business owners can reduce expenses and allocate resources elsewhere.

However, this decision isn’t without consequences. Owners who opt out of coverage essentially remove their safety net. If they’re injured while working—whether it’s lifting heavy equipment or handling day-to-day operations—they won’t receive benefits through workers compensation.

There’s also a strategic element to consider. Some clients or contracts require proof of workers compensation coverage, even for business owners. In these cases, having an exemption might limit opportunities or create additional hurdles.

From a legal standpoint, the process usually involves filing formal paperwork with the state and meeting specific eligibility criteria. For example, some states require corporate officers to own a certain percentage of the company before they can qualify for exemption.

Ultimately, this type of exemption is about balancing risk and reward. It offers financial relief and flexibility, but it also places greater responsibility on the individual. For many business owners, the decision comes down to a simple question: is the cost savings worth the potential risk?

Industry-Specific Exemptions

Not all industries are created equal, and neither are their rules for workers compensation. Some sectors have unique provisions that allow for industry-specific exemptions, often shaped by the nature of the work and the level of risk involved.

Take agriculture, for example. In many regions, small farms with limited employees may be exempt from mandatory workers compensation requirements. Similarly, certain domestic workers or casual laborers might fall outside standard coverage rules. These exemptions are often designed to accommodate industries where traditional employment structures don’t fully apply.

On the other end of the spectrum, high-risk industries like construction and manufacturing tend to have stricter regulations. Exemptions still exist, but they’re often accompanied by additional requirements, such as proof of independent contractor status or formal exemption certificates. This is because the potential for injury is significantly higher, and regulators want to ensure that workers are not left unprotected.

There are also niche cases. For instance, some states provide exemptions for real estate agents or commission-based sales professionals, recognizing their independent working arrangements. Similarly, certain transportation or logistics roles may qualify for exemption under specific conditions.

What’s important to understand is that these exemptions are not arbitrary. They’re carefully designed to reflect the realities of each industry. However, they also create a patchwork of rules that can be confusing to navigate.

This is why many professionals turn to legal advisors or industry associations for guidance. A misunderstanding of exemption rules can lead to penalties, fines, or even legal disputes. And in some cases, failing to provide required coverage can result in significant financial liability.

Industry-specific exemptions highlight the complexity of workers compensation systems. They show that while flexibility exists, it’s always balanced against the need to protect workers and maintain fair practices across different sectors.

Legal Requirements for Exemption

State-by-State Variations

One of the most important things to understand about workers compensation exemption is that there is no universal rulebook. The requirements, eligibility criteria, and application processes vary widely depending on where you are. What’s perfectly acceptable in one state—or country—might be completely prohibited in another.

For example, in some U.S. states, sole proprietors are automatically exempt unless they choose to opt in. In others, they must actively file for an exemption to avoid mandatory coverage. Corporate officers might be allowed to exempt themselves in one jurisdiction but required to carry insurance in another unless they meet strict ownership thresholds.

These variations exist because workers compensation laws are typically governed at the state or regional level. Each jurisdiction tailors its regulations based on local economic conditions, industry risks, and policy priorities. This creates a landscape that can feel like a maze, especially for businesses operating across multiple locations.

Statistics from insurance regulatory bodies show that compliance issues often arise not from intentional violations but from misunderstandings of these regional differences. Businesses assume that rules are consistent everywhere, only to discover—sometimes the hard way—that they’re not.

Another layer of complexity comes from industry-specific regulations within each state. For instance, construction companies may face stricter requirements than office-based businesses, even within the same jurisdiction. This means that exemptions are not just location-dependent but also industry-dependent.

Because of this, staying informed is critical. Many states provide online resources, guides, and forms to help individuals navigate the exemption process. Consulting with an insurance broker or legal expert can also provide clarity, especially for more complex situations.

The key takeaway here is simple: don’t assume. Always verify the specific rules that apply to your location and industry before pursuing an exemption.

Required Documentation and Filing Process

Applying for a workers compensation exemption isn’t as simple as checking a box. It involves a formal process that requires documentation, verification, and, in some cases, periodic renewal. Think of it as a legal declaration—you’re officially stating that you understand the risks and are choosing to operate without coverage.

The process typically begins with completing an exemption form provided by your state or regulatory authority. This form may ask for details such as your business structure, ownership percentage, type of work, and reason for seeking exemption. In some cases, you’ll also need to provide supporting documents, such as business licenses or proof of independent contractor status.

One common requirement is signing an affidavit or waiver. This document confirms that you acknowledge the consequences of exemption, including the lack of workers compensation benefits in case of injury. It’s not just paperwork—it’s a legally binding statement.

Processing times can vary. Some jurisdictions approve exemptions within a few days, while others may take weeks. Once approved, you’ll typically receive a certificate of exemption, which serves as proof for clients, contractors, or regulatory bodies.

However, the process doesn’t end there. Many exemptions have expiration dates and must be renewed periodically. Failing to renew on time can result in automatic reinstatement of coverage requirements—or worse, penalties for non-compliance.

Mistakes during the application process are more common than you might think. Missing information, incorrect classification, or incomplete documentation can delay approval or lead to rejection. This is why attention to detail is crucial.

In essence, obtaining a workers compensation exemption is a structured process that requires careful preparation. It’s not რთ just about opting out—it’s about doing so in a way that’s legally compliant and fully informed.

Benefits of Workers Compensation Exemption

Cost Savings for Businesses

One of the biggest reasons people consider a workers compensation exemption is simple: money. Insurance premiums, especially in high-risk industries, can take a noticeable chunk out of a business’s operating budget. For small businesses or startups already juggling tight margins, every dollar counts. So when the option to legally opt out of those recurring costs appears, it’s understandably tempting.

Let’s put it into perspective. Workers compensation premiums are typically calculated based on payroll size and industry risk classification. A construction company, for instance, might pay significantly higher premiums than a marketing agency because of the increased likelihood of workplace injuries. According to industry estimates, workers compensation insurance can cost anywhere from a few hundred to several thousand dollars per employee annually, depending on risk levels. Over time, that adds up quickly.

By choosing exemption, eligible business owners and independent professionals can redirect those funds into other areas—like hiring, equipment upgrades, or marketing. It’s like freeing up cash flow that was previously locked into insurance expenses. For a small business trying to grow, that flexibility can make a real difference.

However, the savings aren’t just about premiums. There’s also reduced administrative overhead. Managing workers compensation policies often involves audits, compliance checks, and paperwork. Exemption simplifies operations by removing those ongoing responsibilities.

But here’s the catch: those savings come with a trade-off. When you opt out, you’re essentially self-insuring. That means if something goes wrong, the financial burden falls entirely on you. For low-risk professions, this might feel like a manageable gamble. For higher-risk roles, it’s a much bigger leap.

Some business owners treat exemption as part of a broader financial strategy. They might set aside emergency funds or invest in alternative insurance products to offset potential risks. This way, they still benefit from cost savings while maintaining a safety net.

In the end, the appeal of cost savings is undeniable. But it’s not just about cutting expenses—it’s about understanding what you’re giving up in return and deciding whether that trade-off aligns with your financial goals and risk tolerance.

Flexibility for Independent Professionals

If cost savings are the financial incentive, then flexibility is the lifestyle perk. For many independent professionals, a workers compensation exemption isn’t just about money—it’s about control. Control over how they work, how they manage risk, and how they structure their business.

Think about freelancers, consultants, or gig workers. These individuals often operate across multiple clients, projects, and even industries. Being tied to a traditional workers compensation system can feel restrictive, especially when their work doesn’t fit neatly into standard employment categories. Exemption allows them to operate on their own terms.

For example, a freelance graphic designer working from home might see little value in paying for workers compensation insurance. Their risk of workplace injury is relatively low, and they may prefer to rely on personal health insurance instead. On the other hand, a traveling photographer might choose to invest in specialized coverage tailored to their unique needs rather than a one-size-fits-all policy.

This flexibility extends to decision-making. Independent professionals can choose when and how to invest in protection. They’re not locked into mandatory systems—they can explore alternatives like disability insurance, liability coverage, or even savings-based safety nets.

There’s also a psychological aspect to consider. Being able to make your own choices about risk management can feel empowering. It reinforces the independence that many freelancers value in the first place. Instead of following rigid requirements, they can build a system that aligns with their personal and professional priorities.

Of course, flexibility doesn’t mean freedom from responsibility. In fact, it often means the opposite. Without workers compensation coverage, independent professionals must be proactive about managing risks. This includes maintaining proper safety practices, securing appropriate insurance where needed, and planning for unexpected events.

The key here is balance. Flexibility is a powerful advantage, but it works best when paired with informed decision-making. When used wisely, a workers compensation exemption can support a more adaptable, personalized approach to work and risk management.

Risks and Drawbacks of Exemption

Financial and Legal Risks

While the benefits of a workers compensation exemption can be appealing, the risks are just as real—and sometimes far more significant. It’s easy to focus on the immediate savings, but the long-term implications can catch people off guard if they’re not fully prepared.

The most obvious risk is financial exposure. Without workers compensation insurance, there’s no safety net if an injury occurs. Medical bills, rehabilitation costs, and lost income all come directly out of pocket. And those costs can escalate quickly. A single serious injury could result in tens of thousands—or even hundreds of thousands—of dollars in expenses.

But the risks don’t stop there. There’s also potential legal exposure. If a worker is misclassified as an independent contractor and later files a claim, the business could face penalties, fines, and even lawsuits. Regulatory agencies take misclassification seriously, and enforcement efforts have increased in recent years.

For business owners, there’s an added layer of complexity. If you exempt yourself but still employ others, you must ensure that your employees are properly covered. Failing to do so can result in severe consequences, including stop-work orders or legal action.

Another often-overlooked risk is contractual limitations. Some clients or projects require proof of workers compensation coverage. Without it, you might lose out on opportunities or be excluded from certain contracts. This can indirectly impact revenue and growth potential.

There’s also the unpredictability factor. Accidents don’t follow schedules, and even low-risk professions can encounter unexpected situations. A simple slip, repetitive strain injury, or unforeseen incident can quickly turn into a major financial burden.

This is why many experts emphasize the importance of risk assessment. Before choosing exemption, it’s crucial to evaluate not just the likelihood of injury but also the potential impact. It’s not about fear—it’s about preparedness.

In many ways, opting for exemption is like walking a tightrope. The rewards are there, but so are the risks. And staying balanced requires awareness, planning, and a clear understanding of what’s at stake.

Lack of Injury Protection

At the heart of the workers compensation exemption decision lies a simple but critical reality: no coverage means no built-in protection. This is perhaps the most significant drawback, and it’s one that deserves careful consideration.

Workers compensation insurance is designed to provide immediate support when something goes wrong. It covers medical expenses, rehabilitation, and a portion of lost wages, helping injured workers recover without financial strain. When you opt out, that safety net disappears.

Imagine a scenario where a self-employed contractor injures their hand while working. Without coverage, they not only face medical bills but also the loss of income during recovery. It’s a double hit—expenses increase while earnings decrease. For many, that combination can be financially devastating.

There’s also the issue of long-term impact. Some injuries require ongoing treatment or result in permanent limitations. Without workers compensation, there’s no structured system to provide continued support. This can affect not just finances but also career sustainability.

Another angle to consider is mental stress. Knowing that you’re fully responsible for any potential injury can create a constant underlying pressure. It’s like driving without insurance—you might never need it, but the risk is always there in the back of your mind.

That said, some individuals choose to address this gap through alternative means. Health insurance, disability coverage, and emergency savings can provide partial protection. However, these solutions often lack the comprehensive nature of workers compensation.

Ultimately, the lack of injury protection is the trade-off that defines exemption. It’s the price paid for flexibility and cost savings. For some, it’s a calculated risk that aligns with their circumstances. For others, it’s a risk that outweighs the benefits.

Understanding this trade-off is essential. It’s not just about what you gain by opting out—it’s about what you’re willing to handle on your own if things don’t go as planned.

How to Apply for a Workers Compensation Exemption

Step-by-Step Application Process

Applying for a workers compensation exemption might sound intimidating at first, but when you break it down, it’s actually a structured and manageable process. The key is understanding each step clearly and approaching it with attention to detail, because even small mistakes can delay approval or create compliance issues later.

The first step is determining eligibility. Not everyone qualifies for exemption, so you need to confirm whether your role—such as a sole proprietor, independent contractor, LLC member, or corporate officer—meets your state’s criteria. This often involves checking official labor or insurance department websites, which usually provide updated guidelines and forms.

Once eligibility is confirmed, the next step is completing the application form. This document typically requires detailed information about your business structure, ownership percentage, job role, and nature of work. It may feel a bit bureaucratic, but every field serves a purpose. Authorities use this information to verify that your exemption request is legitimate and not an attempt to bypass legal requirements.

After filling out the form, you’ll usually need to sign an affidavit or waiver. This is where things become more serious. By signing, you’re acknowledging that you understand the risks of not having workers compensation coverage. It’s not just paperwork—it’s a legal declaration that you’re choosing to forgo protection.

Next comes submission. Depending on your jurisdiction, this can often be done online, by mail, or in person. Some states process applications within a few business days, while others may take several weeks. Once approved, you’ll receive a certificate of exemption, which acts as official proof.

Finally, don’t forget about maintenance. Many exemptions expire after a certain period—often one or two years—and must be renewed. Keeping track of expiration dates is crucial to avoid accidental non-compliance.

In simple terms, the process follows a logical path:

Verify eligibility

Complete application

Sign waiver

Submit documentation

Receive certification

Renew when required

It’s not რთ complicated, but it does demand accuracy and awareness. Treat it like setting up a safety system—you’re choosing to operate differently, so you need to be extra careful about doing it correctly.

Common Mistakes to Avoid

Even though the application process seems straightforward, many people stumble into avoidable mistakes when applying for a workers compensation exemption. These missteps can lead to delays, rejections, or even legal complications, which is the last thing anyone wants when trying to simplify their business operations.

One of the most common mistakes is misclassification. This happens when someone assumes they qualify as an independent contractor or exempt business owner when, legally, they do not. For example, if you’re working under the direct control of a company but labeled as a contractor, regulators may view this as employee misclassification. This can trigger penalties and force retroactive insurance coverage.

Another frequent issue is incomplete or inaccurate paperwork. Missing fields, incorrect business details, or outdated information can slow down the approval process. It might seem minor, but even a small error—like a mismatched business name or incorrect license number—can raise red flags.

Timing is another critical factor. Many applicants forget that exemptions often have expiration dates. Failing to renew on time can result in losing exempt status, which may leave you unintentionally non-compliant. Imagine thinking you’re exempt, only to discover your certificate expired months ago—that’s a headache no one wants.

There’s also the mistake of overlooking contractual requirements. Some clients require proof of workers compensation coverage, regardless of exemption eligibility. If you don’t check these requirements beforehand, you could lose business opportunities or face last-minute complications.

Another subtle but important mistake is failing to plan for risk. Some individuals focus so much on getting the exemption that they forget to consider what happens afterward. Without a backup plan—like health insurance, disability coverage, or savings—they’re left vulnerable if something goes wrong.

Avoiding these mistakes comes down to awareness and preparation. Double-check your eligibility, review your paperwork carefully, keep track of deadlines, and think beyond the application itself. An exemption isn’t just a form—it’s a decision that affects your financial and legal safety.

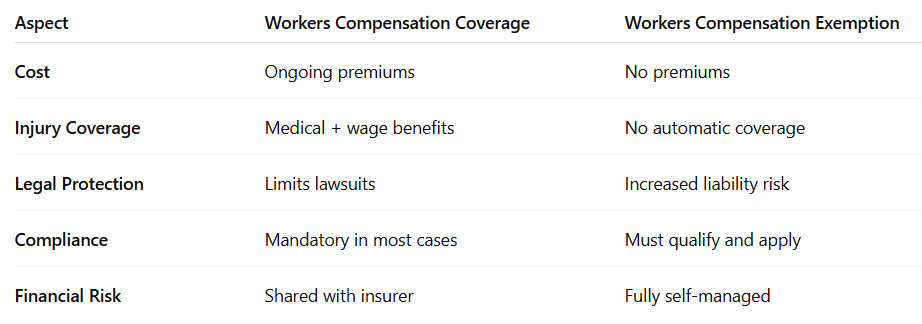

Workers Compensation Exemption vs Insurance Coverage

Key Differences Explained

At first glance, choosing between a workers compensation exemption and maintaining full insurance coverage might seem like a simple cost-based decision. But when you dig deeper, the differences go far beyond just premiums—they touch on protection, responsibility, and long-term stability.

Here’s a clear comparison to help visualize the contrast:

With coverage, the system is designed to absorb risk. If an employee gets injured, the insurance steps in to handle medical costs and lost wages. Employers gain predictability, and employees gain security. It’s a structured safety net that stabilizes both sides.

With exemption, the dynamic shifts completely. There’s no middleman. You’re essentially taking full responsibility for any incidents. While this eliminates premiums, it also removes the buffer that protects against unexpected events.

Another key difference lies in legal exposure. Workers compensation systems often limit an employee’s ability to sue an employer, creating a more controlled environment. Without coverage, that protection may not exist, increasing potential legal risks in certain scenarios.

There’s also a psychological difference. Coverage provides peace of mind—you know that if something happens, there’s a system in place to handle it. Exemption, on the other hand, requires a more proactive mindset. You’re not just working—you’re constantly managing risk behind the scenes.

So while the financial comparison is straightforward, the broader implications are more nuanced. It’s not just about saving money—it’s about deciding how much responsibility you’re willing to carry.

When Coverage Is the Better Choice

Even though a workers compensation exemption can be appealing, there are many situations where maintaining coverage is the smarter, safer choice. The challenge is recognizing when the risks outweigh the benefits.

If you operate in a high-risk industry—like construction, manufacturing, or transportation—coverage is often the better option. The likelihood of injury is simply too high to justify going without protection. In these environments, one accident can have serious financial and operational consequences.

Another scenario is when you have employees. In most jurisdictions, workers compensation coverage is mandatory for employees, regardless of whether the owner is exempt. Ensuring your team is protected isn’t just a legal requirement—it’s also a responsibility that affects morale, trust, and business reputation.

Coverage also becomes important when working with certain clients or contracts. Many organizations require proof of insurance before entering into agreements. Without it, you may be excluded from valuable opportunities.

There’s also the matter of financial stability. If you don’t have substantial savings or alternative insurance in place, opting for exemption can be risky. Coverage acts as a safeguard, ensuring that unexpected events don’t derail your finances.

Think of it like this: exemption is a calculated risk, while coverage is a safety-first approach. Neither is inherently right or wrong—it depends on your situation. But in cases where uncertainty is high or stakes are significant, coverage often provides a more reliable foundation.

The smartest decisions usually come from weighing both sides carefully. It’s not about choosing the cheaper option—it’s about choosing the one that aligns with your level of risk, your financial capacity, and your long-term goals.

Real-Life Examples of Workers Compensation Exemptions

Small Business Owners

To really understand how workers compensation exemption works in practice, it helps to look at real-world scenarios. Small business owners are among the most common users of exemptions, and their experiences highlight both the advantages and challenges.

Imagine a small bakery owned and operated by a single individual. The owner handles everything—from baking to customer service. Since there are no employees, the owner may choose to exempt themselves from workers compensation coverage. This reduces operating costs and simplifies administrative tasks, allowing them to focus on growing the business.

Now consider a slightly larger example: a family-owned construction company. The owners, who are also corporate officers, may file for exemption while still providing coverage for their employees. This approach allows them to balance cost savings with compliance, ensuring that workers are protected while minimizing expenses for leadership.

However, these decisions often come with careful planning. Many small business owners who opt for exemption set aside emergency funds or invest in alternative insurance policies. They understand that while they’re saving money upfront, they need a backup plan in case something goes wrong.

These examples show that exemption isn’t just a technical process—it’s a strategic decision shaped by the size, structure, and risk level of the business.

Freelancers and Contractors

Freelancers and independent contractors offer another perspective on workers compensation exemption. Their work environments are often more flexible, which influences how they approach risk.

Take a freelance writer working from home. Their risk of workplace injury is minimal, so opting for exemption makes practical sense. Instead of paying for workers compensation insurance, they might rely on health insurance and personal savings.

Now contrast that with a self-employed electrician. Their work involves physical labor and potential hazards, making the decision more complex. While they may still qualify for exemption, they might choose to invest in alternative coverage to protect against injuries.

These examples highlight an important point: exemption decisions are highly individual. Two professionals with similar statuses may make completely different choices based on their risk exposure and financial situation.

Conclusion and Key Takeaways

A workers compensation exemption isn’t just a checkbox—it’s a decision that shapes how you manage risk, finances, and responsibility in your professional life. It offers clear advantages, like cost savings and flexibility, but it also removes a critical layer of protection.

The right choice depends on your unique circumstances. Factors like industry risk, financial stability, legal requirements, and personal comfort with uncertainty all play a role. There’s no universal answer—only informed decisions.

Understanding both sides of the equation is what allows you to move forward confidently, whether you choose exemption or full coverage.

FAQs About Workers Compensation Exemption

1. Who qualifies for a workers compensation exemption?

Typically, independent contractors, sole proprietors, business partners, LLC members, and certain corporate officers may qualify, depending on state laws and ownership criteria.

2. Is workers compensation exemption legal?

Yes, but only when done according to local regulations. Filing proper documentation and meeting eligibility requirements is essential to remain compliant.

3. Can I reverse my exemption later?

In most cases, yes. You can choose to obtain workers compensation coverage at any time, even after previously being exempt.

4. Do I need exemption if I have no employees?

Not always. Some jurisdictions automatically exempt sole proprietors, while others require formal filing. It’s important to check local rules.

5. What happens if I get injured while exempt?

You are responsible for your own medical expenses and lost income unless you have alternative insurance or financial support in place.

SOURCEs

https://www.dol.gov/general/topic/workcomp

https://www.irs.gov/businesses/small-businesses-self-employed/independent-contractor-defined

https://www.thehartford.com/workers-compensation

https://www.travelers.com/business-insurance/workers-compensation

https://www.findlaw.com/injury/workers-compensation.html

https://www.nolo.com/legal-encyclopedia/workers-compensation